Chiến lược đa điểm dừng lỗ đa điểm chốt lời theo xu hướng sóng

Tổng quan

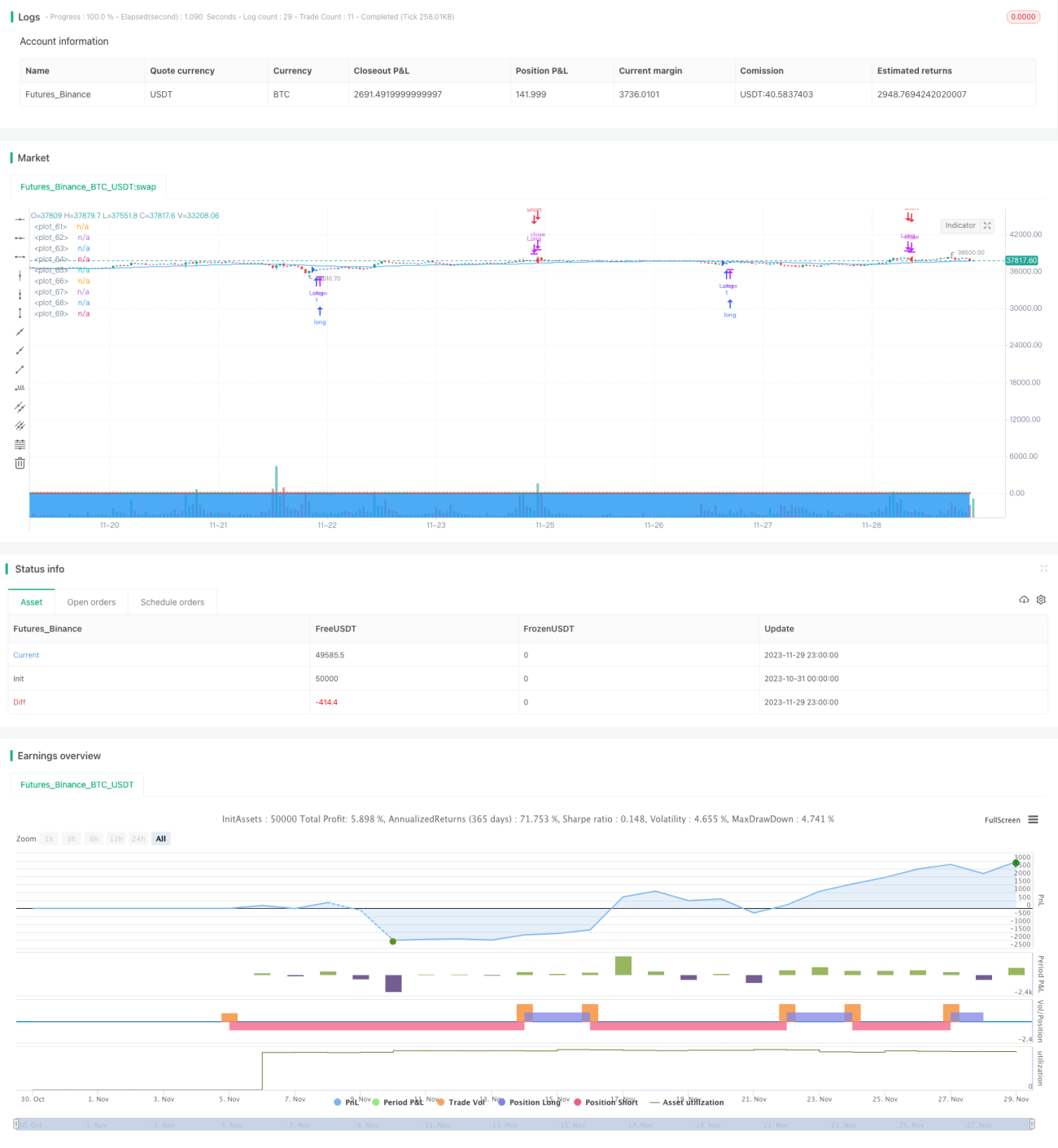

Chiến lược này là chiến lược xu hướng sóng gốc của LazyBear, được bổ sung thêm mức cắt lỗ thứ hai, nhiều mức chốt lời và bộ lọc EMA khung thời gian cao. Nó sử dụng chỉ báo xu hướng sóng để tạo tín hiệu giao dịch, kết hợp với bộ lọc EMA và quản lý cắt lỗ/chốt lời để thực hiện giao dịch theo xu hướng tự động.

Nguyên lý chiến lược

Chỉ báo cốt lõi của chiến lược là chỉ báo xu hướng sóng (WaveTrend), bao gồm ba phần:

-

AP: Giá trung bình = (Giá cao nhất + Giá thấp nhất + Giá đóng cửa) / 3

-

ESA: EMA kỳ n1 của AP

-

CI: EMA kỳ n1 của giá trị tuyệt đối của (AP – ESA) / (0,015 × EMA kỳ n1 của (AP – ESA))

-

TCI: EMA kỳ n2 của CI, tức là đường xu hướng sóng 1 (WT1)

-

WT2: SMA 4 kỳ của WT1

Khi WT1 cắt lên trên WT2 (tạo giao cắt vàng), sẽ mua lên; khi WT1 cắt xuống dưới WT2 (tạo giao cắt chết), sẽ đóng vị thế.

Ngoài ra, chiến lược còn đưa vào bộ lọc EMA khung thời gian cao: chỉ khi giá cao hơn EMA mới được mua lên, và chỉ khi giá thấp hơn EMA mới được bán khống, nhờ đó lọc bỏ một phần tín hiệu giả.

Ưu điểm chiến lược

- Sử dụng chỉ báo xu hướng sóng để tự động bám theo xu hướng, tránh sai sót do phán đoán chủ quan.

- Bổ sung mức cắt lỗ thứ hai, kiểm soát hiệu quả khoản lỗ cho mỗi giao dịch.

- Nhiều mức chốt lời, tối đa hóa lợi nhuận bị khóa.

- Bộ lọc EMA giúp lọc tín hiệu giả, tăng tỷ lệ thắng.

Rủi ro và tối ưu hóa chiến lược

- Không thể lọc được các đảo chiều xu hướng, có thể gây thua lỗ.

- Thiết lập tham số không phù hợp có thể dẫn đến giao dịch quá thường xuyên.

- Có thể thử nghiệm các bộ tham số khác nhau để tối ưu hóa.

- Có thể cân nhắc kết hợp các chỉ báo khác để xác định đảo chiều xu hướng.

Tổng kết

Chiến lược này tích hợp nhiều khía cạnh như bám xu hướng, quản lý rủi ro, tối đa hóa lợi nhuận. Bằng cách tự động phát hiện xu hướng qua chỉ báo xu hướng sóng, kết hợp bộ lọc EMA để nâng cao hiệu quả giao dịch, chiến lược kiểm soát rủi ro trong khi nắm bắt xu hướng, là một chiến lược bám xu hướng hiệu quả và ổn định. Thông qua việc tối ưu tham số và bổ sung phán đoán đảo chiều, có thể mở rộng thêm tính ứng dụng của chiến lược.

- 1