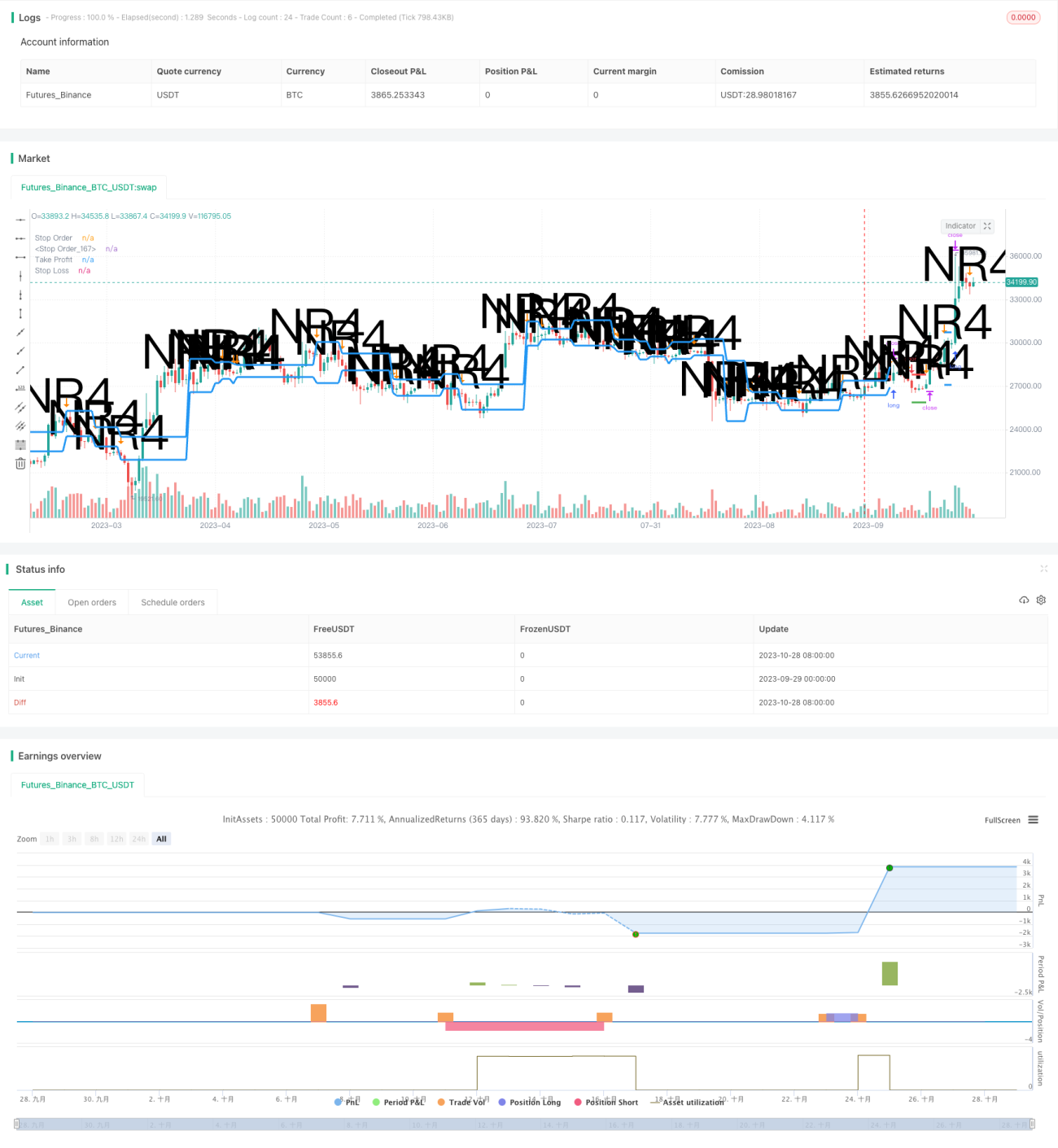

غیر فعال رینج ریورسل حکمت عملی

خلاصہ

سلیپ رینج ریورسل حکمت عملی قیمت کے اتار چڑھاؤ میں کمی کے ادوار کو پوزیشن کھولنے کے سگنل کے طور پر استعمال کرتی ہے، اور جب قیمت کا اتار چڑھاؤ دوبارہ بڑھتا ہے تو منافع کماتے ہوئے پوزیشن بند کرتی ہے۔ یہ ان حالات کی نشاندہی کرکے جہاں قیمت ایک تنگ سلیپ رینج میں محدود ہوتی ہے، آنے والے قیمت کے رجحان کو پکڑتی ہے۔ یہ حکمت عملی عام طور پر اس وقت موزوں ہوتی ہے جب موجودہ اتار چڑھاؤ کم ہو لیکن مستقبل میں پھٹنے کا امکان ہو۔

حکمت عملی کا اصول

حکمت عملی پہلے سلیپ رینج کی شناخت کرتی ہے، یعنی وہ صورت حال جہاں قیمت پچھلے تجارتی دن کی قیمت کی حد کے اندر محدود ہو۔ یہ ظاہر کرتا ہے کہ موجودہ اتار چڑھاؤ پچھلے دنوں کے مقابلے میں کم ہے۔ ہم موجودہ تجارتی دن کی اونچائی کا n دن پہلے (عام طور پر 4 دن) کی اونچائی سے موازنہ کرکے، اور موجودہ تجارتی دن کی نیچی کا n دن پہلے کی نیچی سے موازنہ کرکے اس بات کا تعین کرتے ہیں کہ آیا سلیپ رینج کی شرط پوری ہوتی ہے۔

سلیپ رینج کی تصدیق ہونے کے بعد، حکمت عملی ایک ساتھ دو آرڈر لگاتی ہے: ایک خرید آرڈر رینج کی اونچائی کے قریب، اور ایک فروخت آرڈر رینج کی نیچی کے قریب۔ پھر قیمت کے سلیپ رینج سے اوپر یا نیچے ٹوٹنے کا انتظار کیا جاتا ہے۔ اگر قیمت اوپر ٹوٹتی ہے تو خرید آرڈر متحرک ہو کر لمبی پوزیشن بناتا ہے؛ اگر نیچے ٹوٹتی ہے تو فروخت آرڈر متحرک ہو کر چھوٹی پوزیشن بناتا ہے۔

پوزیشن بنانے کے بعد، حکمت عملی سٹاپ لاس اور ٹیک پروفٹ آرڈر سیٹ کرتی ہے۔ سٹاپ لاس نیچے کی طرف خطرے کو محدود کرتا ہے، جبکہ ٹیک پروفٹ منافع حاصل کرنے کے بعد پوزیشن بند کرنے کے لیے استعمال ہوتا ہے۔ سٹاپ لاس داخلے کی قیمت سے ایک تناسب کے فاصلے پر رکھا جاتا ہے، جو رسک مینجمنٹ پیرامیٹر کے ذریعے طے ہوتا ہے؛ ٹیک پروفٹ داخلے کی قیمت سے سلیپ رینج کے سائز کے برابر فاصلے پر رکھا جاتا ہے، کیونکہ ہم توقع کرتے ہیں کہ قیمت کی حرکت کی حد پچھلے اتار چڑھاؤ کے مطابق ہوگی۔

آخر میں، اس حکمت عملی میں فنڈ مینجمنٹ ماڈیول بھی شامل ہے۔ فکسڈ ملٹیپل طریقہ استعمال کرتے ہوئے آرڈر کی تجارتی رقم کو ایڈجسٹ کیا جاتا ہے، منافع میں فنڈ کے استعمال کی کارکردگی بڑھتی ہے اور نقصان میں خطرہ کم ہوتا ہے۔

فوائد کا تجزیہ

اس حکمت عملی کے درج ذیل فوائد ہیں:

- اتار چڑھاؤ میں کمی کے لمحے کو پوزیشن کھولنے کے سگنل کے طور پر استعمال کرکے قیمت کے رجحان سے پہلے موقع پکڑنا۔

- بیک وقت لمبی اور چھوٹی دونوں سمتوں میں آرڈر رکھ کر اوپر یا نیچے کے رجحان کو پکڑنا۔

- سٹاپ لاس اور ٹیک پروفٹ کی حکمت عملی سے ایک ہی تجارت میں خطرے کو مؤثر طریقے سے کنٹرول کرنا۔

- فکسڈ ملٹیپل فنڈ مینجمنٹ طریقہ سے فنڈ کے استعمال کی کارکردگی بڑھانا۔

- حکمت عملی کی منطق سادہ اور واضح ہے، جسے آسانی سے نافذ کیا جا سکتا ہے۔

خطرات کا تجزیہ

اس حکمت عملی میں کچھ خطرات بھی ہیں جن پر توجہ دینے کی ضرورت ہے:

- سلیپ رینج کے ٹوٹنے کی سمت کا غلط اندازہ لگانے کا خطرہ۔ قیمت اوپر یا نیچے واضح طور پر نہ ٹوٹے، جس کی وجہ سے غلط سمت میں داخلہ ہو سکتا ہے۔

- ٹوٹنے کے بعد رجحان جاری نہ رہنے کا خطرہ۔ ٹوٹنا محض ایک قلیل مدتی ریورسل ہو سکتا ہے۔

- سٹاپ لاس ٹوٹنے کا خطرہ۔ بہت بڑی قیمت کی حرکت براہ راست سٹاپ لاس کو پار کر سکتی ہے۔

- فکسڈ ملٹیپل طریقہ سے پوزیشن بڑھانے پر نقصان بڑھنے کا خطرہ۔ فکسڈ ملٹیپل ویلیو کم کرکے خطرہ کم کیا جا سکتا ہے۔

- پیرامیٹرز کی نامناسب ترتیب سے حکمت عملی کی کارکردگی متاثر ہو سکتی ہے۔

بہتری کی سمت

اس حکمت عملی کو درج ذیل پہلوؤں سے بہتر بنایا جا سکتا ہے:

- غلط بریک آؤٹ سے بچنے کے لیے بریک آؤٹ ڈائیورجنس جیسے فلٹر سگنلز شامل کرنا۔

- سٹاپ لاس حکمت عملی کو بہتر بنانا، جیسے ٹریلنگ سٹاپ، ہینگنگ سٹاپ وغیرہ۔

- رجحان کی نشاندہی کرنے والے انڈیکیٹرز شامل کرنا تاکہ ریورسل میں داخلے سے بچا جا سکے۔

- فکسڈ ملٹیپل ویلیو کو بہتر بنانا تاکہ منافع اور نقصان کے تناسب کو متوازن کیا جا سکے۔

- متعدد ٹائم فریموں کے تجزیے کو ملا کر منافع کے امکانات بڑھانا۔

- مشین لرننگ طریقوں سے خودکار طور پر پیرامیٹرز کو بہتر بنانا۔

خلاصہ

سلیپ رینج ریورسل حکمت عملی کا مجموعی تصور واضح ہے اور اس میں منافع کی صلاحیت موجود ہے۔ پیرامیٹر آپٹیمائزیشن، رسک مینجمنٹ، اور سگنل فلٹرنگ جیسے ذرائع سے حکمت عملی کے استحکام کو مزید بہتر بنایا جا سکتا ہے۔ تاہم، ریورسل کی کسی بھی حکمت عملی میں کچھ خطرات ہوتے ہیں، اسے احتیاط سے استعمال کرنا چاہیے اور پوزیشن کے سائز کو مناسب طور پر ایڈجسٹ کرنا چاہیے۔ یہ حکمت عملی ان تاجروں کے لیے موزوں ہے جو ریورسل آپریشنز سے آشنا ہوں اور خطرے سے آگاہ ہوں۔

- 1