Người theo dõi xu hướng đột phá V2

Tổng quan

Chiến lược này là một biến thể của chiến lược khác của tôi - chiến lược theo dõi đột phá xu hướng. Trong chiến lược kia, bạn có thể sử dụng đường trung bình động làm bộ lọc giao dịch (tức là, nếu giá thấp hơn đường trung bình động, nó sẽ không mua). Sau khi tạo ra công cụ phát hiện xu hướng khung thời gian cao hơn, tôi muốn xem liệu nó có thể là bộ lọc tốt hơn đường trung bình động hay không.

Do đó, chiến lược này cho phép bạn xem xu hướng của khung thời gian cao hơn (tức là có đỉnh cao hơn và đáy thấp hơn không? Nếu có, đó là xu hướng tăng). Bạn chỉ giao dịch theo hướng xu hướng. Bạn có thể chọn tối đa hai xu hướng làm bộ lọc. Mỗi hướng xu hướng được hiển thị trong bảng trên biểu đồ để tiện tham khảo. Các mức hỗ trợ và kháng cự hiện tại được vẽ trên biểu đồ, giúp bạn thấy khi nào có thể xảy ra đột phá khỏi xu hướng khung thời gian hiện tại và xu hướng cấp cao hơn.

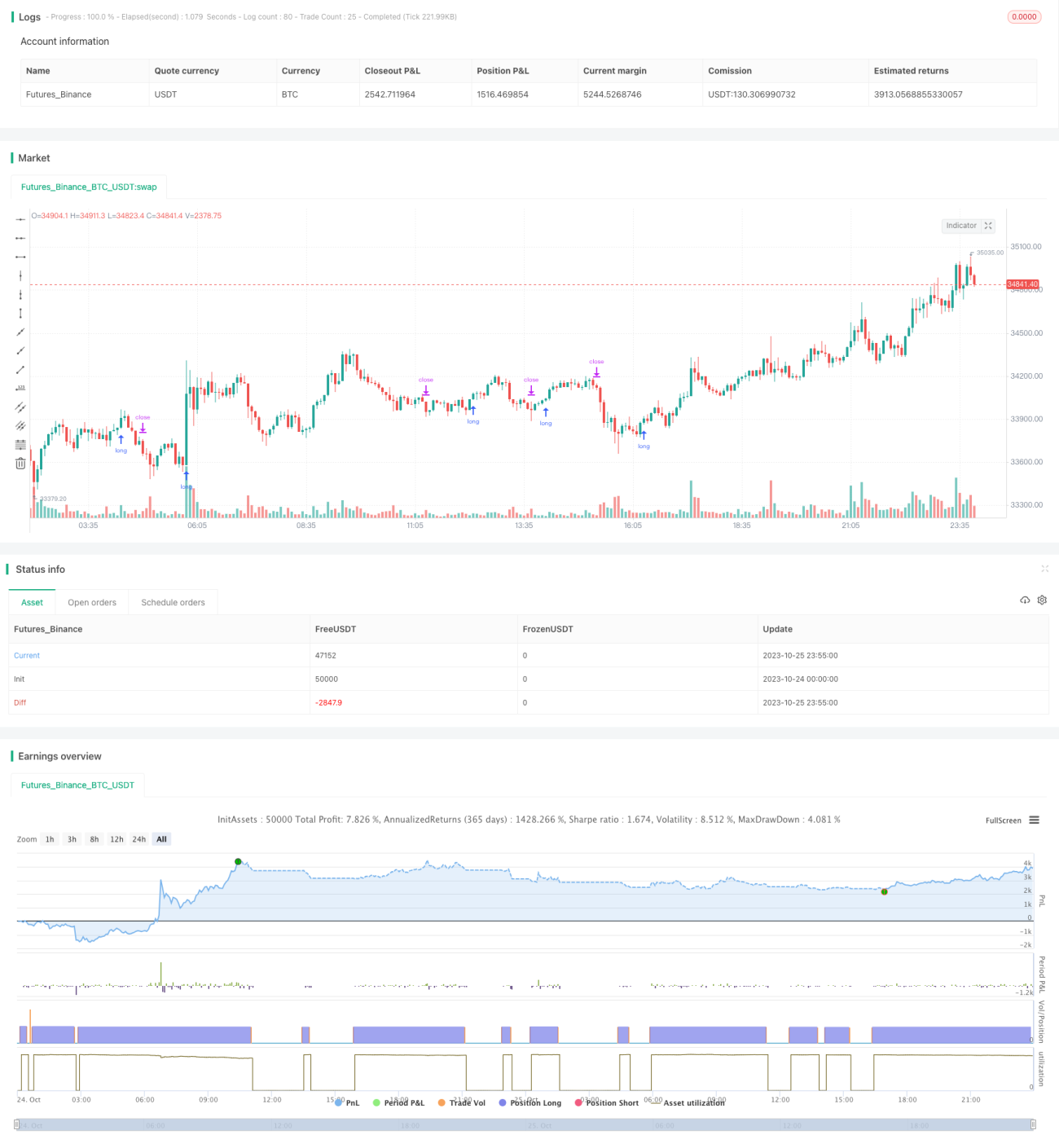

Tôi nhận thấy rằng, so với các chiến lược khác, chiến lược này nhìn chung hoạt động không tốt lắm, nhưng nó có vẻ chọn lọc giao dịch hơn. Thể hiện tỷ lệ thắng cao hơn và hệ số lợi nhuận tốt hơn. Nó chỉ thực hiện một số lượng nhỏ giao dịch và lợi nhuận ròng cũng không cao.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược này là sử dụng việc đột phá các mức hỗ trợ và kháng cự của khung thời gian cao hơn để xác định xu hướng, và giao dịch theo hướng xu hướng.

Cụ thể, nó được thực hiện qua các bước sau:

-

Tính toán các mức hỗ trợ và kháng cự của khung thời gian hiện tại (ví dụ: biểu đồ 1 giờ). Điều này được thực hiện bằng cách tìm giá cao nhất và giá thấp nhất trong một khoảng thời gian nhất định.

-

Tính toán các mức hỗ trợ và kháng cự của một hoặc nhiều khung thời gian cao hơn (ví dụ: biểu đồ 4 giờ và biểu đồ ngày). Điều này sử dụng cùng logic như khung thời gian hiện tại.

-

Vẽ các đường mức hỗ trợ và kháng cự này lên biểu đồ. Khi giá đột phá các mức này, xu hướng của khung thời gian cao hơn sẽ thay đổi.

-

Xác định hướng xu hướng dựa trên việc giá có đột phá các mức quan trọng này hay không. Nếu giá đột phá đỉnh trước đó, thì được coi là xu hướng tăng. Nếu phá vỡ đáy trước đó, thì được coi là xu hướng giảm.

-

Cho phép người dùng chọn một hoặc nhiều xu hướng của khung thời gian cao hơn làm điều kiện lọc. Nghĩa là, chỉ khi hướng xu hướng của khung thời gian hiện tại khớp với hướng xu hướng của khung thời gian cao hơn, mới xem xét giao dịch.

-

Khi thỏa mãn điều kiện lọc xu hướng và giá hiện tại đột phá mức quan trọng, thực hiện mua hoặc bán. Mức dừng lỗ được đặt ở mức hỗ trợ hoặc kháng cự quan trọng trước đó.

-

Khi giá di chuyển, khi hình thành đỉnh hoặc đáy mới, dịch chuyển mức dừng lỗ đến đáy mới để khóa lợi nhuận và theo dõi xu hướng.

-

Khi dừng lỗ bị chạm hoặc các mức hỗ trợ/kháng cự quan trọng bị phá vỡ, đóng vị thế và thoát lệnh.

Thông qua phân tích xu hướng đa khung thời gian này, chiến lược cố gắng chỉ giao dịch theo hướng xu hướng mạnh hơn, nhằm tăng xác suất thắng. Đồng thời, các mức quan trọng cung cấp tín hiệu vào lệnh và dừng lỗ rõ ràng.

Lợi thế của chiến lược

-

Sử dụng nhiều khung thời gian để xác định xu hướng, có thể nhận diện chính xác hơn các hướng xu hướng mạnh, tránh bị đánh lừa bởi nhiễu thị trường.

-

Chỉ giao dịch theo hướng xu hướng chính, có thể cải thiện đáng kể tỷ lệ thắng. Theo kết quả kiểm tra, so với bộ lọc đường trung bình động đơn giản, chiến lược này cho thấy tỷ lệ thắng cao hơn và tỷ lệ lợi nhuận trên rủi ro tốt hơn.

-

Các mức hỗ trợ và kháng cự cung cấp điểm vào lệnh và dừng lỗ rõ ràng. Không cần phải đắn đo lựa chọn điểm vào cụ thể.

-

Điều chỉnh vị trí dừng lỗ theo diễn biến xu hướng, có thể khóa lợi nhuận tối đa.

-

Logic chiến lược đơn giản và rõ ràng, dễ hiểu và tối ưu hóa.

Rủi ro của chiến lược

-

Phụ thuộc vào nhận định xu hướng dài hạn, dễ bị mắc kẹt khi xu hướng đảo chiều. Nên rút ngắn chu kỳ xác định xu hướng hoặc sử dụng các chỉ báo khác để hỗ trợ.

-

Không xem xét các yếu tố cơ bản, có thể xảy ra phân kỳ với giá khi các sự kiện quan trọng xảy ra. Có thể thêm bộ lọc như sự kiện ATM hoặc ngày công bố báo cáo tài chính.

-

Không thiết lập kiểm soát quy mô vị thế. Có thể thiết lập kích thước vị thế dựa trên quy mô tài khoản, mức độ biến động, v.v.

-

Phạm vi thời gian backtest có hạn. Nên mở rộng khoảng thời gian backtest, kiểm tra độ mạnh mẽ trong các điều kiện thị trường khác nhau.

-

Không xem xét ảnh hưởng của chi phí giao dịch. Trong giao dịch thực tế, cần điều chỉnh các tham số chiến lược dựa trên chi phí giao dịch cụ thể.

-

Chỉ xem xét giao dịch dài hạn. Có thể kết hợp với các chiến lược khác để phát triển tín hiệu giao dịch ngắn hạn, thực hiện arbitrage đa chu kỳ.

Hướng tối ưu hóa chiến lược

-

Thêm điều kiện lọc:

-

Dữ liệu cơ bản, như báo cáo tài chính, sự kiện tin tức, v.v.

-

Chỉ báo, như khối lượng, dừng lỗ ATR, v.v.

-

-

Tối ưu hóa tham số:

-

Điều chỉnh chu kỳ tính toán hỗ trợ/kháng cự

-

Điều chỉnh khung thời gian xác định xu hướng

-

-

Mở rộng phạm vi chiến lược:

-

Phát triển chiến lược giao dịch ngắn hạn

-

Xem xét cơ hội bán khống

-

Arbitrage đa sản phẩm

-

-

Cải thiện quản lý rủi ro:

-

Tối ưu hóa kích thước vị thế dựa trên biến động và quy mô tài khoản

-

Tối ưu hóa chiến lược dừng lỗ, như dừng lỗ di động, dừng lỗ chờ, v.v.

-

Giới thiệu cơ chế thưởng phạt rủi ro

-

-

Tối ưu hóa logic thực thi:

-

Cải thiện lựa chọn thời điểm vào lệnh

-

Xem xét vào lệnh một phần vị thế

-

Tối ưu hóa chiến lược di chuyển dừng lỗ

-

Tổng kết

Chiến lược này thiết kế một hệ thống đột phá tương đối mạnh mẽ thông qua phân tích xu hướng đa khung thời gian. So với các bộ lọc chỉ báo như đường trung bình động đơn giản, nó cho thấy tỷ lệ thắng cao hơn và tỷ lệ lợi nhuận trên rủi ro tốt hơn. Tuy nhiên, vẫn có một số khía cạnh có thể tối ưu hóa, chẳng hạn như cơ chế quản lý rủi ro chưa hoàn thiện, không xem xét các yếu tố cơ bản, v.v. Nếu được tối ưu hóa thêm, nó có thể trở thành một chiến lược theo dõi xu hướng rất thực tế. Nhìn chung, chiến lược này có thiết kế hợp lý, cải thiện độ chính xác của nhận định thông qua phân tích đa khung thời gian, đáng để nghiên cứu và ứng dụng thêm.

- 1