Chiến lược phân kỳ RSI

Tổng quan

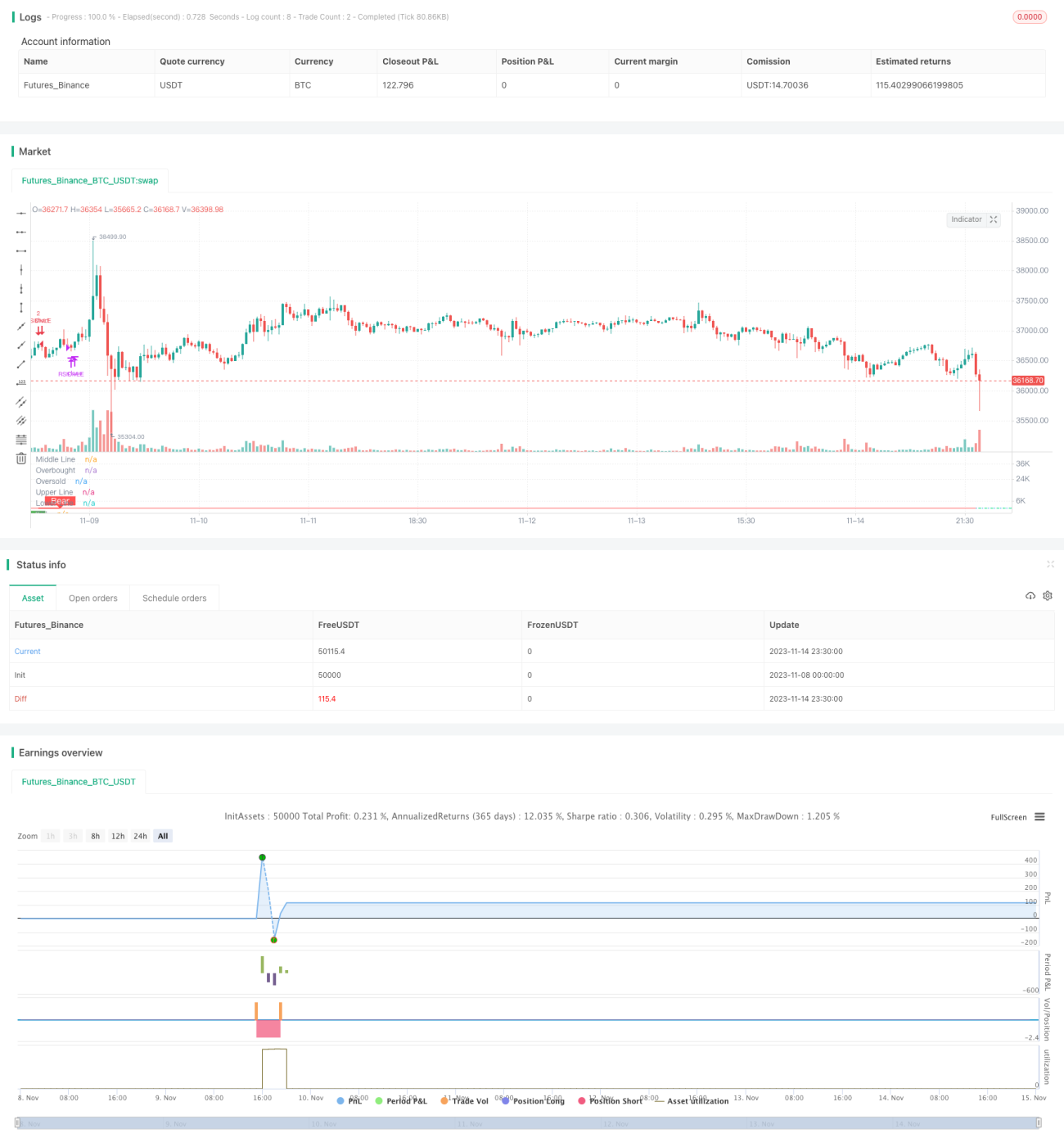

Chiến lược này xác định xu hướng tăng/giảm bằng cách tính toán chỉ báo RSI và sự giao nhau của các đường EMA của nó, kết hợp với sự phân kỳ giữa RSI và giá để tìm điểm mua/bán tiềm năng. Đây là chiến lược theo xu hướng.

Nguyên lý chiến lược

-

Tính chỉ báo RSI với độ dài 14. Khi RSI vượt lên trên mức 50 là tín hiệu tăng, vượt xuống dưới là tín hiệu giảm.

-

Tính đường EMA 20 chu kỳ và EMA 14 chu kỳ của RSI. Khi đường nhanh cắt lên trên đường chậm là tín hiệu mua, cắt xuống dưới là tín hiệu bán.

-

Phát hiện sự phân kỳ giữa RSI và giá:

-

Phân kỳ tăng: Giá tạo đáy mới thấp hơn nhưng RSI không tạo đáy mới, là tín hiệu mua.

-

Phân kỳ tăng ẩn: Giá tạo đỉnh mới cao hơn nhưng RSI không tạo đỉnh mới, là tín hiệu mua.

-

Phân kỳ giảm: Giá tạo đỉnh mới cao hơn nhưng RSI không tạo đỉnh mới, là tín hiệu bán.

-

Phân kỳ giảm ẩn: Giá tạo đáy mới thấp hơn nhưng RSI không tạo đáy mới, là tín hiệu bán.

-

-

Có thể tùy chọn bật chiến lược cắt lỗ, bao gồm cắt lỗ theo phần trăm và cắt lỗ theo ATR.

Phân tích ưu điểm

-

Ưu điểm của chỉ báo RSI là có thể phát hiện tình trạng quá mua/quá bán. Ưu điểm của đường EMA là tác dụng làm mịn, lọc bớt nhiễu.

-

Phân kỳ giữa RSI và giá có thể đưa ra tín hiệu sớm trước khi xu hướng đảo chiều.

-

Kết hợp tín hiệu của hai chỉ báo có thể xác nhận lẫn nhau, nâng cao độ ổn định của chiến lược.

-

Cơ chế cắt lỗ có thể kiểm soát mức thua lỗ trên mỗi giao dịch.

Phân tích rủi ro

-

RSI là chỉ báo dao động theo giá, khi giá biến động mạnh, hiệu quả của RSI sẽ giảm sút.

-

Đường EMA có vấn đề về độ trễ thời gian, không thể xác định chính xác điểm đảo chiều.

-

Tín hiệu phân kỳ có thể xuất hiện tín hiệu giả, giá tiếp tục di chuyển theo xu hướng ban đầu.

-

Việc đặt điểm cắt lỗ không hợp lý có thể gây ra cắt lỗ không cần thiết.

-

Mức sụt giảm có thể lớn, cần có nguồn vốn đủ mạnh.

Hướng tối ưu

-

Có thể thử nghiệm các tham số khác nhau cho RSI và EMA để tìm ra bộ tham số tối ưu.

-

Có thể cân nhắc thay thế đường EMA bằng các chỉ báo khác như MACD để tối ưu tổ hợp.

-

Có thể thiết lập cơ chế xác nhận để tránh phân kỳ giả. Ví dụ yêu cầu nhiều tín hiệu phân kỳ liên tiếp mới kích hoạt.

-

Thêm chiến lược chốt lời để khóa lợi nhuận.

-

Có thể dựa trên các tín hiệu ngắn hạn như mô hình nến để vào lệnh, kết hợp với nhận định xu hướng của chiến lược này.

Tổng kết

Chiến lược này kết hợp nhận định quá mua/quá bán của RSI, nhận định xu hướng của EMA và dự báo phân kỳ, tạo thành một hệ thống theo xu hướng tương đối hoàn chỉnh. Sau khi điều chỉnh tham số và tối ưu tổ hợp, có thể đạt được hiệu quả chiến lược tốt. Tuy nhiên vẫn cần chú ý phòng ngừa tác động của thị trường xu hướng và nhiễu từ tín hiệu giả. Thông qua quản lý vốn chặt chẽ, chiến lược này có thể mang lại lợi nhuận vượt trội ổn định trong trung và dài hạn.

/*backtest

start: 2023-11-08 00:00:00

end: 2023-11-15 00:00:00

period: 30m

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="RSI Divergence Indicator", overlay=false,pyramiding=2, default_qty_value=2, default_qty_type=strategy.fixed, initial_capital=10000, currency=currency.USD)

len = input(title="RSI Period", minval=1, defval=14)- 1