Estratégia de Tendência com Bandas de Bollinger Adaptativas Bidirecionais

Visão Geral

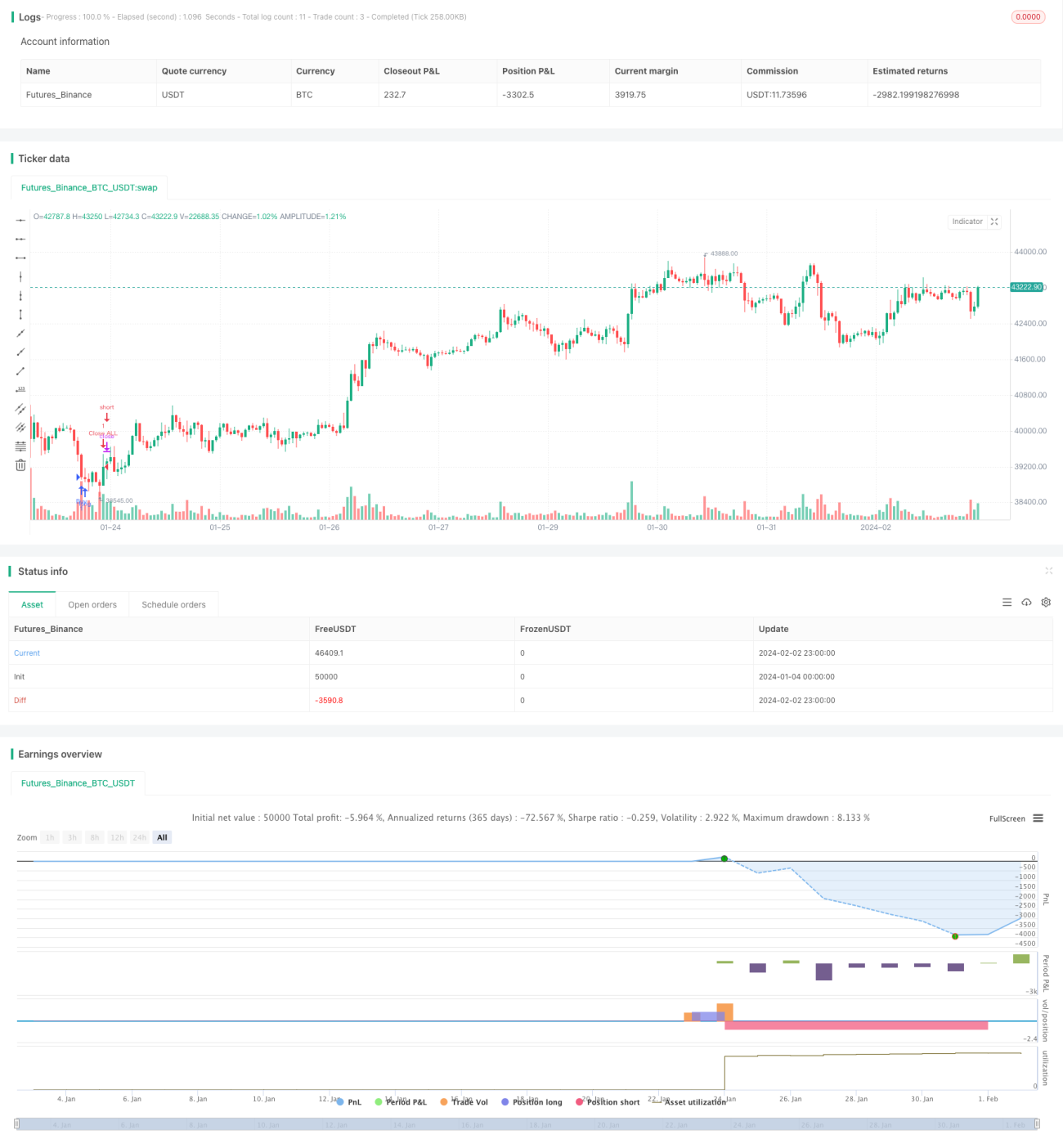

Esta estratégia utiliza um indicador de Bandas de Bollinger adaptativas bidirecionais para identificar a direção da tendência, combinado com ordens a mercado para executar um stop loss dinâmico, realizando uma negociação de tendência de alta eficiência.

Princípio da Estratégia

- Calcular a banda média, a banda superior e a banda inferior das Bandas de Bollinger com base em um determinado período.

- Se o preço romper a banda superior, entrar em posição comprada com trailing stop; se romper a banda inferior, entrar em posição vendida com trailing stop.

- Utilizar ordens a mercado para entrada rápida.

- Definir níveis de stop loss e take profit para gerenciamento da posição.

Análise de Vantagens

- O indicador de Bandas de Bollinger adaptativas é sensível à volatilidade do mercado, permitindo identificar rapidamente as mudanças de tendência.

- O uso de ordens a mercado para entrada rápida reduz o risco de slippage.

- Stop loss e take profit automáticos controlam rigorosamente o risco e garantem lucros.

Análise de Riscos

- As Bandas de Bollinger possuem inerentemente uma defasagem (lag), não sendo capazes de evitar completamente falsos rompimentos.

- As ordens a mercado não permitem controlar o preço de execução.

- É necessário definir adequadamente os níveis de stop loss e take profit.

Direções de Otimização

- Ajustar os parâmetros das Bandas de Bollinger para otimizar a sensibilidade na identificação de tendências.

- Adicionar indicadores como volume ou MACD para filtrar falsos rompimentos.

- Otimizar a configuração dos níveis de stop loss e take profit.

Resumo

Esta estratégia aproveita ao máximo a capacidade das Bandas de Bollinger de identificar a direção e as mudanças da tendência, combinando-as com ordens a mercado para execução rápida em ambos os lados (compra e venda) com trailing stop, obtendo retornos excessivos enquanto controla o risco. Através de uma otimização adicional dos parâmetros das Bandas de Bollinger, da inclusão de indicadores auxiliares para filtragem e do ajuste da lógica de stop loss e take profit, é possível alcançar um desempenho ainda melhor. A estratégia possui uma lógica clara e é de fácil implementação, sendo uma abordagem eficiente e confiável para negociação de tendências.

- 1