Chiến lược dừng lỗ bám theo dựa trên khoảng cách giá

Tổng quan

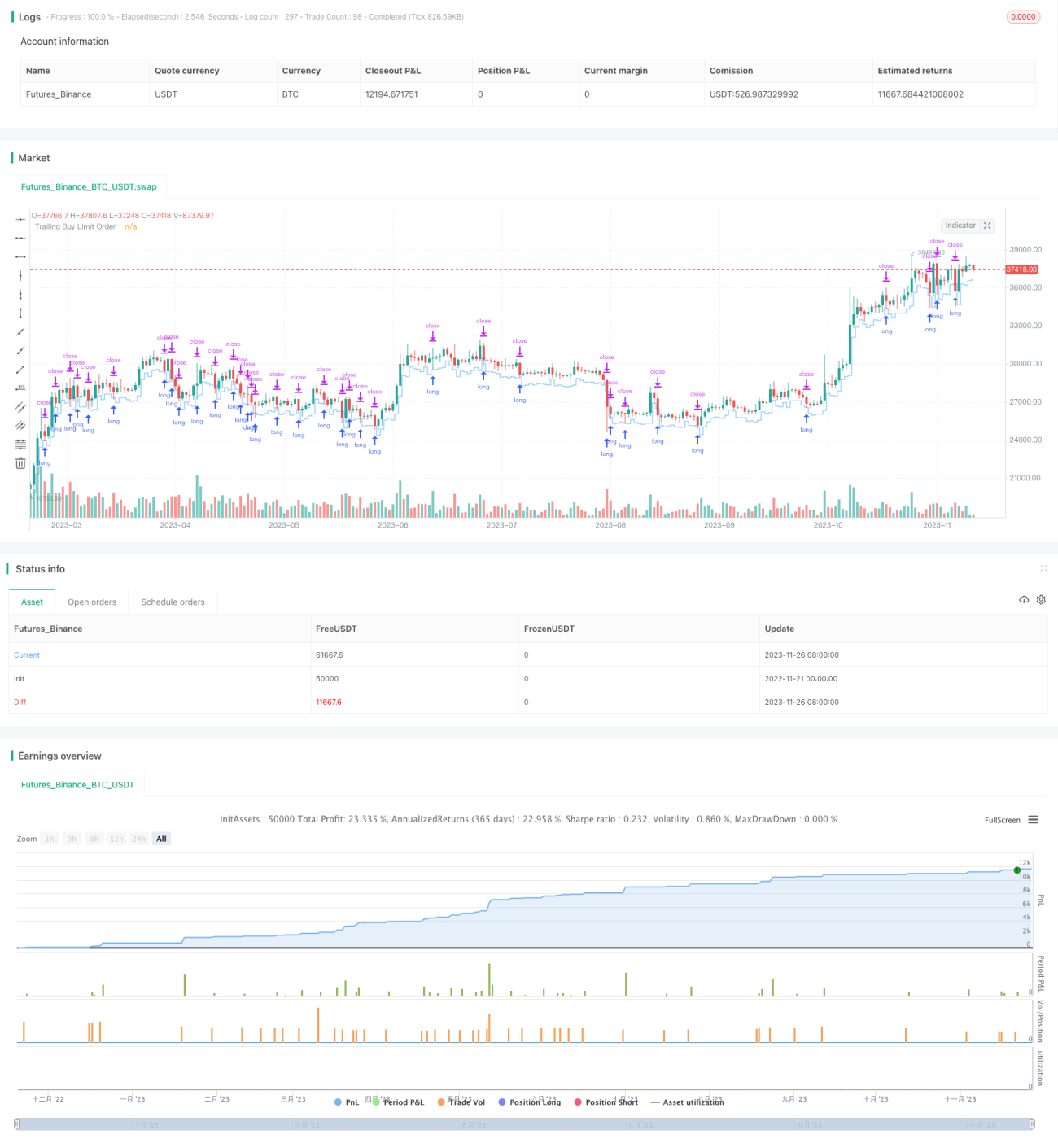

Chiến lược này áp dụng nguyên lý khoảng trống giá, mua vào khi phá vỡ đáy, thiết lập lệnh dừng lỗ và chốt lời, theo dõi đáy để dừng lỗ, nhằm đạt được lợi nhuận.

Nguyên lý chiến lược

Khi giá phá vỡ xuống dưới mức đáy trong N giờ gần nhất, xác định khoảng trống, vào lệnh long theo tỷ lệ phần trăm đã thiết lập, đồng thời đặt lệnh dừng lỗ và chốt lời. Sau đó, đường dừng lỗ và chốt lời sẽ được di chuyển theo diễn biến thị trường. Logic cụ thể như sau:

- Tính mức đáy trong N giờ làm giá neo

- Khi giá hiện tại thấp hơn giá neo nhân với tỷ lệ phần trăm mua vào, vào lệnh long

- Đặt lệnh chốt lời bằng giá vào lệnh nhân với tỷ lệ phần trăm bán ra

- Đặt lệnh dừng lời bằng giá vào lệnh trừ đi (giá vào lệnh nhân với tỷ lệ phần trăm dừng lỗ)

- Khối lượng lệnh long bằng phần trăm vốn chiến lược

- Theo dõi đáy để di chuyển đường dừng lỗ

- Đóng vị thế khi chốt lời hoặc dừng lỗ

Phân tích ưu điểm chiến lược

Chiến lược này có những ưu điểm sau:

- Áp dụng tư tưởng khoảng trống giá, vào lệnh khi phá vỡ đáy, tăng tỷ lệ thắng

- Tự động theo dõi dừng lỗ, có thể khóa phần lớn lợi nhuận

- Có thể cấu hình tỷ lệ phần trăm chốt lời/dừng lỗ, thích ứng với các thị trường khác nhau

- Phù hợp với các sản phẩm có đặc tính đảo chiều rõ rệt

- Thao tác đơn giản, dễ thực hiện

Phân tích rủi ro chiến lược

Chiến lược này cũng tồn tại một số rủi ro:

- Việc phá vỡ khoảng trống không nhất thiết thành công, có thể giảm trở lại

- Cài đặt dừng lỗ hoặc chốt lời không phù hợp có thể dẫn đến dừng lỗ/chốt lời quá sớm, bỏ lỡ xu hướng lớn hơn

- Cần tối ưu hóa tham số định kỳ để thích ứng với biến động thị trường

- Sản phẩm áp dụng có hạn, có thể không hiệu quả với một số sản phẩm

- Tồn tại nhu cầu can thiệp thủ công nhất định

Hướng tối ưu hóa chiến lược

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

- Bổ sung thuật toán học máy để tự động tối ưu hóa tham số

- Thêm nhiều phương thức dừng lỗ/chốt lời hơn, như dừng lỗ động, dừng lỗ treo, v.v.

- Tối ưu hóa logic dừng lỗ/chốt lời, thực hiện việc dừng lỗ/chốt lời thông minh và mượt mà hơn

- Kết hợp thêm nhiều chỉ báo để đánh giá độ tin cậy của tín hiệu, lọc tín hiệu nhiễu

- Mở rộng áp dụng cho nhiều sản phẩm hơn, tăng tính phổ quát của chiến lược

Kết luận

Nhìn chung, chiến lược này là một chiến lược dừng lỗ theo dõi đơn giản và hiệu quả dựa trên tư tưởng khoảng trống giá. Nó giảm xác suất vào lệnh sai, có thể khóa lợi nhuận hiệu quả, và còn nhiều không gian tối ưu về tham số cũng như lọc tín hiệu, đáng để nghiên cứu và cải tiến thêm.

/*backtest

start: 2022-11-21 00:00:00

end: 2023-11-27 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="Squeeze Backtest by Shaqi v1.0", overlay=true, pyramiding=0, currency="USD", process_orders_on_close=true, commission_type=strategy.commission.percent, commission_value=0.075, default_qty_type=strategy.percent_of_equity, default_qty_value=100, initial_capital=100, backtest_fill_limits_assumption=0)

strategy.risk.allow_entry_in(strategy.direction.long)- 1