Chiến lược bám xu hướng đa chỉ báo

Tổng quan

Chiến lược này kết hợp 3 chỉ báo mã nguồn mở để đánh giá xu hướng đa khung thời gian, đồng thời thiết lập cắt lỗ và chốt lời nhằm khóa lợi nhuận. Cụ thể, chiến lược sử dụng chỉ báo AK MACD BB để xác định hướng xu hướng ngắn hạn, chỉ báo SSL để lọc bỏ một phần tín hiệu giả, và cuối cùng kết hợp với chỉ báo khối lượng VSF để đánh giá sức mạnh thực sự của bên mua/bán, từ đó xác định thời điểm vào lệnh. Đồng thời, chiến lược thiết lập sẵn các mức cắt lỗ và chốt lời để khóa lợi nhuận, giúp giảm đáng kể rủi ro thua lỗ cho từng giao dịch.

Nguyên lý chiến lược

-

Chỉ báo AK MACD BB

Chỉ báo này áp dụng Bollinger Bands lên chỉ báo MACD. Khi đường MACD phá vỡ dải trên của Bollinger Bands, tín hiệu mua được tạo ra; khi phá vỡ dải dưới, tín hiệu bán được tạo ra.

-

Chỉ báo SSL

Chỉ báo SSL xác định xem giá có phá vỡ đường trung bình động hay không và phát hiện tín hiệu kiểm tra lại (retest). Khi giá cắt lên trên đường trung bình động và chỉ báo SSL có màu xanh lam, đó là xu hướng tăng; khi giá cắt xuống dưới đường trung bình động và chỉ báo SSL có màu đỏ, đó là xu hướng giả, và tín hiệu giao dịch được phát ra.

-

Chỉ báo VSF

Chỉ báo VSF đánh giá sức mạnh của bên mua và bên bán. Chiến lược chỉ phát tín hiệu khi sức mạnh của bên mua hoặc bên bán lớn hơn 50%, tránh các phá vỡ không hiệu quả.

-

Cắt lỗ và chốt lời

Chiến lược có 4 mức chốt lời tiến bộ (progressive take profit), với khoảng cách lợi nhuận từ 1.5 đến 3 lần. Đồng thời, thiết lập cắt lỗ cố định 2%, kiểm soát hiệu quả mức thua lỗ tối đa cho mỗi giao dịch.

Phân tích ưu điểm

-

Kết hợp đa chỉ báo, độ chính xác cao

Bằng cách sử dụng các chỉ báo khác nhau để đánh giá xu hướng đa khung thời gian, có thể lọc bỏ tín hiệu giả và đưa ra phán đoán chính xác hơn.

-

Tự động chốt lời và cắt lỗ, rủi ro được kiểm soát

Chiến lược tích hợp sẵn các thiết lập chốt lời và cắt lỗ, giúp giới hạn thua lỗ mỗi giao dịch ở mức khoảng 2%, tránh thua lỗ lớn.

-

Dữ liệu backtest xuất sắc

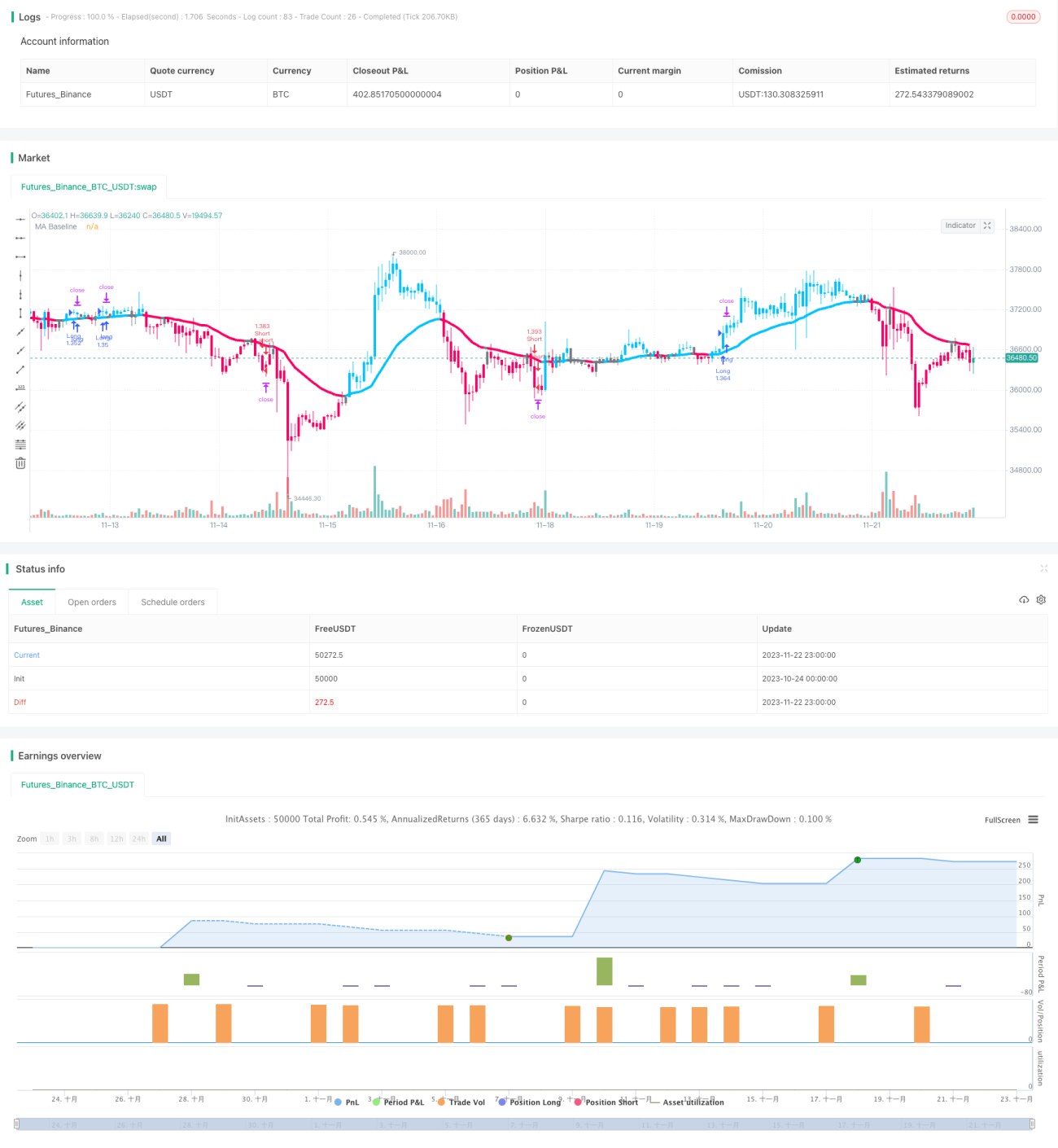

Theo backtest của nhà phát hành, trong 100 giao dịch, tỷ lệ giao dịch có lợi nhuận đạt 74%, tổng lợi nhuận 427%.

Phân tích rủi ro và biện pháp đối phó

-

Rủi ro biến động thị trường mạnh

Khi thị trường dao động trong biên độ lớn, có thể xảy ra nhiều lần thua lỗ nhỏ. Lúc này có thể điều chỉnh mức cắt lỗ cố định hoặc tạm dừng giao dịch.

-

Rủi ro hạn chế mua hoặc bán

Hiện tại chiến lược có thể mua và bán. Nếu chỉ giới hạn mua hoặc chỉ bán, cơ hội kiếm lợi nhuận sẽ giảm đi một nửa.

-

Rủi ro thời gian giao dịch

Chiến lược sử dụng dữ liệu 5 phút để đánh giá. Nếu chỉ có vài giờ dữ liệu trong một ngày giao dịch, số lượng mẫu không đủ, tín hiệu có thể không đáng tin cậy.

Hướng tối ưu hóa chiến lược

-

Tối ưu hóa tham số cắt lỗ và chốt lời

Có thể kiểm tra các mức cắt lỗ và chốt lời khác nhau để tìm ra tham số tối ưu. Cắt lỗ quá nhỏ không kiểm soát được rủi ro hiệu quả, cắt lỗ quá lớn có thể bỏ lỡ lợi nhuận lớn hơn.

-

Thêm tính năng điều chỉnh vị thế tự động

Có thể thiết lập trailing stop hoặc moving stop để khóa lợi nhuận. Hoặc tăng vị thế dựa trên các điều kiện cụ thể để thu được nhiều lợi nhuận hơn.

-

Kết hợp với các chỉ báo khác

Có thể kiểm tra sự kết hợp của các chỉ báo khác nhau để xem tổ hợp nào hiệu quả nhất. Cũng có thể thêm nhiều chỉ báo hơn để xác nhận chéo.

-

Tối ưu hóa tham số

Có thể backtest với các tham số khác nhau để tìm hướng tối ưu hóa tham số. Trong chiến lược này, việc thay đổi tham số Bollinger Bands hoặc tham số đường trung bình động có thể mang lại kết quả tốt hơn.

Tổng kết

Chiến lược này tích hợp nhiều chỉ báo để xác định hướng xu hướng, thiết lập tự động chốt lời và cắt lỗ, có thể thu lợi nhuận trong xu hướng mạnh và kiểm soát thua lỗ mỗi giao dịch ở mức rất nhỏ. Từ dữ liệu backtest của nhà phát hành, tỷ lệ chiến thắng và lợi nhuận đều rất lý tưởng. Thông qua một số tối ưu hóa nhất định, có thể nâng cao hơn nữa tính ổn định và khả năng sinh lời của chiến lược.

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © myn

//@version=5

strategy('Strategy Myth-Busting #7 - MACDBB+SSL+VSF - [MYN]', max_bars_back=5000, overlay=true, pyramiding=0, initial_capital=1000, currency='USD', default_qty_type=strategy.percent_of_equity, default_qty_value=1.0, commission_value=0.075, use_bar_magnifier = false)

/////////////////////////////////////

//* Put your strategy logic below *//

/////////////////////////////////////

//nwVqTuPe6yo- 1