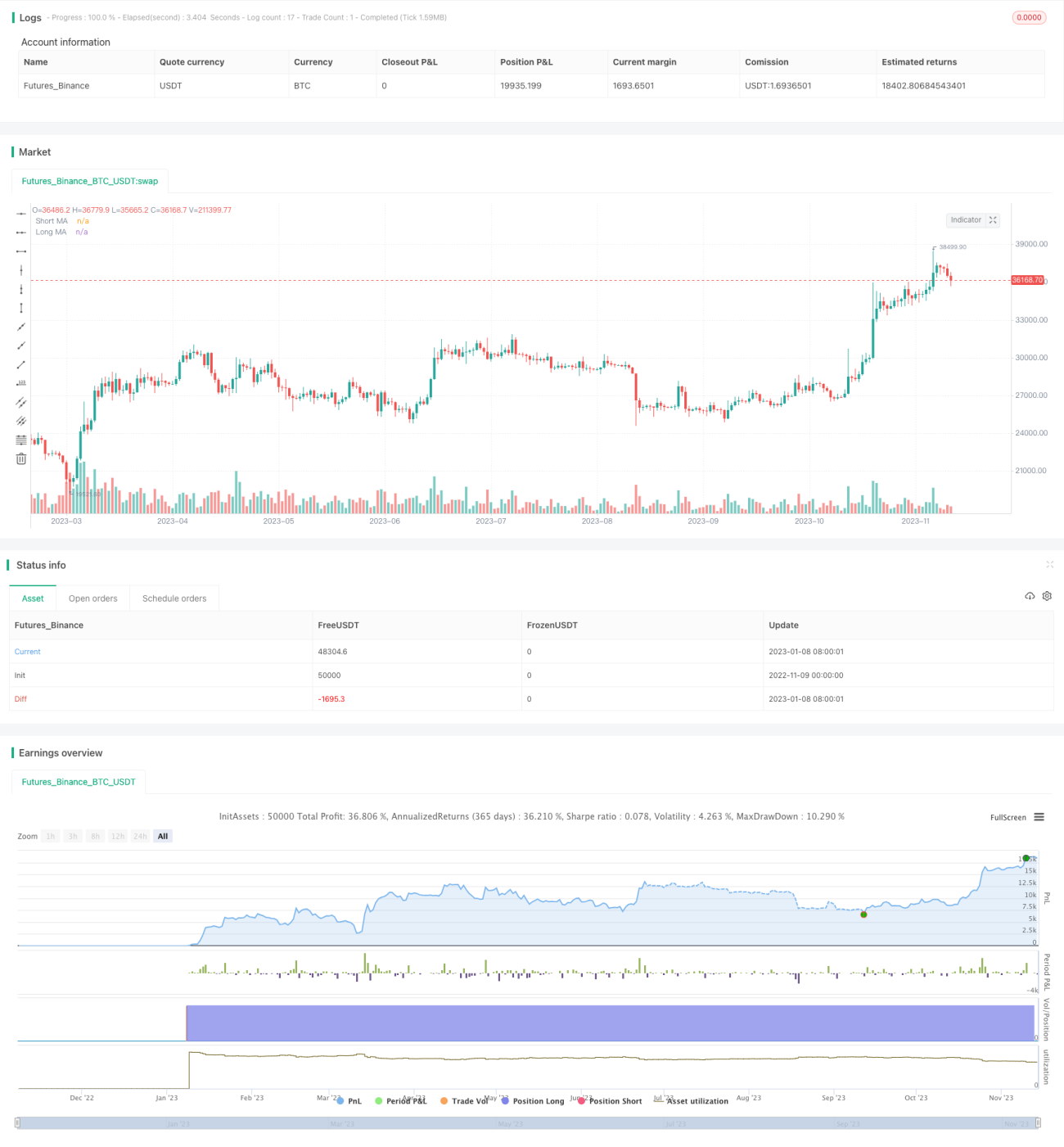

Chiến lược giao dịch định lượng DCA có trọng số phần tử tiến bộ

Tổng quan

Chiến lược giao dịch định lượng DCA trọng số lũy tiến là một chiến lược giao dịch định lượng kết hợp tín hiệu kích hoạt từ chỉ báo đường trung bình động và cơ chế trung bình giá (dollar cost averaging) trọng số lũy tiến. Chiến lược này nhằm đạt được lợi nhuận ổn định trên các thị trường có xu hướng rõ ràng thông qua việc đánh giá xu hướng và phân bổ chi phí.

Nguyên lý

Chiến lược này chủ yếu bao gồm ba phần:

-

Xác định tín hiệu vào lệnh

Sử dụng giao cắt giữa đường trung bình động nhanh và đường trung bình động chậm làm tín hiệu vào lệnh. Theo thiết lập của người dùng, có thể chọn SMA, EMA hoặc HMA làm đường nhanh và chậm. Khi đường nhanh vượt lên trên đường chậm từ phía dưới, sẽ phát ra tín hiệu mua; khi đường nhanh cắt xuống dưới đường chậm từ phía trên, sẽ phát ra tín hiệu bán.

-

DCA trọng số lũy tiến

Sau khi tín hiệu mua được kích hoạt, chiến lược sẽ ngay lập tức mở vị thế cơ sở ban đầu. Sau đó, nếu giá tiếp tục giảm, chiến lược sẽ tăng dần các vị thế an toàn tiếp theo theo cách trọng số lũy tiến. Giá của mỗi vị thế an toàn mới sẽ được điều chỉnh giảm dần một biên độ nhất định so với giá của vị thế an toàn trước đó. Đồng thời, khối lượng tiền cho các vị thế an toàn mới cũng sẽ tăng dần.

Bằng cách tăng vị thế dần dần này, có thể đạt được sự phân bổ chi phí ở một mức độ nhất định, vừa đảm bảo rủi ro giao dịch có thể kiểm soát được, vừa có được mức giá chi phí tối ưu.

-

Chốt lời và cắt lỗ

Khi giá tăng vượt qua đường chốt lời, chiến lược sẽ chọn chốt lời; khi giá giảm xuyên qua đường cắt lỗ, chiến lược sẽ chọn cắt lỗ.

Đường chốt lời cố định bằng giá trung bình khớp lệnh của vị thế cơ sở nhân với (1 + tỷ lệ cố định).

Đường cắt lỗ dao động theo giá của vị thế an toàn cuối cùng. Tín hiệu cắt lỗ được xác nhận dựa trên một tỷ lệ nhất định bên dưới giá khớp lệnh của vị thế an toàn cuối cùng.

Lợi thế

-

Kết hợp đánh giá xu hướng và phân bổ chi phí giúp chiến lược ổn định hơn

Đánh giá xu hướng có thể tránh được các thị trường dao động đi ngang không có hướng, phân bổ chi phí giúp đạt được chi phí tốt hơn trong xu hướng.

-

Tăng vị thế dần dần giúp kiểm soát rủi ro

Mỗi lần quy mô vị thế cân đối có một biên độ nhất định, đồng thời các vị thế sau có yêu cầu giảm nhất định, giúp kiểm soát rủi ro.

-

Giám sát thời gian thực vốn sử dụng của chiến lược

Mã lệnh có thêm nhãn giám sát thời gian thực, giúp người dùng biết rõ giới hạn vốn sử dụng của chiến lược, tránh sử dụng quá mức dẫn đến bị thanh lý vị thế.

-

Linh hoạt trong chốt lời và cắt lỗ từng vị thế

Vị thế cơ sở và vị thế an toàn có thể chốt lời và cắt lỗ riêng biệt, kết thúc lợi nhuận và kiểm soát rủi ro.

Rủi ro và tối ưu hóa

-

Biến động giá mạnh có thể dẫn đến tăng vị thế nhiều lần

Trong trường hợp giá biến động mạnh, có thể kích hoạt nhiều lần tăng vị thế và làm tăng thua lỗ. Có thể giảm số lần tăng vị thế bằng cách tăng yêu cầu giảm giá giữa các vị thế an toàn tiếp theo.

-

Cần tối ưu hóa lựa chọn tham số đường trung bình

Tham số đường trung bình ảnh hưởng trực tiếp đến thời điểm vào lệnh, các sản phẩm khác nhau cần kiểm tra để xác định tham số phù hợp.

-

Cần kiểm tra, tối ưu hóa tỷ lệ chốt lời và cắt lỗ

Tỷ lệ chốt lời/cắt lỗ liên quan đến tỷ suất lợi nhuận và kiểm soát sụt giảm, cần tối ưu thông qua dữ liệu backtest.

-

Có thể thiết lập điều kiện thanh lý bắt buộc dựa trên sụt giảm hoặc thời gian

Có thể kiểm tra thêm điều kiện thanh lý bắt buộc khi sụt giảm tối đa hoặc thời gian nắm giữ vượt ngưỡng để kiểm soát rủi ro thêm.

Kết luận

Chiến lược giao dịch định lượng DCA trọng số lũy tiến kết hợp ưu điểm của đánh giá xu hướng và phân bổ chi phí, có thể đạt được lợi nhuận ổn định trong các thị trường có xu hướng mạnh. Bằng cách tối ưu hóa thiết lập tham số, điều chỉnh quy mô vị thế và yêu cầu giảm giá giữa các vị thế, có thể thực hiện giao dịch ổn định với rủi ro có thể kiểm soát. Chiến lược này có thể áp dụng cho quỹ phòng hộ, quỹ CTA và thiết kế một số chiến lược đối kháng.

- 1