Chiến lược RSI dựa trên tăng cường xác suất

Tổng quan

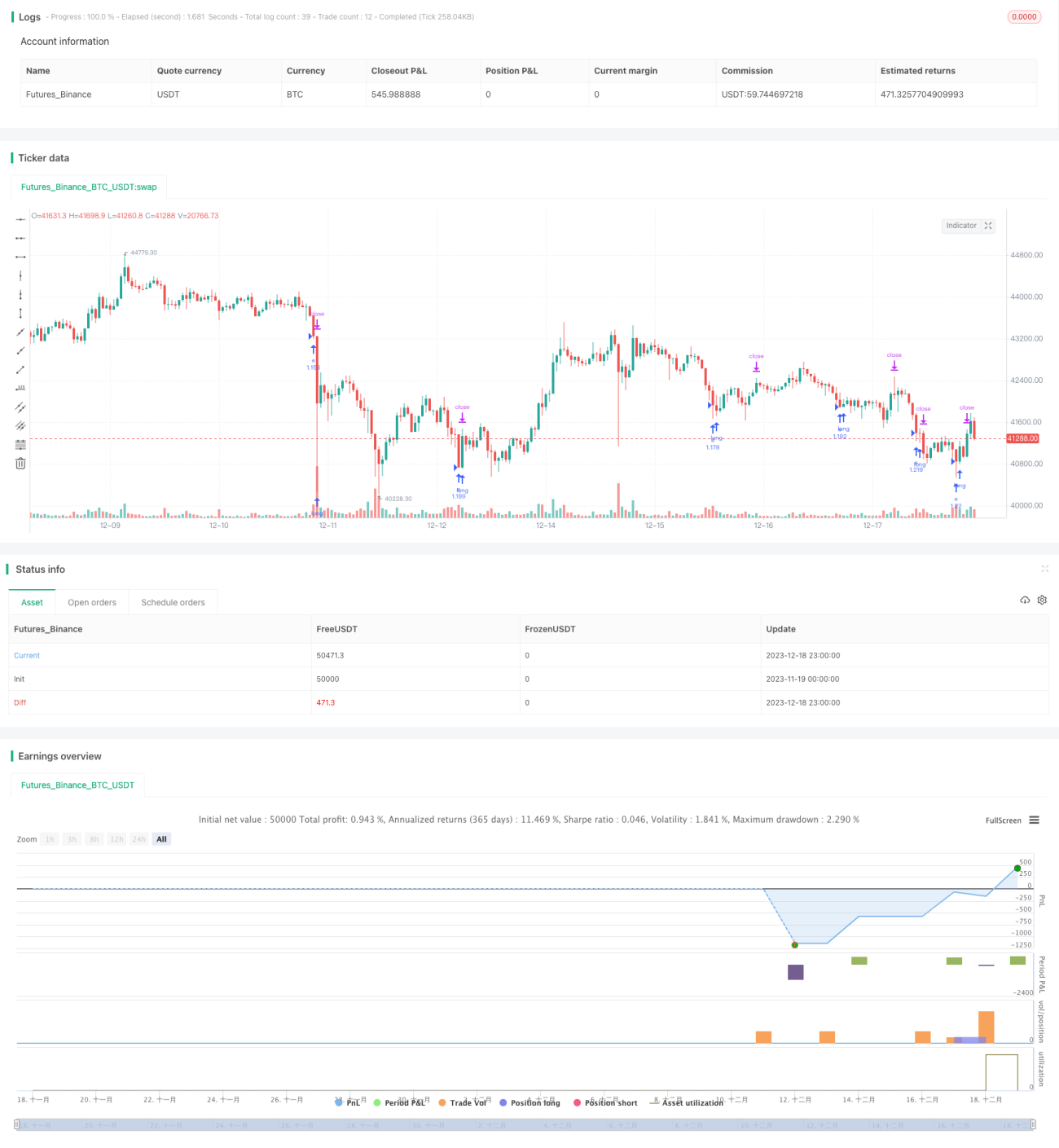

Chiến lược này là một chiến lược chỉ mua đơn giản, sử dụng chỉ báo RSI để xác định tình trạng quá mua/quá bán. Chúng tôi đã nâng cấp nó bằng cách thêm cắt lỗ và chốt lời, đồng thời tích hợp mô-đun xác suất để tăng cường hiệu quả. Chỉ khi xác suất giao dịch có lợi nhuận trong khoảng thời gian gần đây lớn hơn hoặc bằng 51% thì mới mở vị thế. Điều này cải thiện đáng kể hiệu suất của chiến lược.

Nguyên lý chiến lược

Chiến lược này sử dụng chỉ báo RSI để xác định tình trạng quá mua/quá bán của thị trường. Cụ thể, khi RSI phá vỡ xuống dưới ngưỡng vùng quá bán đã đặt, chúng ta mua vào; khi RSI phá vỡ lên trên ngưỡng vùng quá bán, chúng ta đóng vị thế. Ngoài ra, chúng tôi thiết lập tỷ lệ cắt lỗ và chốt lời.

Điểm mấu chốt là chúng tôi tích hợp một mô-đun đánh giá xác suất. Mô-đun này thống kê tỷ lệ các giao dịch mua có lãi hay lỗ trong một khoảng thời gian gần đây (được thiết lập qua tham số lookback). Chỉ khi xác suất giao dịch có lợi nhuận trong giai đoạn gần đây lớn hơn hoặc bằng 51% thì mới mở lệnh mua. Điều này giúp giảm đáng kể các giao dịch thua lỗ có thể xảy ra.

Phân tích ưu điểm

Đây là chiến lược RSI được tăng cường xác suất, có những ưu điểm sau so với chiến lược RSI thông thường:

- Bổ sung cài đặt cắt lỗ và chốt lời, giúp hạn chế thua lỗ từng giao dịch và khóa lợi nhuận.

- Tích hợp mô-đun xác suất, tránh được các thị trường vrf có xác suất sinh lời thấp.

- Tham số mô-đun xác suất có thể điều chỉnh, cho phép tối ưu hóa theo các điều kiện thị trường khác nhau.

- Cơ chế chỉ mua đơn giản, dễ hiểu và dễ thực hiện.

Phân tích rủi ro

Chiến lược này cũng tồn tại một số rủi ro:

- Chỉ mua, không thể tận dụng thị trường giảm để kiếm lợi nhuận.

- Mô-đun xác suất đánh giá không chính xác có thể bỏ lỡ các cơ hội tốt.

- Không thể xác định bộ tham số tối ưu, hiệu suất khác biệt lớn trong các điều kiện thị trường khác nhau.

- Cài đặt cắt lỗ quá rộng, thua lỗ từng giao dịch vẫn có thể lớn.

Các giải pháp tương ứng:

- Có thể xem xét thêm cơ chế bán khống.

- Tối ưu hóa tham số mô-đun xác suất, giảm xác suất đánh giá sai.

- Sử dụng phương pháp học máy để tối ưu hóa tham số động.

- Đặt mức cắt lỗ thận trọng hơn, thu hẹp khoảng thua lỗ từng giao dịch.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa thêm từ các khía cạnh sau:

- Thêm mô-đun bán khống, thực hiện giao dịch hai chiều.

- Sử dụng phương pháp học máy để tối ưu hóa động các thiết lập tham số.

- Thử các chỉ báo khác để xác định quá mua/quá bán.

- Tối ưu hóa chiến lược cắt lỗ chốt lời, cải thiện tỷ lệ lợi nhuận/rủi ro.

- Kết hợp các yếu tố lọc tín hiệu khác để tăng xác suất.

Tổng kết

Chiến lược này là một chiến lược RSI đơn giản, được tăng cường bằng mô-đun đánh giá xác suất. So với chiến lược RSI thông thường, nó có thể lọc bỏ một phần giao dịch thua lỗ, tối ưu hóa mức sụt giảm tổng thể và tỷ lệ lợi nhuận/rủi ro. Trong tương lai, có thể cải thiện từ các khía cạnh như bán khống, tối ưu hóa động, v.v., để chiến lược trở nên ổn định hơn.

- 1