Стратегия количественной торговли на основе множества технических индикаторов

Обзор

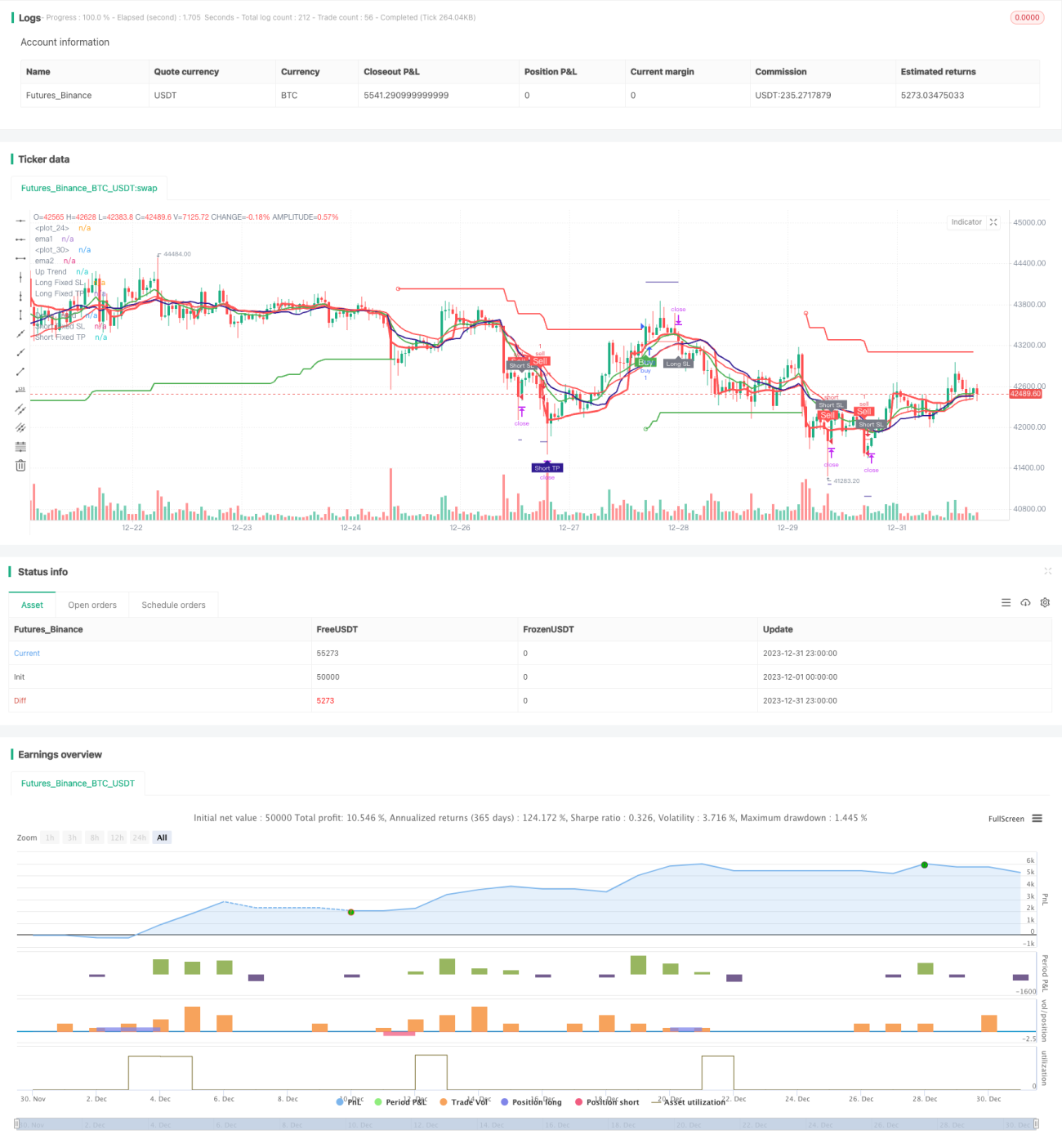

Данная стратегия представляет собой количественную торговую стратегию, использующую несколько технических индикаторов. Основные сигналы формируются на основе комбинации таких индикаторов, как пересечение скользящих средних EMA, индикатор SuperTrend, RSI и MACD.

Принцип стратегии

Основная торговая логика стратегии основана на следующих аспектах:

-

Пересечение EMA: рассчитываются быстрая линия EMA1 и медленная линия EMA2. Когда быстрая линия пересекает медленную снизу вверх, генерируется сигнал на покупку; при пересечении сверху вниз — сигнал на продажу.

-

VWMA: рассчитывается линия VWMA. Когда цена закрытия пересекает её снизу вверх, это считается сигналом на покупку; при пересечении сверху вниз — сигналом на продажу.

-

SuperTrend: на основе ATR и множителя (multiplier) вычисляются верхняя и нижняя границы SuperTrend, определяется направление тренда. В восходящем тренде генерируется сигнал на покупку, в нисходящем — на продажу.

-

RSI: рассчитывается индикатор RSI. Когда RSI превышает уровень перекупленности, это сигнал на продажу; когда RSI опускается ниже уровня перепроданности — сигнал на покупку.

-

MACD: рассчитываются быстрая, медленная линии и сигнальная линия MACD. Когда быстрая линия пересекает сигнальную снизу вверх, генерируется сигнал на покупку; при пересечении сверху вниз — сигнал на продажу.

После получения сигналов от вышеперечисленных индикаторов стратегия использует логику «И» (AND): окончательные сигналы на покупку и продажу генерируются только при одновременном совпадении сигналов от нескольких индикаторов.

Преимущества стратегии

Данная стратегия, объединяя несколько индикаторов для оценки рынка, позволяет эффективно снизить количество ложных сигналов. Основные преимущества:

-

Комплексная фильтрация с использованием нескольких индикаторов уменьшает количество ошибочных сигналов от одного индикатора.

-

Сочетание трендовых и осцилляторных индикаторов позволяет получать дополнительную прибыль в трендовых движениях.

-

Реализована логика стоп-лосса, которая эффективно ограничивает максимальный убыток по одной сделке.

-

Логика мартингейла (удвоения ставки) позволяет после убыточной сделки вернуть потери за счёт увеличения позиции.

Риски стратегии

Основные риски стратегии:

-

Комбинация множества индикаторов может быть слишком консервативной, что приведёт к пропуску части торговых возможностей. Возможно упрощение комбинации индикаторов.

-

Логика мартингейла может привести к увеличению убытков. Следует разумно ограничить количество шагов увеличения позиции.

-

Неправильная установка уровня стоп-лосса может привести к неоправданным потерям. Рекомендуется внедрить адаптивный стоп-лосс.

-

Неоптимальные параметры индикаторов могут генерировать избыточное количество ложных сигналов. Необходимо оптимизировать параметры для получения наилучшей комбинации.

Направления оптимизации стратегии

Стратегию можно дополнительно оптимизировать по следующим направлениям:

-

Оценка эффективности различных комбинаций параметров индикаторов и подбор весов для каждого индикатора.

-

Тестирование различных настроек параметров индикаторов.

-

Добавление адаптивной логики стоп-лосса.

-

Внедрение динамического управления размером позиции.

-

Использование методов машинного обучения для оптимизации параметров и модели.

Заключение

В целом, данная стратегия является весьма практичной количественной торговой стратегией. Она объединяет преимущества нескольких классических технических индикаторов и позволяет эффективно оценивать рыночную ситуацию. Путём оптимизации параметров и итерации модели можно добиться лучших торговых результатов.

- 1