Estratégia de Índice de Momentum de Reversão Dupla

Visão Geral

A Estratégia de Índice de Momentum com Dupla Reversão é uma estratégia combinada que integra a Estratégia de Reversão 123 e a Estratégia de Índice de Momentum Relativo (RMI). Ela visa melhorar a precisão das decisões de negociação utilizando sinais duplos.

Princípio da Estratégia

A estratégia é composta por duas partes:

-

Estratégia de Reversão 123

- Quando o preço de fechamento de ontem é menor que o de anteontem, o preço de fechamento de hoje é maior que o de ontem, e a linha K lenta de 9 períodos está abaixo de 50, opera-se comprado.

- Quando o preço de fechamento de ontem é maior que o de anteontem, o preço de fechamento de hoje é menor que o de ontem, e a linha K rápida de 9 períodos está acima de 50, opera-se vendido.

-

Estratégia de Índice de Momentum Relativo (RMI)

- O RMI é uma variante do RSI que incorpora o fator momentum. Sua fórmula é: RMI = (SMA do momentum ascendente) / (SMA do momentum descendente) × 100.

- Quando o RMI está abaixo da linha de sobrecompra, opera-se comprado; quando o RMI está acima da linha de sobrevenda, opera-se vendido.

Esta estratégia combinada só gera um sinal de negociação quando os sinais duplos da Reversão 123 e do RMI estão na mesma direção. Isso pode reduzir efetivamente as oportunidades de negociação errôneas.

Análise de Vantagens da Estratégia

A estratégia apresenta as seguintes vantagens:

- Combina indicadores duplos, aumentando a precisão dos sinais.

- Utiliza estratégia de reversão, adequada para mercados laterais.

- O indicador RMI é sensível e pode identificar pontos de inflexão em tendências fortes.

Análise de Riscos da Estratégia

A estratégia também apresenta alguns riscos:

- A filtragem dupla pode perder algumas oportunidades de negociação.

- Os sinais de reversão podem ser interpretados erroneamente.

- Configurações inadequadas dos parâmetros do RMI podem afetar o desempenho.

Esses riscos podem ser reduzidos ajustando as combinações de parâmetros e otimizando os métodos de cálculo dos indicadores.

Direções de Otimização da Estratégia

A estratégia ainda pode ser otimizada nos seguintes aspectos:

- Testar diferentes combinações de parâmetros para encontrar os parâmetros ideais.

- Experimentar diferentes combinações de indicadores de reversão, como KDJ, MACD, etc.

- Ajustar a fórmula do RMI para torná-la mais sensível.

- Adicionar mecanismo de stop loss para controlar perdas individuais.

- Combinar com volume de negociação para evitar sinais falsos.

Conclusão

A Estratégia de Índice de Momentum com Dupla Reversão, através da filtragem de sinais duplos e otimização de parâmetros, pode efetivamente aumentar a precisão das decisões de negociação e reduzir a probabilidade de sinais falsos. Ela é adequada para mercados laterais e pode explorar oportunidades de reversão. A estratégia pode ser ainda mais aprimorada em termos de efeito e gerenciamento de riscos ajustando os parâmetros e otimizando os métodos de cálculo dos indicadores.

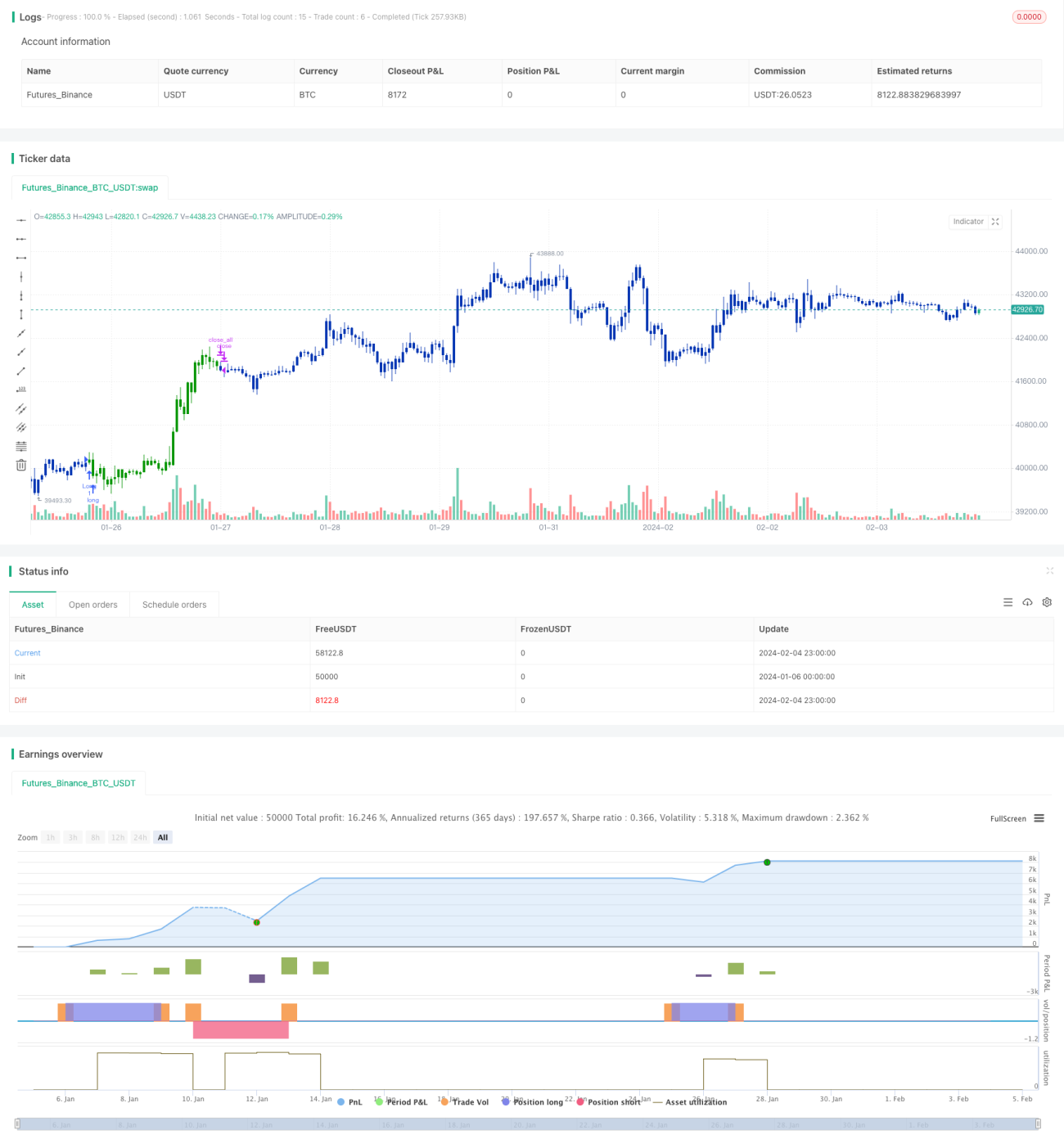

/*backtest

start: 2024-01-06 00:00:00

end: 2024-02-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 07/06/2021

// This is combo strategies for get a cumulative signal. - 1