Chiến lược phá vỡ độ lệch chuẩn của Dải Bollinger

1

Follow

1802

Followers

Tổng quan

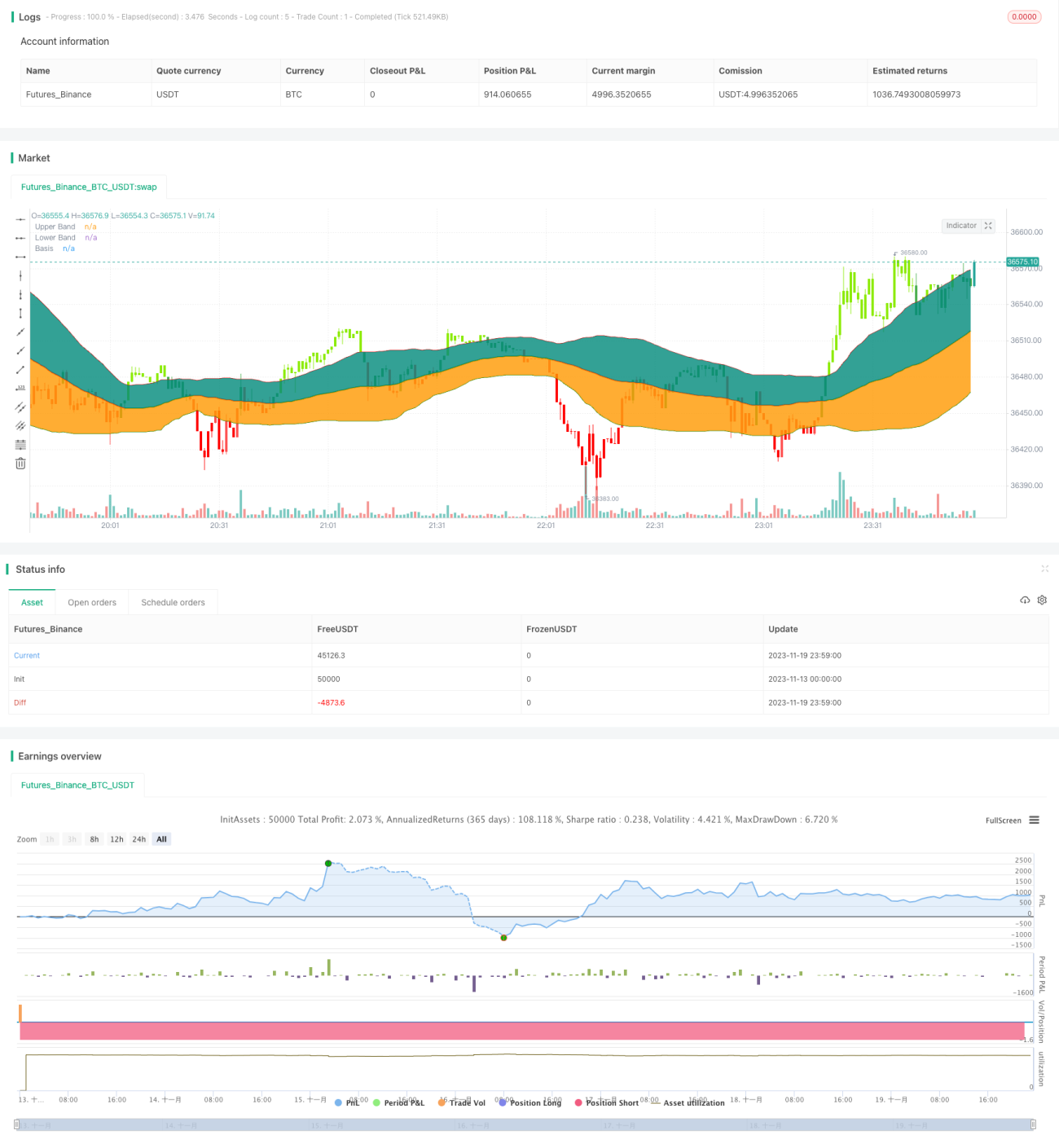

Chiến lược này dựa trên chỉ báo Bollinger Bands cổ điển, khi giá đóng cửa vượt lên band trên thì mua, khi giá đóng cửa phá vỡ band dưới thì bán khống, thuộc chiến lược breakout theo xu hướng.

Nguyên lý chiến lược

- Đường cơ sở là đường trung bình động đơn giản 55 kỳ.

- Band trên và band dưới lần lượt là đường cơ sở cộng/trừ một độ lệch chuẩn.

- Khi giá đóng cửa vượt lên band trên, phát tín hiệu mua.

- Khi giá đóng cửa phá vỡ band dưới, phát tín hiệu bán khống.

- Sử dụng một độ lệch chuẩn thay vì hai độ lệch chuẩn cổ điển giúp giảm rủi ro.

Phân tích ưu điểm

- Sử dụng độ lệch chuẩn thay vì giá trị cố định giúp giảm rủi ro.

- Đường trung bình động 55 kỳ phản ánh tốt xu hướng trung hạn.

- Đóng cửa vượt ngưỡng giúp lọc nhiễu giả.

- Dễ dàng phân tích đa khung thời gian để xác định hướng xu hướng.

Phân tích rủi ro

- Dễ tạo ra lợi nhuận nhỏ trong dao động.

- Cần xem xét ảnh hưởng của phí giao dịch.

- Tín hiệu breakout có thể là giả.

- Có thể xảy ra trượt giá thua lỗ.

Có thể giảm rủi ro bằng cách đặt stop loss, cân nhắc phí giao dịch, hoặc thêm bộ lọc chỉ báo.

Hướng tối ưu hóa

- Tối ưu tham số đường cơ sở để tìm đường trung bình tốt nhất.

- Tối ưu độ lớn độ lệch chuẩn để tìm thông số tốt nhất.

- Thêm các chỉ báo khối lượng, giá để hỗ trợ ra quyết định.

- Thêm cơ chế stop loss.

Tổng kết

Chiến lược này có logic tổng thể rõ ràng, điều chỉnh rủi ro thông qua độ rộng của dải độ lệch chuẩn, phá vỡ khi đóng cửa tránh tín hiệu giả. Tuy nhiên, vẫn cần chú ý tránh thua lỗ trong dao động, có thể tối ưu bằng cách đặt stop loss, thêm bộ lọc, v.v.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1