Chiến lược mua vào khi điều chỉnh giảm

Tổng quan

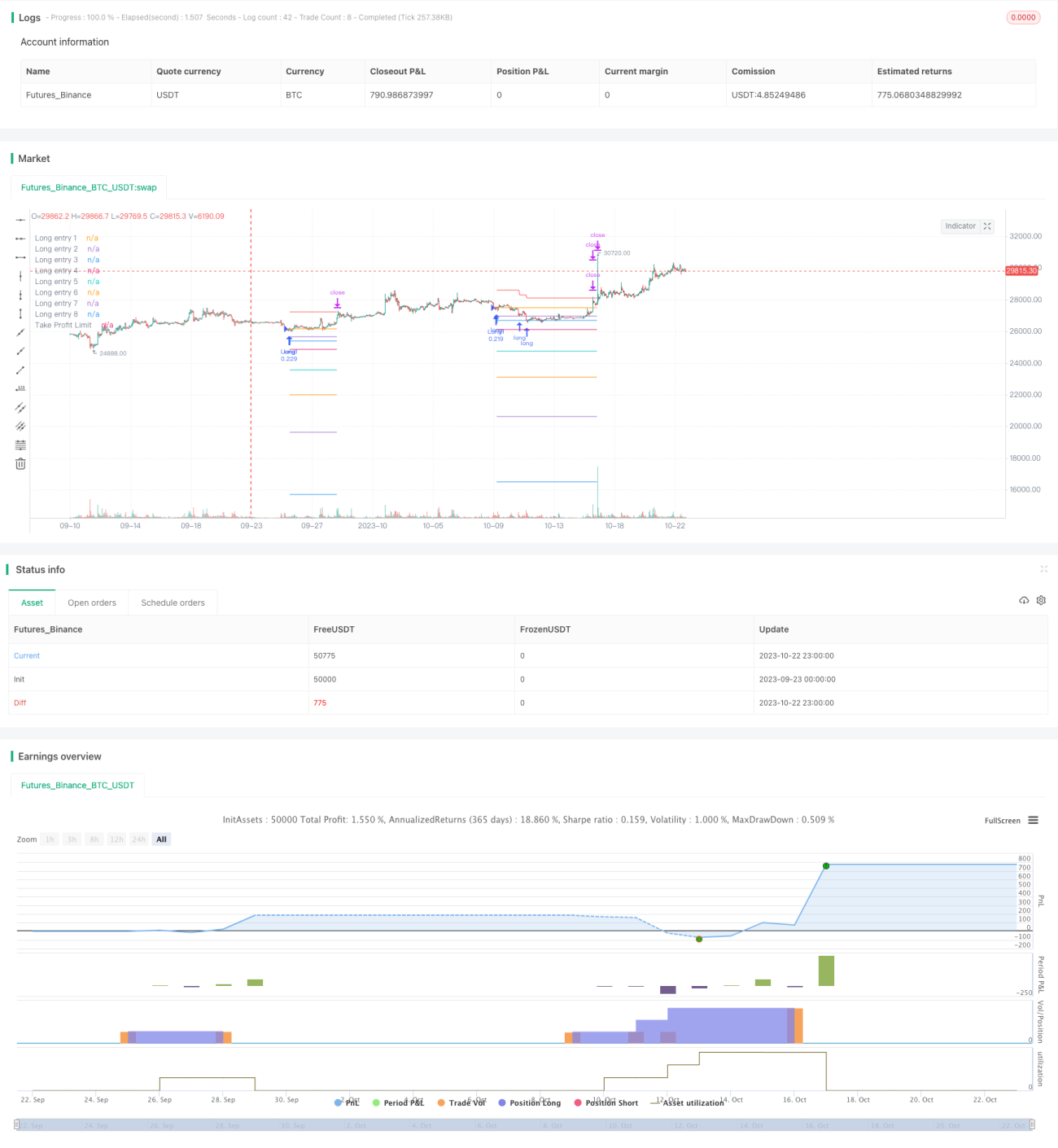

Chiến lược này kết hợp chỉ báo RSI và đường trung bình giá, tìm kiếm cơ hội quá bán để mở vị thế mua khi giá cổ phiếu phá vỡ xuống dưới đường trung bình. Khi giá tiếp tục giảm, chiến lược sẽ tăng dần vị thế theo các mức phần trăm được cài đặt sẵn nhằm mục đích làm trung bình chi phí nắm giữ. Khi lợi nhuận của vị thế đạt đến mức chốt lời được cấu hình, chiến lược sẽ chọn đóng vị thế. Đồng thời, chiến lược đưa vào cơ chế chốt lời dần dần, dựa trên lợi nhuận đã thực hiện của từng lô vị thế để điều chỉnh giá chốt lời của toàn bộ danh mục. Điều này có thể giảm thiểu rủi ro thua lỗ một cách hiệu quả và thực hiện thoát lệnh dần dần.

Nguyên lý chiến lược

-

Khi chỉ báo RSI thấp hơn ngưỡng quá bán 29 và giá đóng cửa thấp hơn đường trung bình, mở lệnh mua đầu tiên.

-

Khi giá giảm 2% so với lệnh đầu tiên, thêm lệnh mua; khi giảm 3% thì thêm lần thứ ba, cứ thế tối đa 8 lần thêm lệnh. Điều này tạo hiệu ứng xây dựng vị thế theo từng đợt.

-

Sau mỗi lần mở lệnh, ghi lại giá mở lệnh tại thời điểm đó. Các mức giá này là các mức tham chiếu để vào lệnh. Vẽ các đường giá này trên biểu đồ.

-

Sau khi mở vị thế, tính toán giá trung bình của vị thế. Lấy 3% giá trung bình làm mức chốt lời cho từng lô, 4% làm mức chốt lời cho toàn bộ danh mục.

-

Khi giá tăng vượt quá mức chốt lời của một lô vị thế nào đó, chọn đóng lô vị thế đó.

-

Cách tính chốt lời dần dần: mỗi khi đóng một lô, sẽ trừ đi lợi nhuận thực hiện của lô đó khỏi giá chốt lời tổng thể. Điều này làm cho đường chốt lời giảm dần, chỉ khi lợi nhuận của tất cả các lô đủ bù đắp khoản lỗ tối đa thì mới chốt lời toàn bộ.

-

Khi giá chạm đường chốt lời dần dần, chọn đóng toàn bộ vị thế.

Phân tích ưu điểm

-

Chỉ báo RSI có thể đánh giá khá chính xác vùng quá bán, hữu ích để nắm bắt cơ hội đảo chiều.

-

Việc tăng vị thế nhiều lần cho phép làm trung bình chi phí nắm giữ tại các điểm thấp.

-

Chốt lời dần dần có thể giảm thiểu rủi ro thua lỗ, thực hiện thoát lệnh từ từ. Ngay cả khi có thua lỗ cũng có thể kiểm soát trong phạm vi nhất định.

-

Các tỷ lệ chốt lời và tỷ lệ tăng vị thế có thể cấu hình, cho phép điều chỉnh rủi ro của chiến lược theo thị trường.

-

Vẽ các đường tham chiếu mở lệnh và đường chốt lời trên biểu đồ, giúp trực quan hóa phân bố vị thế.

Phân tích rủi ro

-

Trong thị trường dao động, có thể kích hoạt nhiều lần mở và đóng vị thế, giao dịch thường xuyên gây tổn thất do trượt giá. Có thể nới lỏng tham số RSI để giảm số lần giao dịch.

-

Việc thiết lập số lần và tỷ lệ tăng vị thế không phù hợp có thể dẫn đến giao dịch quá mức, cần cấu hình thận trọng dựa trên tình hình vốn.

-

Nếu thị trường tiếp tục giảm và tăng vị thế, có thể đối mặt với rủi ro lỗ vô đáy. Nên đặt giới hạn trên cho số lần tăng vị thế và tỷ lệ tăng vị thế cuối cùng thận trọng.

-

Nếu tỷ lệ chốt lời đặt quá nhỏ, có thể dẫn đến chốt lời quá sớm. Nên đặt tỷ lệ chốt lời phù hợp dựa trên dữ liệu backtest lịch sử.

Hướng tối ưu hóa

-

Có thể đưa vào các chỉ báo như MACD để lọc tín hiệu RSI, giảm giao dịch không hiệu quả.

-

Có thể đặt stop loss dựa trên ATR để tránh thua lỗ lớn trong các tình huống thị trường cực đoan.

-

Có thể tối ưu hóa các tham số như số lần tăng vị thế, tỷ lệ, tỷ lệ chốt lời để chiến lược thích ứng với các loại tài sản khác nhau.

-

Có thể điều chỉnh tỷ lệ chốt lời một cách thông minh dựa trên độ biến động, nới lỏng khi biến động lớn.

Tổng kết

Chiến lược này tận dụng triệt để chỉ báo RSI để xác định vùng quá bán, kết hợp với đường trung bình giá để thực hiện giao dịch đảo chiều. Đồng thời sử dụng cơ chế tăng vị thế thông minh và chốt lời dần dần, đạt được chiến lược mua hiệu quả trong khi kiểm soát rủi ro. Bằng cách tối ưu hóa các tham số chỉ báo, cơ chế chốt lời, v.v., có thể làm cho chiến lược ổn định và hiệu quả hơn. Chiến lược này có thể được áp dụng rộng rãi cho các sản phẩm tài chính có đặc điểm đảo chiều xu hướng như hợp đồng tương lai chỉ số, tiền điện tử, v.v., và có giá trị đầu tư thực tế.

- 1