Estratégia de negociação baseada em rompimento de momentum

Visão Geral

Esta estratégia é uma estratégia de negociação de breakout baseada em indicadores de momentum. Ela utiliza múltiplos indicadores, como médias móveis, ATR e RSI, para avaliar a tendência do mercado e a volatilidade, combinando configurações rigorosas de stop profit e stop loss para realizar as operações. A estratégia determina principalmente se o preço ultrapassa ou rompe a média móvel adicionada ao intervalo do ATR para gerar sinais de negociação.

Princípio da Estratégia

A estratégia baseia-se nos seguintes pontos principais:

-

Utiliza a média móvel EMA para determinar a direção da tendência dos preços. Quando o preço cruza acima da média móvel, é um sinal de alta; quando cruza abaixo, é um sinal de baixa.

-

O indicador ATR avalia a volatilidade do mercado. O ATR multiplicado por um coeficiente serve como faixa de stop loss. Isso pode controlar efetivamente a perda por operação.

-

O indicador RSI avalia condições de sobrecompra e sobrevenda. As operações de breakout julgadas pelo preço do stop loss do ATR e pela média móvel devem ser acionadas apenas quando o RSI não estiver em sobrecompra ou sobrevenda. Isso evita falsos breakouts.

-

Utiliza máximas ou mínimas anteriores como base para o stop profit. O trailing stop profit pode travar mais lucros.

-

Regras rigorosas de stop profit e stop loss. O stop loss do ATR combinado com o indicador de volatilidade controla o risco, enquanto o stop profit permite travar os ganhos.

O sinal de entrada ocorre quando o preço rompe a média móvel mais a faixa de stop loss do ATR. Para um sinal de alta, o preço precisa cruzar acima desse ponto máximo; para um sinal de baixa, o preço precisa cruzar abaixo desse ponto mínimo.

Análise de Vantagens

Esta estratégia apresenta as seguintes vantagens:

-

A avaliação com múltiplos indicadores evita falsos breakouts, aumentando a precisão dos sinais.

-

A faixa de stop loss baseada no ATR mantém as perdas em um nível razoável.

-

O trailing stop profit dinâmico maximiza a captura de lucros.

-

Regras rigorosas de stop profit e stop loss ajudam no controle de risco.

-

Grande espaço para otimização de indicadores e parâmetros, permitindo ajustes conforme diferentes mercados.

Análise de Riscos

A estratégia também apresenta os seguintes riscos:

-

A rentabilidade está relacionada à volatilidade do mercado. Em mercados sem tendência clara ou com ciclos longos, o potencial de lucro é limitado.

-

Pode ocorrer um cenário em que o preço oscila no stop loss e depois rompe novamente. Isso pode impedir a entrada a tempo de acompanhar a tendência. É possível ajustar o preço do stop loss de forma mais flexível.

-

Risco de perseguir o mercado (chasing).

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

-

Ajustar os parâmetros da média móvel, ATR, etc., de acordo com diferentes ativos e períodos.

-

Podem ser introduzidos mais indicadores para julgamento, como MACD, KDJ, para avaliar sobrecompra e sobrevenda.

-

O coeficiente do stop loss pode ser ajustado em tempo real com base no valor do ATR, tornando o stop loss mais adaptável à volatilidade do mercado.

-

Criar uma combinação de múltiplos períodos de tempo. A combinação de indicadores de diferentes períodos pode melhorar a qualidade dos sinais.

-

Utilizar técnicas de aprendizado de máquina para testar e otimizar indicadores e parâmetros, alcançando a otimização dos parâmetros da estratégia.

Resumo

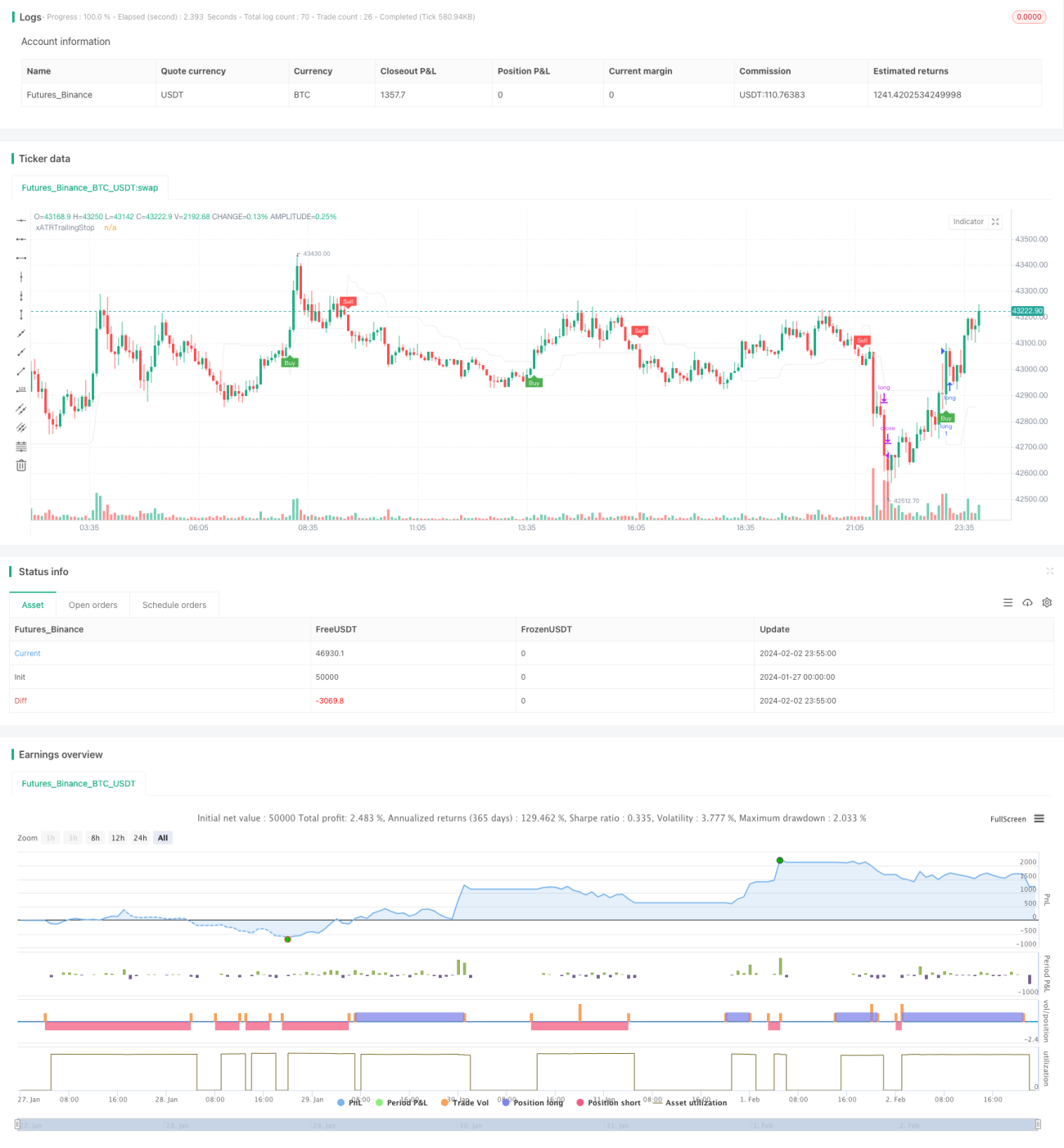

No geral, esta estratégia é uma estratégia de negociação de breakout que utiliza indicadores para julgar, com stop profit e stop loss rigorosos. Ela aproveita efetivamente as vantagens de indicadores como médias móveis, ATR e RSI, sendo capaz de determinar a direção da tendência do mercado. Combinada com configurações rigorosas de stop profit e stop loss, pode aproveitar as tendências para obter lucros enquanto controla os riscos. Com a otimização de parâmetros e regras, esta estratégia pode se tornar uma estratégia de negociação quantitativa válida para uso a longo prazo.

/*backtest

start: 2024-01-27 00:00:00

end: 2024-02-03 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="UT Bot Strategy", overlay = true)

//CREDITS to HPotter for the orginal code. The guy trying to sell this as his own is a scammer lol.

// Inputs- 1