Chiến lược giao dịch đường trung bình động hình tam giác ngược Siêu Nga

Tổng quan

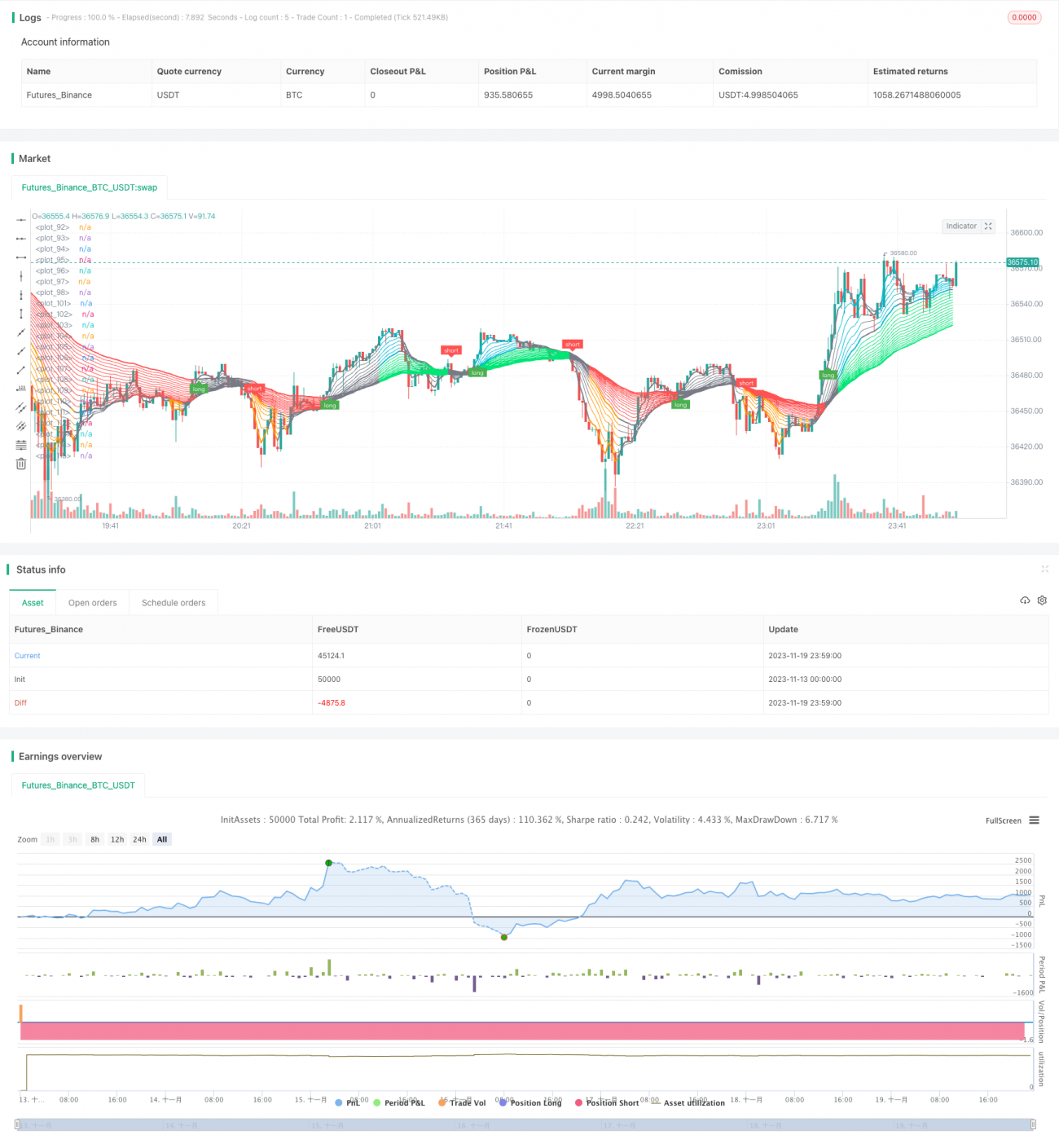

Ý tưởng chính của chiến lược này là sử dụng nhiều đường trung bình động với các chu kỳ khác nhau để xây dựng tín hiệu giao dịch "Super Goose" (Ngỗng Siêu Cấp), nhằm phát hiện các xu hướng mang tính định hướng trong khoảng thời gian tương đối dài. Super Goose được cấu tạo từ hai nhóm đường trung bình động nhanh và chậm, đường nhanh quyết định điểm vào lệnh cụ thể, đường chậm quyết định hướng giao dịch tổng thể. Khi đường nhanh cắt lên trên đường chậm, tín hiệu long được tạo ra; khi cắt xuống dưới, tín hiệu short được tạo ra.

Nguyên lý

Chiến lược này sử dụng nhiều nhóm đường EMA với các chu kỳ khác nhau, cụ thể:

- Đường nhanh: 3 chu kỳ, 6 chu kỳ... 21 chu kỳ (7 đường)

- Đường chậm: 24 chu kỳ, 27 chu kỳ... 200 chu kỳ

Khi các đường nhanh giao nhau, chúng được chia thành màu xanh lam (tăng) và màu cam (giảm); khi các đường chậm giao nhau, chúng được chia thành màu xanh lục (tăng) và màu đỏ (giảm). Khi đường nhanh màu xanh lam chuyển từ màu xám sang màu xanh lục (đường chậm), tín hiệu long được tạo ra; ngược lại, khi chuyển từ màu xanh lục sang màu xám, vị thế long được đóng; khi chuyển từ màu xám sang màu đỏ, tín hiệu short được tạo ra.

Chiến lược này đồng thời cung cấp hai chế độ: Chế độ ổn định chỉ giao dịch sau khi EMA nhanh và chậm xác nhận hướng; chế độ mạo hiểm, bất kỳ sự thay đổi hướng nào của EMA nhanh cũng tạo ra tín hiệu.

Lợi thế

Chiến lược này kết hợp ưu điểm của hệ thống hai đường trung bình động, vừa có thể kịp thời nắm bắt cơ hội giao dịch trong chu kỳ ngắn hạn, vừa có thể sử dụng đường chậm để lọc bỏ các tín hiệu nhiễu quá mức. Cụ thể:

- Sự kết hợp giữa EMA nhanh và chậm giúp kiểm soát rủi ro hiệu quả.

- Chế độ mạo hiểm có thể kịp thời nắm bắt cơ hội ngắn hạn.

- Chế độ ổn định mang lại cơ hội có xác suất cao và tỷ lệ lợi nhuận/rủi ro cao.

- Không gian tối ưu hóa tham số thủ công rộng lớn.

Rủi ro

Chiến lược này cũng tồn tại một số rủi ro:

- Trong thị trường biến động mạnh, có thể xuất hiện nhiều thời gian tiếp xúc với thị trường.

- Hệ thống nhiều đường trung bình động khiến việc tối ưu hóa và kiểm tra tham số trở nên khó khăn hơn.

- Trong chế độ ổn định, một phần lợi nhuận có thể bị mất do độ trễ của đường EMA nhanh.

Có thể kiểm soát rủi ro bằng cách điều chỉnh phù hợp bộ tham số EMA nhanh/chậm hoặc thiết lập stop loss.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

- Thêm stop loss dựa trên độ biến động. Điều này có thể kiểm soát hiệu quả tổn thất sau các biến động lớn riêng lẻ.

- Thử nghiệm thuật toán học máy để tối ưu hóa tham số EMA. Điều này có thể nâng cao đáng kể hiệu suất sử dụng tham số.

- Thêm bộ lọc kết hợp khối lượng và giá. Điều này có thể gia tăng các cơ hội giao dịch thực chất.

- Khám phá kết hợp các chỉ báo khác với giao cắt EMA. Làm như vậy có thể nâng cao thêm độ chính xác giao dịch.

Tổng kết

Chiến lược Super Goose này cân nhắc tổng hợp các yếu tố đa khung thời gian, vừa kiểm soát rủi ro vừa gia tăng cơ hội sinh lời. Nó có thể được tối ưu hóa và nâng cấp thông qua nhiều cách, xứng đáng để các nhà giao dịch định lượng nghiên cứu sâu.

/*backtest

start: 2023-11-13 00:00:00

end: 2023-11-20 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// A strategized version Daryl Guppy Super EMA's with additional options

// by default "early signals" is enabled, which will trade any green/gray or red/gray transitions of the guppy. Disable to only take longs while green, and shorts while red.

//@version=4- 1