Estratégia de Seguimento de Tendência com Gaussian Channel

Visão Geral

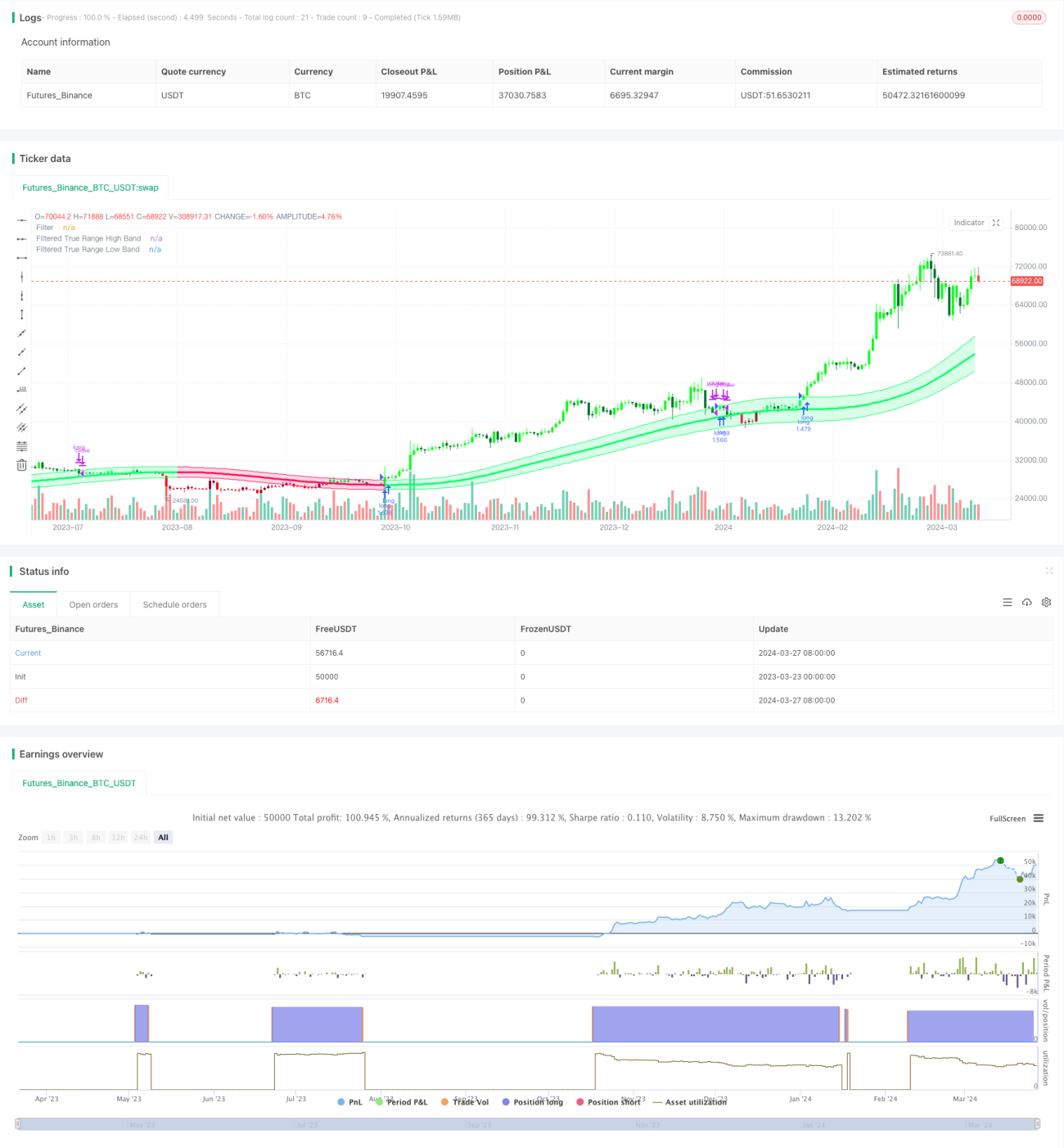

A Estratégia de Rastreamento de Tendência com Canal Gaussiano é uma estratégia de negociação baseada no indicador Gaussian Channel para acompanhar tendências. O objetivo da estratégia é capturar a principal tendência do mercado, comprando e mantendo posições durante uma tendência de alta, e fechando posições e aguardando durante uma tendência de baixa. A estratégia utiliza o indicador Gaussian Channel para identificar a direção e a força da tendência, analisando a relação entre o preço e as bandas superior e inferior do canal para determinar momentos de compra e venda. O principal objetivo é obter o máximo de lucro possível durante a persistência da tendência, evitando ao máximo negociações frequentes em mercados laterais.

Princípio da Estratégia

O núcleo da Estratégia de Rastreamento de Tendência com Canal Gaussiano é o indicador Gaussian Channel, proposto por Ehlers, que combina a técnica de filtragem gaussiana com o True Range (Variação Verdadeira) como ferramenta de análise de tendência. O indicador primeiro calcula os valores β e α com base no período da amostra e no número de polos, depois aplica um filtro nos dados para obter uma curva suave (banda central). Em seguida, a estratégia multiplica o True Range suavizado por um multiplicador para obter as bandas superior e inferior. Quando o preço cruza para cima/para baixo a banda superior/inferior, gera-se um sinal de compra/venda. Além disso, a estratégia oferece funções para reduzir a latência do indicador e um modo de reação rápida.

Vantagens da Estratégia

- Rastreamento de Tendência: A estratégia é eficaz em capturar as principais tendências do mercado, investindo na direção da tendência, o que ajuda a obter retornos estáveis a longo prazo.

- Redução da Frequência de Negociação: A estratégia só entra no mercado quando a tendência é confirmada, mantendo a posição durante a duração da tendência, reduzindo assim o número de negociações desnecessárias e os custos de transação.

- Redução de Latência: Através do modo de redução de latência e do modo de reação rápida, a estratégia pode responder mais rapidamente às mudanças do mercado.

- Parâmetros Flexíveis: Os usuários podem ajustar os parâmetros da estratégia de acordo com suas necessidades, como período da amostra, número de polos, multiplicador do True Range, etc., para otimizar o desempenho.

Riscos da Estratégia

- Risco de Otimização de Parâmetros: Configurações inadequadas de parâmetros podem levar a um desempenho insatisfatório. Recomenda-se realizar otimização de parâmetros e backtesting em diferentes condições de mercado para encontrar a melhor combinação.

- Risco de Reversão de Tendência: Quando a tendência do mercado sofre uma reversão abrupta, a estratégia pode gerar grandes retrações. O risco pode ser controlado através da definição de stop loss ou da introdução de outros indicadores.

- Risco de Mercado Lateral: Em um mercado lateral, a estratégia pode gerar sinais de negociação frequentes, prejudicando os lucros. Isso pode ser mitigado otimizando os parâmetros ou combinando com outros indicadores técnicos para filtrar sinais.

Direções de Otimização da Estratégia

- Introdução de Outros Indicadores Técnicos: Combinar com indicadores de tendência ou osciladores, como MACD, RSI, etc., para melhorar a precisão e confiabilidade dos sinais.

- Otimização Dinâmica de Parâmetros: Ajustar dinamicamente os parâmetros da estratégia de acordo com as mudanças nas condições do mercado para se adaptar a diferentes ambientes.

- Adição de Módulo de Controle de Risco: Definir regras razoáveis de stop loss e take profit para controlar o risco de cada negociação e o nível geral de retração.

- Análise de Múltiplos Timeframes: Combinar sinais de diferentes períodos de tempo, como diário, 4 horas, etc., para obter informações de mercado mais abrangentes.

Resumo

A Estratégia de Rastreamento de Tendência com Canal Gaussiano é uma estratégia baseada na técnica de filtragem gaussiana para rastreamento de tendências, capturando a principal tendência do mercado para obter retornos estáveis a longo prazo. A estratégia utiliza o indicador Gaussian Channel para identificar a direção e a força da tendência, oferecendo funções de redução de latência e reação rápida. Suas vantagens residem na boa capacidade de rastreamento de tendências e na baixa frequência de negociação, mas também enfrenta riscos como otimização de parâmetros, reversão de tendência e mercado lateral. No futuro, a estratégia pode ser otimizada através da introdução de outros indicadores técnicos, otimização dinâmica de parâmetros, adição de módulo de controle de risco e análise de múltiplos timeframes, a fim de aumentar sua robustez e rentabilidade.

/*backtest

start: 2023-03-23 00:00:00

end: 2024-03-28 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Gaussian Channel Strategy v2.0", overlay=true, calc_on_every_tick=false, initial_capital=1000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.1, slippage=3)

//------------------------------------------------------------------------------------------------------------------------------------------------------------------ 1