Chiến lược theo dõi xu hướng với chỉ báo Williams và EMA kép

Tổng quan

Chiến lược này kết hợp chỉ báo hai đường EMA và chỉ báo Williams để xác định hướng xu hướng, theo dõi khi xu hướng đủ mạnh. Ý tưởng cơ bản là:

- Sử dụng bộ đôi EMA để lọc ra những xu hướng mạnh nhất

- Chỉ báo Williams xác nhận khu vực quá mua/quá bán hiện tại

- Kết hợp chỉ báo RSI để tránh mua đuổi bán đáy

Nguyên lý

Chiến lược này sử dụng EMA ngắn hạn và EMA dài hạn trong bộ đôi EMA. Khi EMA ngắn hạn cắt lên trên EMA dài hạn phát sinh tín hiệu mua, EMA ngắn hạn cắt xuống dưới EMA dài hạn phát sinh tín hiệu bán, tận dụng hai đường EMA để bắt xu hướng trung dài hạn.

Ngoài ra, chiến lược còn kết hợp chỉ báo Williams để xác định tình huống đảo chiều. Chỉ báo Williams xác định xem giá có đang ở trạng thái quá mua hay quá bán thông qua việc xét đỉnh và đáy trong chu kỳ. Khi chỉ báo Williams hiển thị quá mua, phát sinh tín hiệu bán; khi hiển thị quá bán, phát sinh tín hiệu mua.

Trong code, logic cụ thể như sau:

Vào lệnh Long: EMA ngắn hạn cắt lên trên EMA trung hạn và EMA dài hạn, đồng thời chỉ báo Williams hiển thị vùng quá bán và hình thành đáy thấp nhất trong vùng quá bán, cho thấy cơ hội đảo chiều, lúc này phát sinh tín hiệu mua.

Vào lệnh Short: EMA ngắn hạn cắt xuống dưới EMA trung hạn và EMA dài hạn, đồng thời chỉ báo Williams hiển thị vùng quá mua và hình thành đỉnh cao nhất trong vùng quá mua, cho thấy cơ hội đảo chiều, lúc này phát sinh tín hiệu bán.

Ngoài ra, chiến lược còn đưa vào chỉ báo RSI để xác nhận thêm tín hiệu giao dịch, tránh mua đuổi bán đáy một cách mù quáng.

Ưu điểm

Ưu điểm lớn nhất của chiến lược này là sử dụng hai đường EMA để lọc bỏ phần lớn các xu hướng không hiệu quả, chỉ chọn những xu hướng trung dài hạn mạnh nhất để theo dõi, từ đó lọc nhiễu, giảm giao dịch không hiệu quả.

Ngoài ra, việc đưa vào chỉ báo Williams cũng có tác dụng rất tốt. Một là có thể xác định cơ hội đảo chiều, từ đó đóng vị thế kịp thời; hai là có thể xác nhận thêm độ tin cậy của tín hiệu xu hướng.

Sự kết hợp giữa hai đường EMA và Williams giúp chiến lược này đạt được lợi nhuận theo dõi tốt trong các sản phẩm trung dài hạn, đồng thời cũng có thể xác định đảo chiều và hạn chế thua lỗ.

Rủi ro

Rủi ro chính của chiến lược này là khó xác định điểm đảo chiều xu hướng. Mặc dù đã đưa vào chỉ báo Williams và RSI để đảm bảo hiệu quả giao dịch đảo chiều, nhưng độ khó của giao dịch đảo chiều vẫn cao, không thể hoàn toàn tránh được rủi ro mua đuổi bán đáy.

Ngoài ra, bản thân bộ đôi EMA cũng có độ trễ nhất định. Khi xu hướng ngắn hạn và trung dài hạn không đồng nhất, có thể gây khó khăn cho chiến lược trong việc nhận diện.

Tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

-

Thử nghiệm thêm nhiều tổ hợp chu kỳ EMA để tìm thông số tốt hơn

-

Thêm cơ chế thoát lệnh thích ứng, sử dụng các chỉ báo như ATR, chỉ số biến động để xác định đảo chiều xu hướng

-

Thêm yếu tố học máy, sử dụng LSTM để dự đoán xu hướng và đảo chiều

-

Sử dụng lý thuyết sóng và các phương pháp khác để hoàn thiện quy tắc giao dịch đảo chiều

-

Đưa vào quản lý vị thế thích ứng, điều chỉnh quy mô vị thế dựa trên điều kiện thị trường

Kết luận

Chiến lược này đã kết hợp thành công hai đường EMA và chỉ báo Williams để bắt xu hướng trung dài hạn, thu được lợi nhuận cao hơn trong xu hướng lớn. Đồng thời, việc đưa vào chỉ báo Williams giúp chiến lược có thể xác định tình huống đảo chiều và cắt lỗ kịp thời. Bước tiếp theo, thông qua việc đưa thêm nhiều chỉ báo và mô hình để tối ưu hóa, tăng cường hơn nữa độ ổn định của chiến lược.

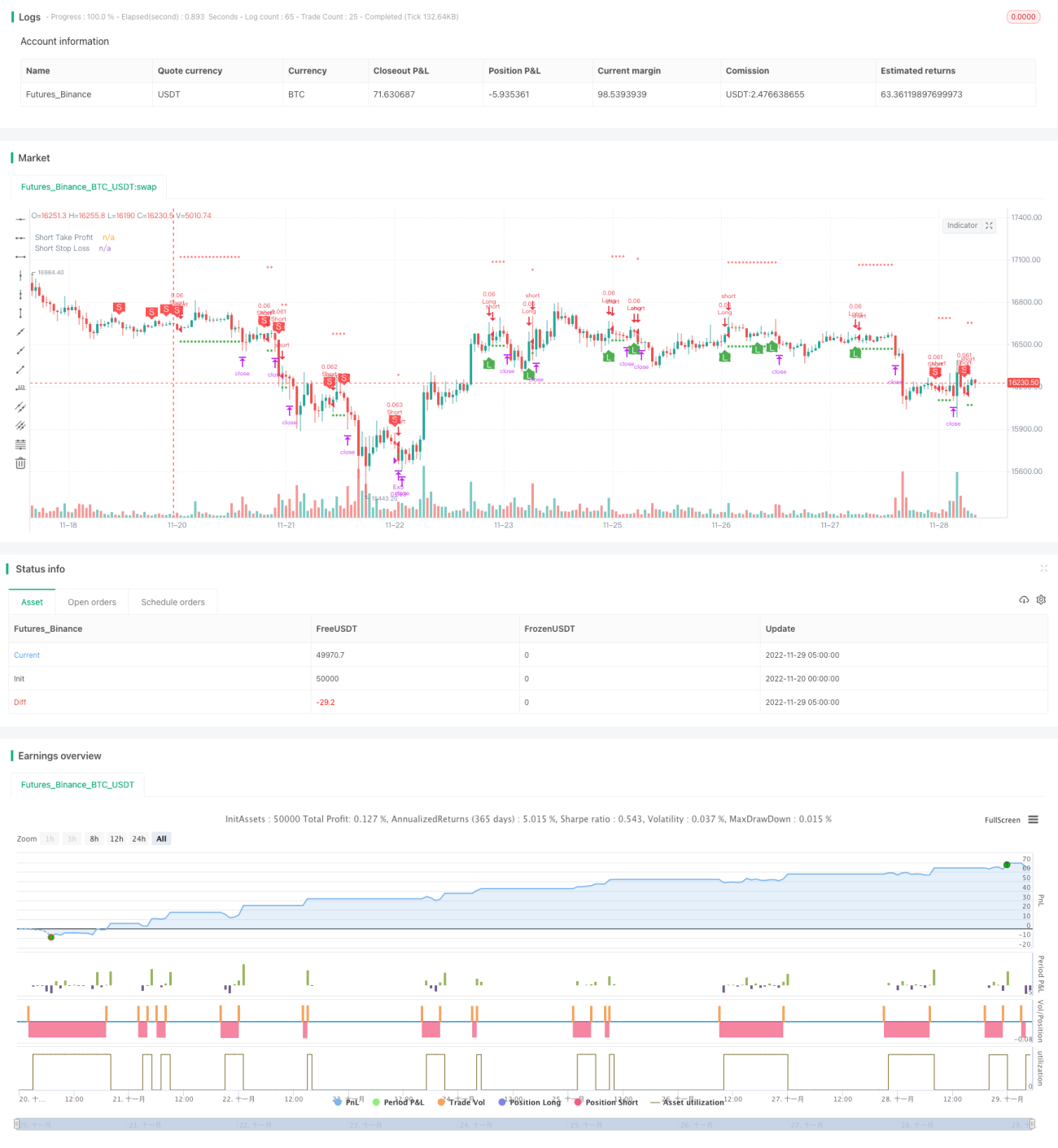

/*backtest

start: 2022-11-20 00:00:00

end: 2022-11-29 05:20:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © B_L_A_C_K_S_C_O_R_P_I_O_N

// v 1.1

- 1