Chiến lược phá vỡ dao động SuperTrend đa khung thời gian

Tổng quan

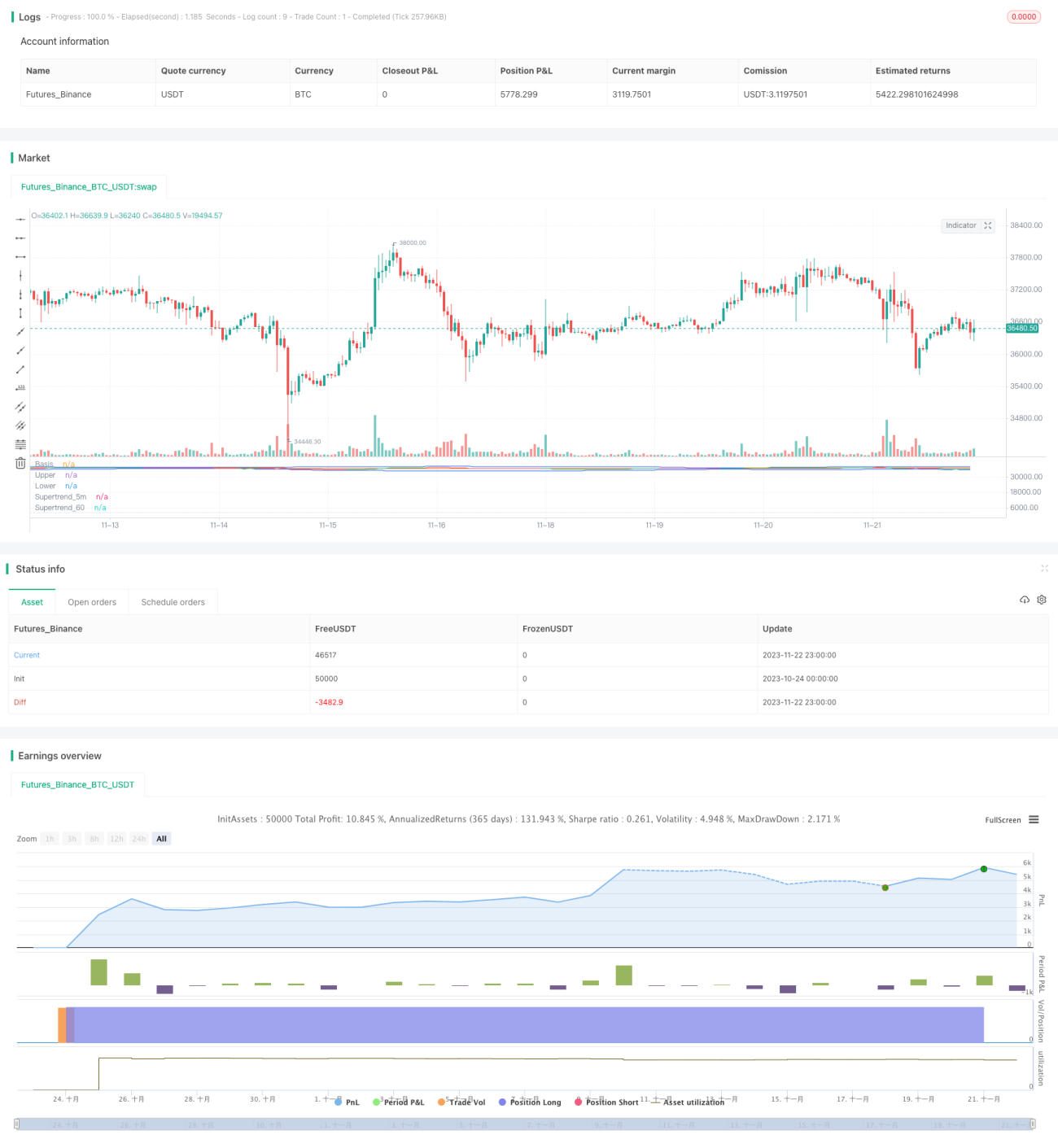

Chiến lược này kết hợp chỉ báo SuperTrend đa khung thời gian với dải Bollinger, xác định hướng xu hướng và các mức hỗ trợ/kháng cự chính, thực hiện vào lệnh khi có sự bứt phá trong vùng dao động và thoát lệnh dựa trên giao cắt. Chiến lược này chủ yếu phù hợp với các hợp đồng hàng hóa tương lai có biến động cao như vàng, bạc, dầu thô, v.v.

Nguyên lý chiến lược

Dựa trên hàm SuperTrend đa khung thời gian tùy chỉnh được viết bằng Pine Script pine_supertrend(), kết hợp SuperTrend ở các khung thời gian khác nhau (ví dụ: 1 phút và 5 phút) để xác định hướng xu hướng của khung thời gian lớn.

Đồng thời, tính toán dải trên và dải dưới của Bollinger để xác định sự bứt phá kênh. Khi giá phá vỡ dải trên Bollinger, được coi là bứt phá tăng giá; khi giá phá vỡ dải dưới Bollinger, được coi là bứt phá giảm giá.

Tín hiệu chiến lược:

Tín hiệu Long: Giá đóng cửa > Dải trên Bollinger và Giá đóng cửa > Chỉ báo SuperTrend đa khung thời gian

Tín hiệu Short: Giá đóng cửa < Dải dưới Bollinger và Giá đóng cửa < Chỉ báo SuperTrend đa khung thời gian

Cắt lỗ:

Cắt lỗ Long: Giá đóng cửa < Chỉ báo SuperTrend khung 5 phút

Cắt lỗ Short: Giá đóng cửa > Chỉ báo SuperTrend khung 5 phút

Do đó, chiến lược này nắm bắt sự bứt phá cộng hưởng giữa chỉ báo SuperTrend và dải Bollinger, thực hiện giao dịch trong các đợt biến động mạnh.

Phân tích ưu điểm

- Sử dụng chỉ báo SuperTrend đa khung thời gian để xác định hướng xu hướng khung thời gian lớn, nâng cao chất lượng tín hiệu.

- Dải trên và dải dưới Bollinger đóng vai trò là các mức hỗ trợ/kháng cự quan trọng, giúp giảm các phá vỡ giả.

- Sử dụng chỉ báo SuperTrend làm mức cắt lỗ, giảm thua lỗ và kiểm soát rủi ro.

Phân tích rủi ro

- Chỉ báo SuperTrend có độ trễ, có thể bỏ lỡ điểm đảo chiều xu hướng.

- Cài đặt tham số Bollinger không phù hợp có thể dẫn đến giao dịch quá thường xuyên hoặc bỏ sót quá nhiều.

- Trong phiên giao dịch đêm hoặc khi có sự kiện lớn, giá biến động mạnh dễ dẫn đến cắt lỗ.

Giải pháp rủi ro:

- Kết hợp nhiều chỉ báo phụ trợ để xác nhận tín hiệu, tránh phá vỡ giả.

- Tối ưu hóa tham số Bollinger để tìm điểm cân bằng tốt nhất.

- Điều chỉnh vị trí cắt lỗ, mở rộng khoảng cách cắt lỗ.

Hướng tối ưu hóa

- Thử nghiệm các chỉ báo xu hướng khác như KDJ, MACD làm hỗ trợ.

- Thêm mô hình học máy để đánh giá xác suất làm trợ lực.

- Thực hiện tối ưu hóa tham số để tìm bộ siêu tham số tốt nhất.

Tổng kết

Chiến lược này tích hợp hai chỉ báo hiệu quả là SuperTrend và Bollinger, thông qua phân tích đa khung thời gian và xác định bứt phá kênh để đạt được giao dịch xác suất cao. Chiến lược kiểm soát rủi ro vốn hiệu quả, chứng minh có thể thu được lợi nhuận tốt trong các sản phẩm biến động mạnh. Bằng cách tối ưu hóa thêm và kết hợp các chỉ báo khác, hiệu quả của chiến lược vẫn có thể được cải thiện.

- 1