Estratégia de Negociação com Linha de Tendência de Inclinação Dinâmica

Visão Geral

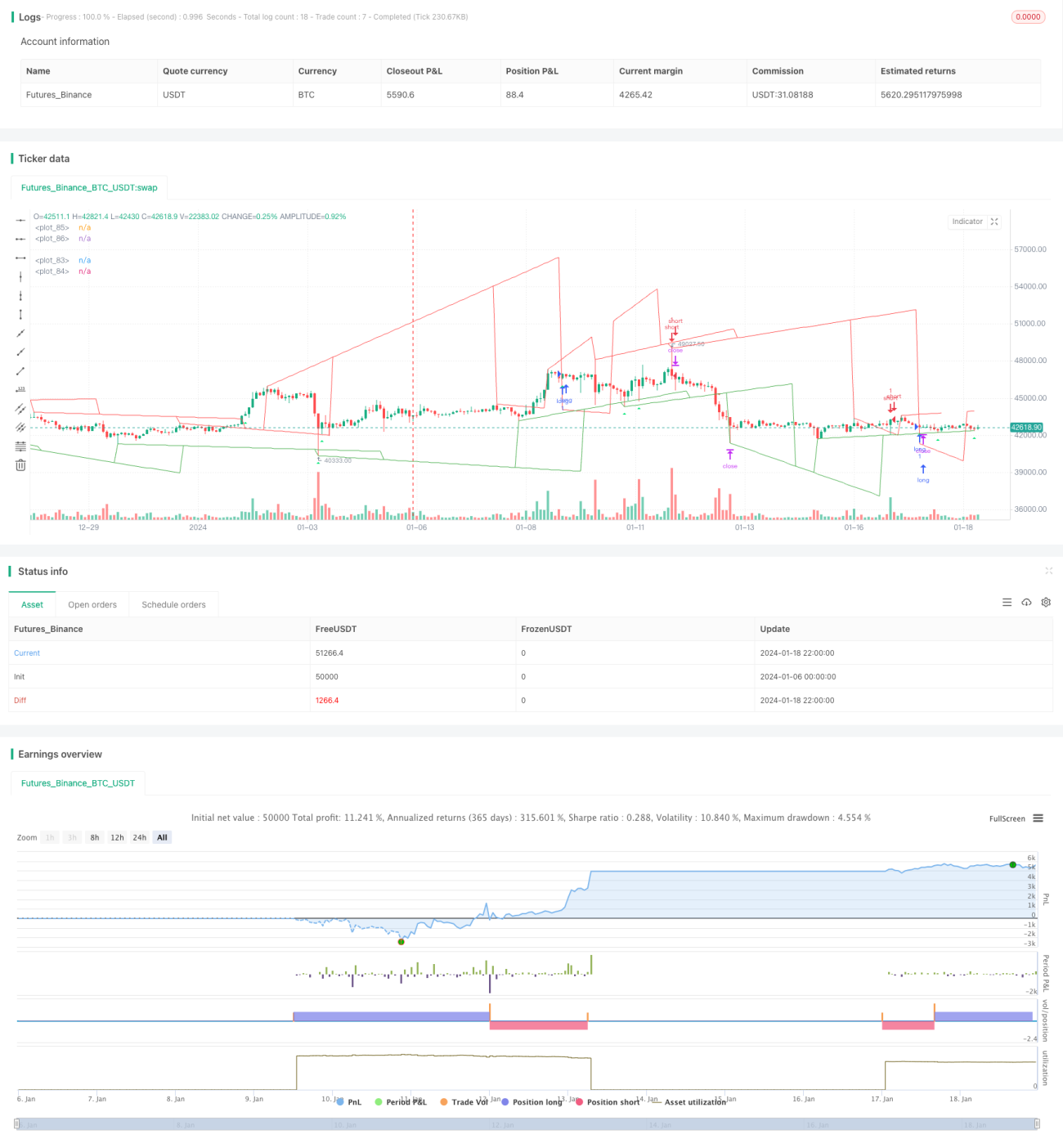

A ideia central desta estratégia é utilizar a inclinação dinâmica para julgar a direção da tendência dos preços, combinando com a quebra de níveis para gerar sinais de negociação. Especificamente, ela acompanha em tempo real as novas máximas e mínimas dos preços, calcula a inclinação dinâmica com base nas variações de preço em diferentes períodos e, em seguida, combina a quebra da linha de tendência pelo preço para determinar os sinais de compra e venda.

Princípio da Estratégia

Esta estratégia é dividida principalmente nas seguintes etapas:

-

Identificar Máximas e Mínimas: Acompanhar a máxima e a mínima dentro de um determinado período (ex.: 20 candles) e verificar se novas máximas ou mínimas são formadas.

-

Calcular a Inclinação Dinâmica: Registrar o número do candle onde ocorreu a nova máxima ou mínima e calcular a inclinação dinâmica do ponto da nova máxima/mínima até um ponto após um determinado período (ex.: 9 candles).

-

Desenhar Linhas de Tendência: Com base na inclinação dinâmica, desenhar linhas de tendência de alta e de baixa.

-

Prolongar e Atualizar Linhas de Tendência: Quando o preço rompe uma linha de tendência, esta é prolongada e atualizada.

-

Sinais de Negociação: Combinar a quebra das linhas de tendência pelo preço para determinar os sinais de compra (long) e venda (short).

Vantagens da Estratégia

Esta estratégia possui as seguintes vantagens:

-

Julga dinamicamente a direção da tendência, adaptando-se com flexibilidade às mudanças do mercado.

-

Permite controlar razoavelmente o stop loss, com baixo drawdown.

-

Sinais de negociação de breakout são claros e fáceis de implementar.

-

Parâmetros customizáveis, alta adaptabilidade.

-

Estrutura de código clara, fácil de entender e fazer desenvolvimento secundário.

Riscos e Soluções

Esta estratégia também apresenta alguns riscos:

-

Em mercado lateral (range), os sinais podem ser falsos; recomenda-se adicionar filtros.

-

Podem ocorrer muitos sinais falsos de breakout; ajustar os parâmetros ou adicionar condições de filtro pode ajudar.

-

Risco de stop loss durante movimentos bruscos de preço; pode-se aumentar a distância do stop loss.

-

Espaço de otimização limitado, lucratividade restrita; adequada para negociação de curto prazo.

Direções de Otimização

Os pontos onde esta estratégia pode ser otimizada incluem:

-

Adicionar mais indicadores técnicos para filtrar os sinais.

-

Otimizar a combinação de parâmetros para encontrar os melhores valores.

-

Testar melhorias na estratégia de stop loss para reduzir riscos.

-

Adicionar funcionalidade de ajuste automático da amplitude de entrada.

-

Tentar combinar com outras estratégias para explorar mais oportunidades.

Resumo

Em suma, esta estratégia é uma estratégia de curto prazo eficiente baseada na inclinação dinâmica para identificar tendências e operar breakouts. Ela possui boa precisão nos sinais, risco controlável e é adequada para capturar oportunidades de curto prazo no mercado. Com a otimização adicional dos parâmetros e a inclusão de filtros, é possível melhorar a taxa de acerto e o nível de lucro da estratégia.

/*backtest

start: 2024-01-06 00:00:00

end: 2024-01-19 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © pune3tghai

//Originally posted by matsu_bitmex- 1