Chiến lược theo dõi động lượng tự thích ứng đa yếu tố

Tổng quan

Chiến lược theo dõi động lượng thích ứng đa yếu tố xác định xu hướng thị trường và các mức hỗ trợ/kháng cự chính thông qua việc tích hợp nhiều chỉ báo kỹ thuật, thực hiện giao dịch tự động đối với các tài sản có biến động cao như tiền điện tử. Chiến lược này kết hợp sử dụng các chỉ báo RSI, MACD, Stochastic để xác định thời điểm mua/bán, đồng thời kết hợp phần trăm thay đổi giá để nhận diện mô hình chính xác hơn.

Nguyên lý chiến lược

Cốt lõi của chiến lược theo dõi động lượng thích ứng đa yếu tố là việc tích hợp nhiều chỉ báo kỹ thuật. Chiến lược này chủ yếu sử dụng các thành phần sau:

-

Chỉ báo RSI xác định vùng quá mua/quá bán. Kết hợp các tham số khác nhau có thể nhận diện tín hiệu RSI thông thường hoặc tín hiệu Connors RSI cải tiến, từ đó xác định liệu có cơ hội đảo chiều hay không.

-

Chỉ báo MACD giúp xác định hướng xu hướng. Khi đường MACD cắt lên hoặc cắt xuống đường tín hiệu, sẽ phát sinh tín hiệu mua và bán.

-

Chỉ báo Stochastic xác định vùng quá mua/quá bán. Các tín hiệu giao cắt vàng/tử thần của đường %K và %D được sử dụng để xác định sự đảo chiều.

-

Phần trăm thay đổi giá kiểm tra sự phá vỡ thực sự. Tính toán phần trăm thay đổi của giá cao nhất, giá thấp nhất, giá đóng cửa trong một khoảng thời gian nhất định để xác định liệu có tạo thành sự phá vỡ thực sự hay không.

-

Chỉ báo EMA xác định xu hướng đa khung thời gian. Khi đường nhanh cắt lên đường chậm là tín hiệu tăng giá, cắt xuống là tín hiệu giảm giá.

Chiến lược này lựa chọn mua hoặc bán dựa trên trạng thái đa/không của thị trường, và đặt stop loss/take profit sau khi vào lệnh để kiểm soát rủi ro hiệu quả. Khi tín hiệu đảo chiều xuất hiện, chiến lược sẽ đóng vị thế. Toàn bộ quá trình ra quyết định kết hợp đầy đủ nhiều yếu tố để đạt được nhận định chính xác hơn.

Phân tích ưu điểm

Chiến lược này có những ưu điểm sau:

-

Đa yếu tố mang lại lợi thế nhận định. So với chỉ báo đơn lẻ, sự kết hợp nhiều chỉ báo có thể xác nhận lẫn nhau, giúp kết quả chính xác và đáng tin cậy hơn, từ đó tiết kiệm chi phí giao dịch không cần thiết.

-

Điều kiện chặt chẽ tránh giao dịch sai. Chiến lược đặt ra các yêu cầu nghiêm ngặt cho điều kiện mua/bán, cần nhiều chỉ báo đồng thời phát tín hiệu, do đó có thể lọc bỏ nhiễu và tránh các giao dịch sai.

-

Siêu tham số thích ứng giảm can thiệp thủ công. Chiến lược tích hợp khả năng tính toán tham số chỉ báo động, tránh tính chủ quan khi chọn siêu tham số thủ công, giúp các tham số chiến lược khoa học và khách quan hơn.

-

Cơ chế stop loss/take profit kiểm soát rủi ro. Sau khi mở vị thế, chiến lược sẽ tính toán và vẽ các mức stop loss/take profit theo thời gian thực, có thể kiểm soát hiệu quả khoản lỗ từng lệnh, tránh tình trạng cháy tài khoản.

Phân tích rủi ro

Chiến lược này cũng tồn tại một số rủi ro cần phòng tránh:

-

Xác suất chỉ báo phát tín hiệu sai. Mặc dù xác nhận nhiều chỉ báo có thể giảm đáng kể tỷ lệ tín hiệu sai, nhưng vẫn có khả năng xảy ra. Điều này có thể dẫn đến thua lỗ không cần thiết.

-

Rủi ro stop loss bị phá vỡ. Trong điều kiện thị trường cực đoan, giá có thể giảm mạnh, khiến stop loss ban đầu dễ dàng bị phá vỡ, gây ra thua lỗ lớn.

-

Tối ưu hóa tham số dẫn đến overfitting. Mặc dù tham số động tránh được tính chủ quan khi lựa chọn thủ công, nhưng cũng có thể dẫn đến tối ưu hóa quá mức, làm mất khả năng tổng quát hóa.

Các giải pháp tương ứng:

- Tăng cường độ chặt chẽ của điều kiện lọc tín hiệu, giảm tỷ lệ tín hiệu sai.

- Sử dụng phương pháp vào lệnh theo từng phần, tránh stop loss quá lớn cho một lần.

- Tăng kích thước mẫu kiểm tra, đánh giá nghiêm ngặt độ ổn định của tham số.

Hướng tối ưu hóa chiến lược

Chiến lược theo dõi động lượng thích ứng đa yếu tố còn có thể tối ưu hóa ở các khía cạnh sau:

-

Tăng số lượng yếu tố nhận định. Kết hợp thêm các tín hiệu từ các loại chỉ báo khác nhau, chẳng hạn như biến động, khối lượng giao dịch để hỗ trợ nhận định.

-

Tối ưu hóa thuật toán cơ chế stop loss. Có thể áp dụng các thuật toán stop loss tiên tiến hơn như trailing stop, volatility stop, để giảm thêm xác suất stop loss bị phá vỡ.

-

Đưa vào mô hình học máy. Sử dụng các mô hình như RNN, LSTM để mô hình hóa dữ liệu lịch sử, hỗ trợ ra quyết định mua bán.

-

Tích hợp chiến lược. Sử dụng nhiều chiến lược con và kết hợp chúng bằng phương pháp học ensemble, có thể đạt được hiệu suất tổng thể ổn định hơn.

Tổng kết

Chiến lược theo dõi động lượng thích ứng đa yếu tố tích hợp nhiều chỉ báo kỹ thuật để xác định thời điểm mua bán. So với chỉ báo đơn lẻ, chiến lược này đưa ra nhận định chính xác hơn, đồng thời tích hợp cơ chế thích ứng tham số và cơ chế stop loss để kiểm soát rủi ro. Bước tiếp theo, thông qua việc đưa vào nhiều yếu tố hỗ trợ nhận định hơn, thuật toán stop loss tiên tiến và các phương pháp học máy, có thể tăng cường hiệu quả của chiến lược này.

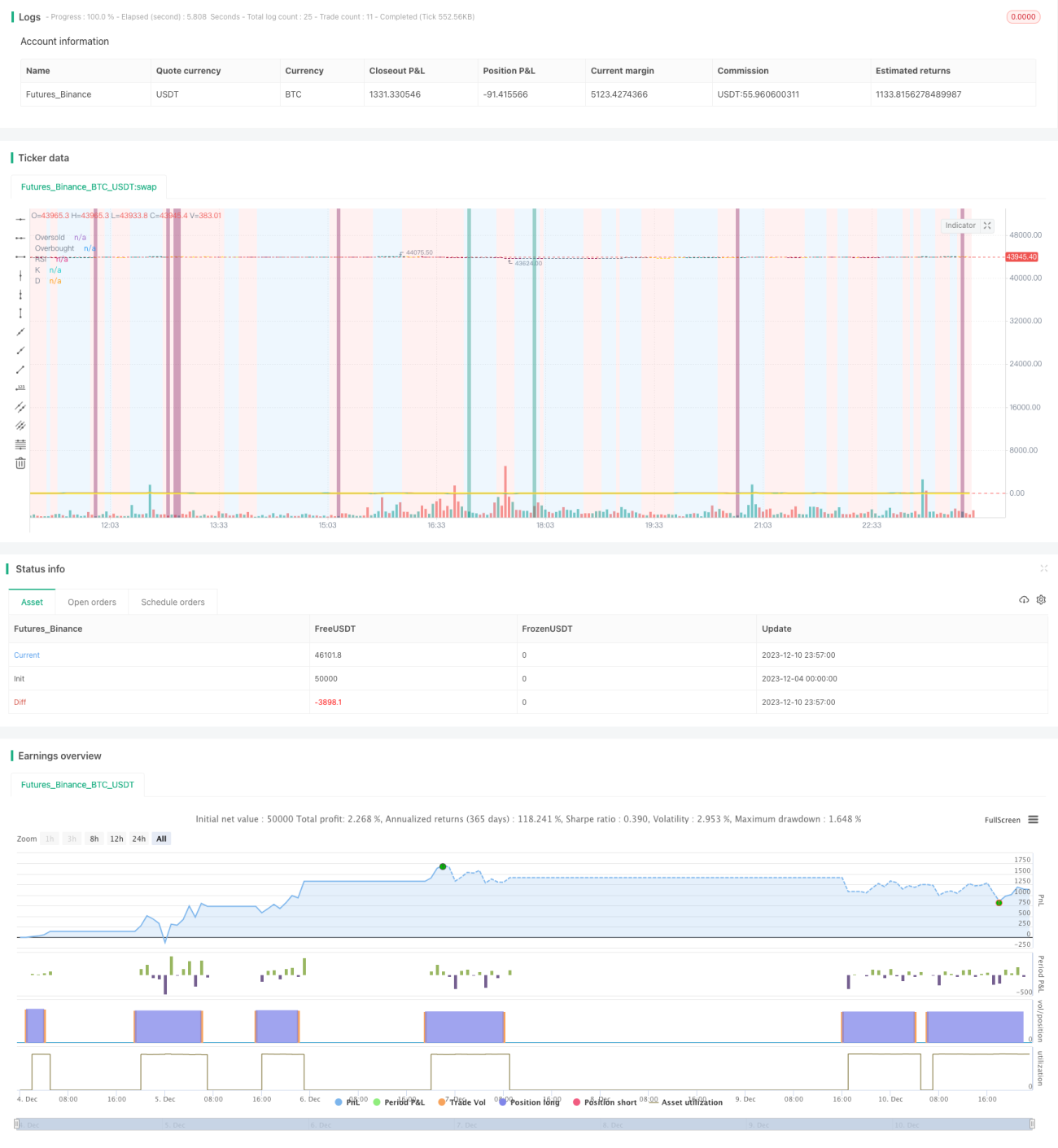

/*backtest

start: 2023-12-04 00:00:00

end: 2023-12-11 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

// ██████╗██████╗ ███████╗ █████╗ ████████╗███████╗██████╗ ██████╗ ██╗ ██╗ - 1