Chiến lược giao dịch độ lệch chuẩn trọng số đường trung bình

Tổng quan

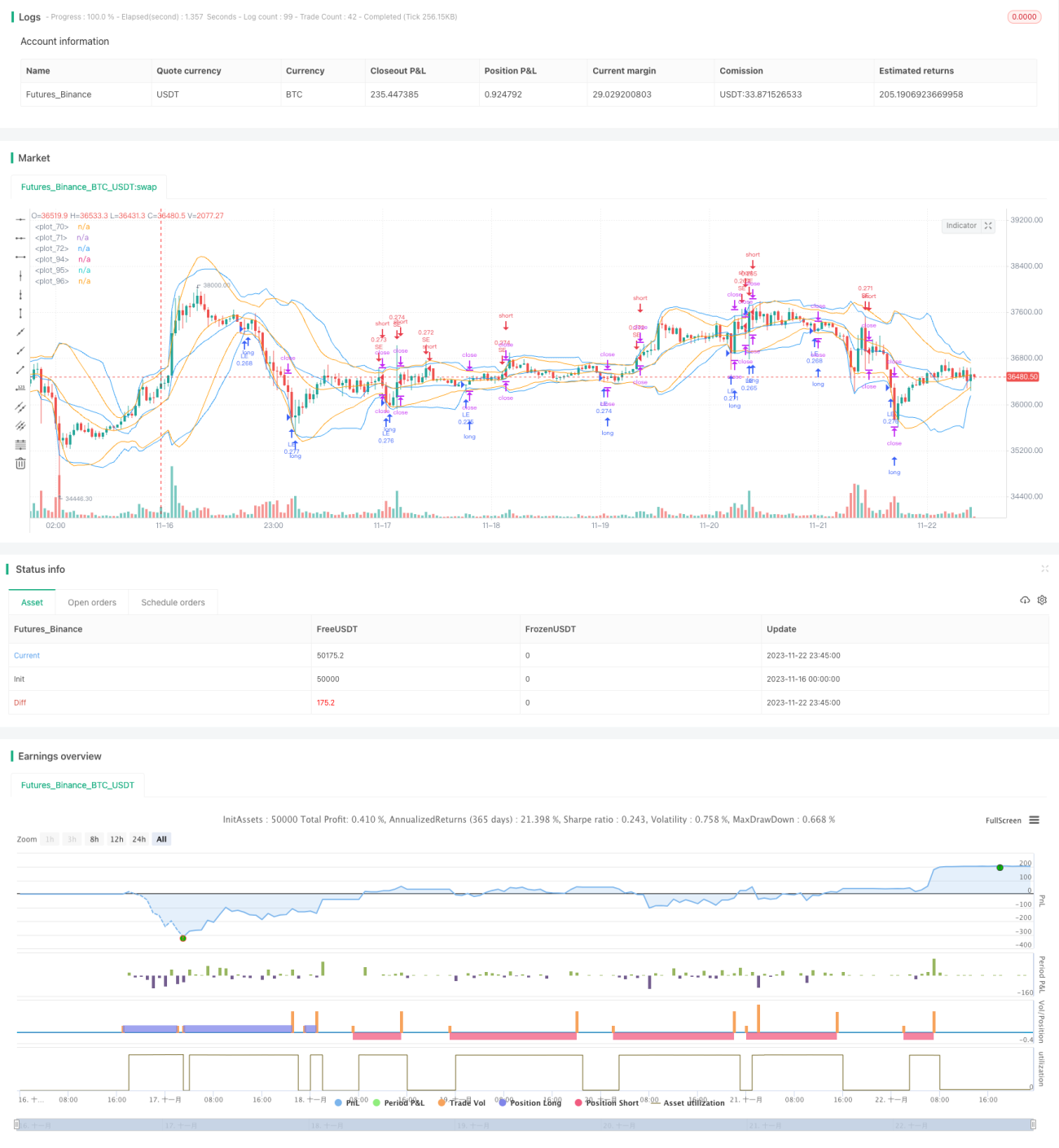

Chiến lược này sử dụng chỉ báo độ lệch chuẩn có trọng số, kết hợp với đường trung bình động, để thực hiện giao dịch theo xu hướng đối với tiền điện tử. Chiến lược tính toán kênh độ lệch chuẩn có trọng số của giá dựa trên giá đóng cửa và khối lượng trong một khoảng thời gian nhất định. Khi giá phá vỡ biên trên hoặc biên dưới của kênh, sẽ thực hiện mua vào hoặc bán ra. Đồng thời, thiết lập các điều kiện cắt lỗ và chốt lời để giảm thiểu tổn thất cho mỗi lệnh.

Nguyên lý chiến lược

Trong mã nguồn định nghĩa hai hàm tùy chỉnh, tính toán độ lệch chuẩn có trọng số từ chuỗi thời gian và mảng. Các bước chính bao gồm:

- Tính giá trung bình có trọng số dựa trên giá đóng cửa và khối lượng

- Tính bình phương sai số của mỗi nến so với giá trung bình

- Tính phương sai theo số lượng mẫu và trọng số đã điều chỉnh

- Lấy căn bậc hai để có độ lệch chuẩn

Nhờ đó, chúng ta có được một kênh có tâm là giá trung bình có trọng số, khoảng cách trên và dưới là một độ lệch chuẩn. Khi giá phá vỡ từ dưới lên qua đáy kênh, sẽ mua vào; khi phá vỡ từ trên xuống qua đỉnh kênh, sẽ bán ra.

Phân tích ưu điểm

Ưu điểm lớn nhất của chiến lược này là kết hợp phân tích đường trung bình động và độ biến động. Đường trung bình động xác định hướng xu hướng thị trường, độ lệch chuẩn xác định vùng giá hợp lý, cả hai bổ trợ lẫn nhau, độ tin cậy cao. Ngoài ra, trọng số khối lượng có thể lọc các phá vỡ giả, xác suất phá vỡ thực tế cao hơn.

Chiến lược này cũng thiết lập điểm cắt lỗ và chốt lời, giúp nắm bắt xu hướng và tránh tổn thất lớn khi đảo chiều. Đây là điểm mà nhiều người mới không thể nắm vững.

Phân tích rủi ro

Rủi ro chính là thị trường có thể biến động mạnh. Khi đó, kênh độ lệch chuẩn cũng biến động lớn, gây khó khăn cho việc phán đoán. Ngoài ra, nếu chọn chu kỳ quá ngắn, dễ bị nhiễu loạn, tỷ lệ lỗi cao.

Giải pháp là có thể điều chỉnh tham số chu kỳ phù hợp, làm mượt đường cong. Cũng có thể kết hợp các chỉ báo khác như RSI để tăng xác nhận phá vỡ.

Hướng tối ưu hóa

- Tối ưu tham số chu kỳ. Có thể thử nghiệm các chu kỳ 5 phút, 15 phút, 30 phút khác nhau để tìm tổ hợp tốt nhất.

- Tối ưu tỷ lệ cắt lỗ/chốt lời. Thử nghiệm các điểm cắt lỗ, chốt lời khác nhau để đạt tỷ suất lợi nhuận tối ưu.

- Thêm bộ lọc. Ví dụ kết hợp với khối lượng để tránh tổn thất từ phá vỡ giả.

- Thêm chỉ báo nến. Ví dụ xác nhận thân nến qua vị trí giá đóng cửa, độ dài râu nến để giảm tỷ lệ lỗi.

Tổng kết

Chiến lược này đã thành công sử dụng chỉ báo độ lệch chuẩn có trọng số, kết hợp với đường trung bình động xác định hướng, để theo dõi xu hướng của tiền điện tử. Đồng thời, thiết lập cắt lỗ và chốt lời hợp lý giúp nắm bắt nhịp thị trường, tránh tổn thất do đảo chiều quá mức. Bằng cách điều chỉnh tham số và xác nhận đa chỉ báo, có thể tối ưu hóa thêm và hình thành chiến lược giao dịch định lượng đáng tin cậy.

/*backtest

start: 2023-11-16 00:00:00

end: 2023-11-23 00:00:00

period: 45m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © rumpypumpydumpy © cache_that_pass

//@version=4- 1