Chiến lược đảo chiều phạm vi ngủ đông

Tổng quan

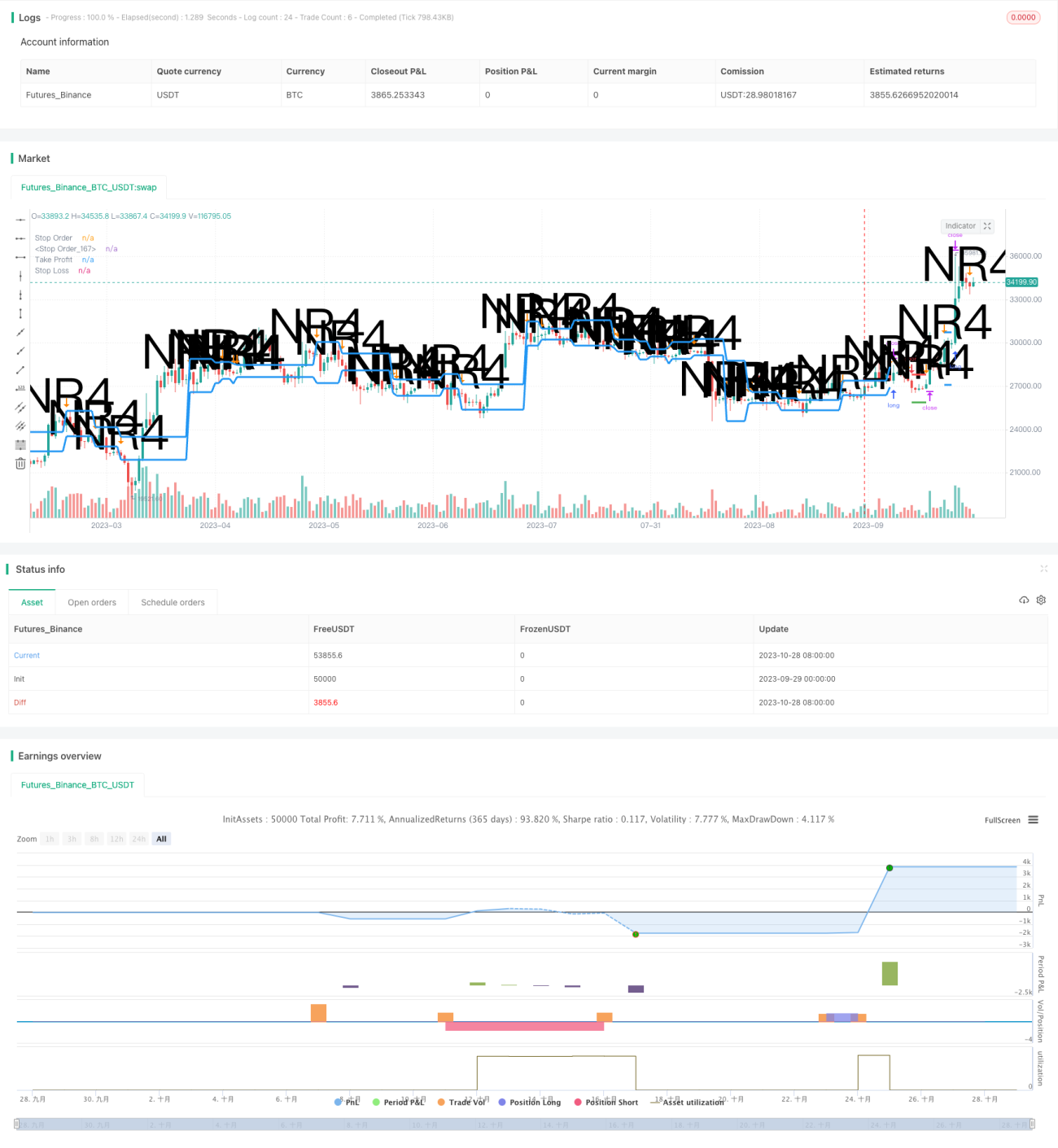

Chiến lược đảo chiều phạm vi ngủ đông tận dụng giai đoạn biến động giá thấp để làm tín hiệu mở lệnh, và đóng lệnh có lợi nhuận khi biến động giá tăng trở lại. Bằng cách xác định tình huống giá bị giới hạn trong phạm vi dao động hẹp (phạm vi ngủ đông), chiến lược này nắm bắt xu hướng giá sắp bùng nổ. Chiến lược thường áp dụng khi biến động hiện tại ở mức thấp nhưng có khả năng bùng nổ trong tương lai.

Nguyên lý chiến lược

Chiến lược trước hết xác định phạm vi ngủ đông, tức là tình huống giá bị giới hạn trong phạm vi giá của ngày giao dịch trước đó. Điều này cho thấy biến động hiện tại giảm so với vài ngày trước. Chúng ta so sánh giá cao nhất của phiên giao dịch hiện tại với giá cao nhất của n ngày trước (thường là 4 ngày), và giá thấp nhất của phiên hiện tại với giá thấp nhất của n ngày trước để xác định xem có thỏa mãn điều kiện phạm vi ngủ đông hay không.

Khi đã xác nhận phạm vi ngủ đông, chiến lược đồng thời đặt hai lệnh chờ: một lệnh mua đặt gần đỉnh phạm vi, một lệnh bán đặt gần đáy phạm vi. Sau đó chờ giá phá vỡ phạm vi ngủ đông để tiếp tục đi lên hoặc đi xuống. Nếu giá phá vỡ lên, lệnh mua sẽ được kích hoạt để mở vị thế Long; nếu phá vỡ xuống, lệnh bán sẽ được kích hoạt để mở vị thế Short.

Sau khi vào lệnh, chiến lược đặt lệnh dừng lỗ và chốt lời. Lệnh dừng lỗ giới hạn rủi ro giảm, lệnh chốt lời dùng để đóng lệnh khi có lợi nhuận. Khoảng cách dừng lỗ tính từ giá vào lệnh theo một tỷ lệ do tham số quản lý rủi ro thiết lập; khoảng cách chốt lời tính từ giá vào lệnh bằng kích thước phạm vi ngủ đông, vì chúng tôi kỳ vọng biên độ giá di chuyển tương đương với biến động trước đó.

Cuối cùng, chiến lược còn có mô-đun quản lý vốn. Sử dụng phương pháp tỷ lệ cố định để điều chỉnh khối lượng giao dịch, tăng hiệu suất sử dụng vốn khi có lợi nhuận, giảm rủi ro khi thua lỗ.

Phân tích ưu điểm

Chiến lược này có những ưu điểm sau:

-

Sử dụng thời điểm biến động giảm làm tín hiệu mở lệnh, có thể nắm bắt cơ hội trước khi xu hướng giá hình thành.

-

Đồng thời đặt lệnh hai chiều mua và bán, có thể nắm bắt xu hướng tăng hoặc giảm.

-

Áp dụng chiến lược dừng lỗ và chốt lời, có thể kiểm soát hiệu quả rủi ro từng giao dịch.

-

Sử dụng phương pháp quản lý vốn tỷ lệ cố định, nâng cao hiệu quả sử dụng vốn.

-

Logic chiến lược đơn giản, rõ ràng, dễ thực hiện.

Phân tích rủi ro

Chiến lược này cũng tồn tại một số rủi ro cần lưu ý:

-

Rủi ro xác định sai hướng phá vỡ phạm vi ngủ đông. Giá có thể phá vỡ lên hoặc xuống không rõ ràng, dẫn đến vào lệnh sai hướng.

-

Rủi ro sau khi phá vỡ không tiếp tục di chuyển theo hướng đó. Sự phá vỡ chỉ là hiện tượng đảo chiều ngắn hạn.

-

Rủi ro bị chạm dừng lỗ. Các biến động lớn có thể trực tiếp vượt qua mức dừng lỗ.

-

Rủi ro phương pháp tỷ lệ cố định làm mở rộng thua lỗ khi vào thêm lệnh. Có thể giảm giá trị tỷ lệ cố định để giảm rủi ro.

-

Thiết lập tham số không phù hợp có thể khiến hiệu quả chiến lược kém.

Hướng tối ưu

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

-

Thêm các bộ lọc tín hiệu như phân kỳ phá vỡ để tránh phá vỡ sai.

-

Cải thiện chiến lược dừng lỗ, ví dụ dừng lỗ động, dừng lỗ bằng lệnh chờ.

-

Thêm chỉ báo xác định xu hướng để tránh vào lệnh ngược hướng.

-

Tối ưu hóa giá trị tỷ lệ cố định, cân bằng tỷ lệ lời/lỗ.

-

Kết hợp phân tích nhiều khung thời gian để tăng xác suất có lợi nhuận.

-

Sử dụng phương pháp học máy để tự động tối ưu tham số.

Tổng kết

Chiến lược đảo chiều phạm vi ngủ đông có tư duy tổng thể rõ ràng và có tiềm năng lợi nhuận nhất định. Thông qua tối ưu tham số, quản lý rủi ro, lọc tín hiệu và các biện pháp khác có thể nâng cao tính ổn định của chiến lược. Tuy nhiên, bất kỳ chiến lược đảo chiều xu hướng nào cũng tồn tại rủi ro nhất định, cần sử dụng thận trọng và điều chỉnh quy mô vị thế phù hợp. Chiến lược này phù hợp với các nhà giao dịch quen thuộc với thao tác đảo chiều và có ý thức quản lý rủi ro.

- 1