Estratégia de negociação baseada no Índice de Força Relativa (RSI) e no Índice de Força Relativa Estocástico (StochRSI)

Visão Geral

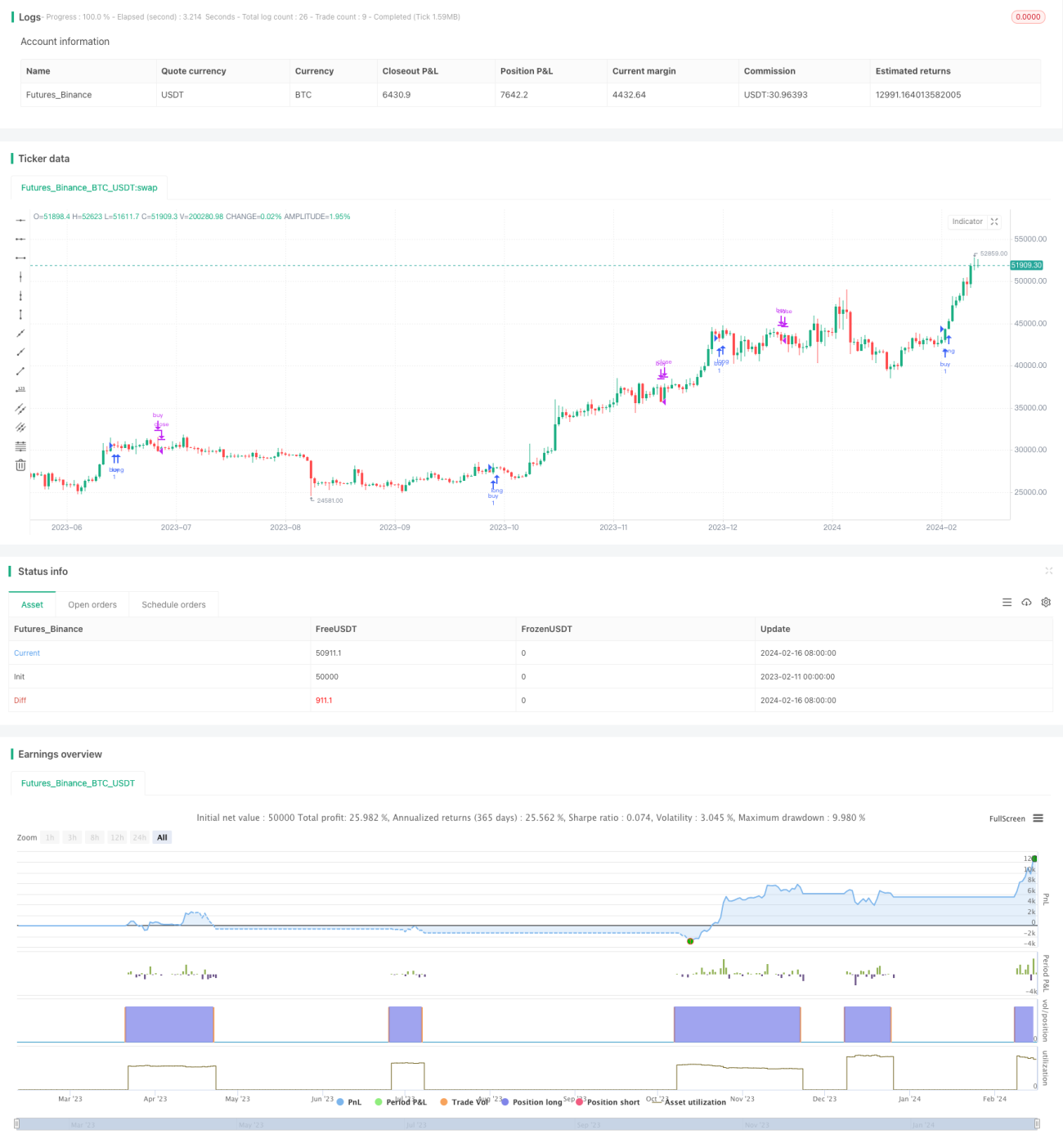

Esta estratégia de negociação combina o uso de dois indicadores técnicos, o Índice de Força Relativa (RSI) e o Estocástico do RSI (Stochastic RSI), para gerar sinais de negociação. A estratégia utiliza adicionalmente a movimentação de preços de criptomoedas em um timeframe superior para confirmar a tendência, aumentando a confiabilidade dos sinais.

Nome da Estratégia

Estratégia de Negociação RSI-SRSI Multi Timeframe (Multi Timeframe RSI-SRSI Trading Strategy)

Princípio da Estratégia

A estratégia julga as condições de sobrecompra e sobrevenda com base nos valores do indicador RSI. Quando o RSI está abaixo de 30, é um sinal de sobrevenda; acima de 70, é um sinal de sobrecompra. O Estocástico do RSI observa a volatilidade do próprio indicador RSI. Quando o Estocástico do RSI está abaixo de 5, é um sinal de sobrevenda; acima de 50, é um sinal de sobrecompra.

A estratégia também combina a movimentação de preços de criptomoedas em um timeframe superior (por exemplo, semanal). Somente quando o RSI do timeframe superior está acima de um limite (por exemplo, 45) é que um sinal de compra é gerado. Essa configuração filtra sinais de sobrevenda não persistentes que ocorrem durante uma tendência geral de queda.

Os sinais de compra e venda, após serem acionados, precisam ser confirmados ao longo de um certo período (por exemplo, 8 candles) para evitar sinais enganosos.

Vantagens da Estratégia

- Utiliza o método clássico de análise técnica do indicador RSI para identificar sobrecompra e sobrevenda

- Combina o Estocástico do RSI para detectar sinais de reversão do próprio RSI

- Aplica a técnica de múltiplos timeframes para filtrar sinais enganosos, melhorando a qualidade dos sinais

Riscos da Estratégia e Soluções

- O indicador RSI é propenso a gerar sinais falsos

- Combinar com outros indicadores para filtrar sinais enganosos

- Aplicar técnicas de confirmação de tendência

- Parâmetros de limite mal ajustados podem gerar muitos sinais de negociação

- Otimizar a combinação de parâmetros para encontrar os melhores

- Os sinais de compra e venda exigem um certo tempo de confirmação

- Encontrar um período de confirmação equilibrado que filtre sinais enganosos sem perder oportunidades

Direções de Otimização da Estratégia

- Testar mais combinações de indicadores para buscar sinais mais fortes

- Por exemplo, adicionar o indicador MACD à estratégia

- Tentar métodos de aprendizado de máquina para encontrar parâmetros ótimos

- Utilizar algoritmos genéticos/algoritmos evolutivos para otimização automática

- Adicionar uma estratégia de stop loss para controlar o risco de cada operação

- Parar a perda quando o preço romper o suporte

Resumo

Esta estratégia baseia-se principalmente nos dois indicadores clássicos RSI e Estocástico do RSI para gerar sinais de negociação. Ao mesmo tempo, a introdução de um timeframe superior para confirmação de tendência filtra efetivamente sinais enganosos, melhorando a qualidade dos sinais. Através da otimização de parâmetros, estratégias de stop loss e outros meios, é possível aprimorar ainda mais o desempenho da estratégia. A lógica é simples e direta, fácil de entender e implementar, sendo um excelente ponto de partida para negociação quantitativa.

- 1