Estratégia de negociação de grade bidirecional com rastreamento de candlestick

Visão Geral

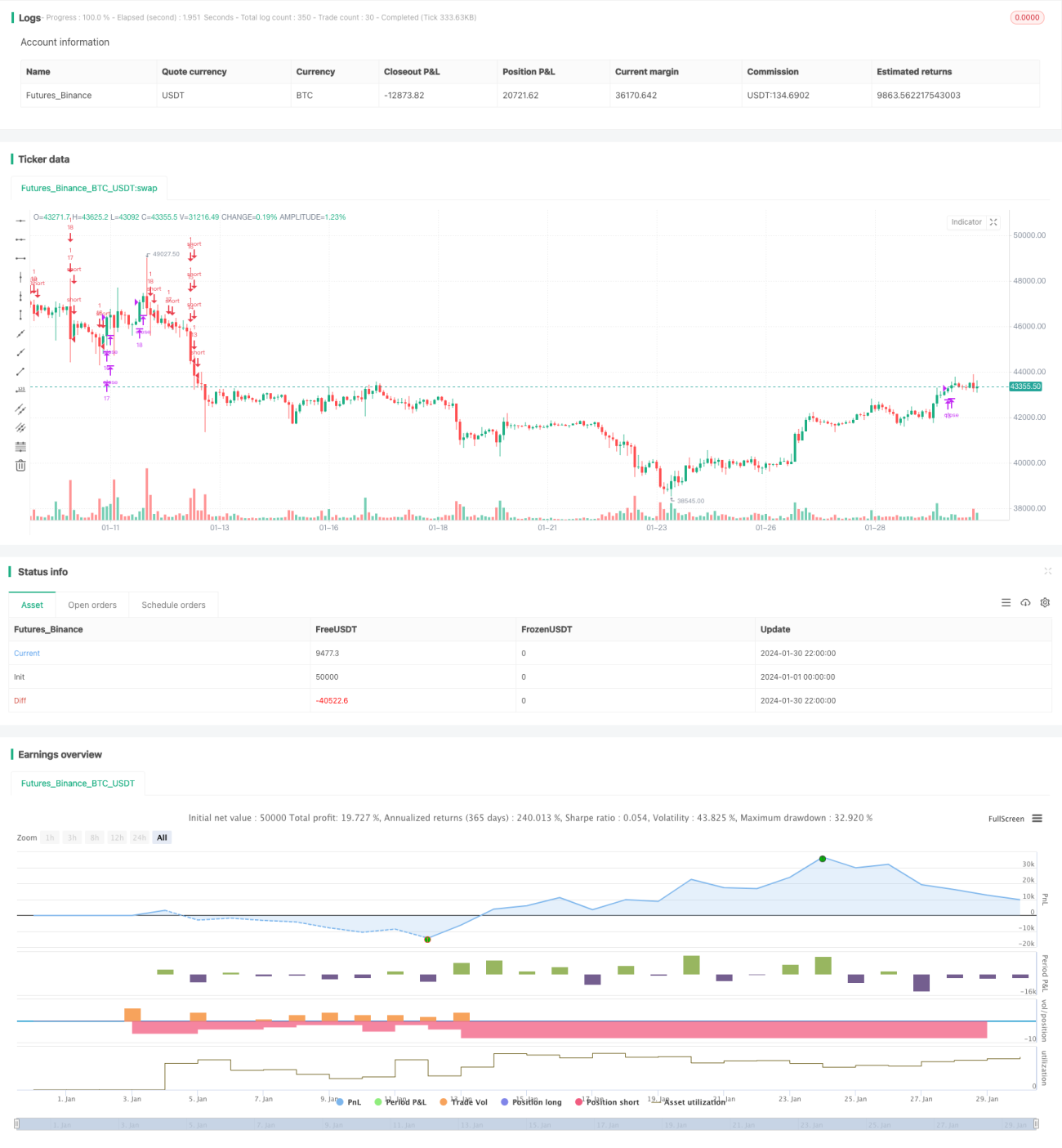

Esta estratégia é uma estratégia de trading de grade bidirecional baseada na variação em tempo real dos candles. Ela pode obter lucros estáveis tanto em mercados de alta quanto de baixa.

Princípio da Estratégia

-

Com base no número de grades definido pelo usuário, calcula automaticamente o intervalo de preços da grade e o preço de cada grade.

-

Quando o preço ultrapassa o preço da grade, abre uma posição comprada com uma quantidade fixa; quando o preço cai abaixo do preço da grade, fecha a posição comprada e abre uma posição vendida.

-

Dessa forma, quando o preço oscila dentro do intervalo da grade, é possível obter lucro acompanhando as variações de preço.

Análise de Vantagens

-

Cálculo automático de intervalos de grade razoáveis, sem necessidade de determinar suportes e resistências manualmente.

-

Trading bidirecional, adaptável a ambientes de mercado voláteis.

-

Quantidade fixa de abertura de posições, favorecendo o controle de risco.

-

Código intuitivo e simples, fácil de entender e modificar.

Análise de Riscos

-

Flutuações violentas do mercado podem levar a perdas ampliadas.

-

O acúmulo de taxas de negociação também afeta o lucro final.

-

É necessário definir um número adequado de grades; muitas grades aumentam a frequência de negociações, mas cada lucro é limitado.

Direções de Otimização

-

Adicionar uma estratégia de stop loss para evitar o agravamento das perdas.

-

Incluir ajuste dinâmico do número de grades.

-

Considerar a adição de alavancagem para ampliar o volume de negociação.

Resumo

A ideia geral desta estratégia é clara e simples, obtendo ganhos estáveis por meio do trading de grade bidirecional, embora também apresente certos riscos de negociação. Com otimizações contínuas, espera-se alcançar melhores resultados.

- 1