Chiến lược Intraday bám xu hướng tích hợp nhiều mức cắt lỗ

Tổng quan

Chiến lược này kết hợp nhiều mức dừng lỗ động ATR và gạch Renko cải tiến, nhằm mục đích bắt kịp xu hướng trong ngày (Intraday). Nó kết hợp các chỉ báo xu hướng và chỉ báo gạch, thực hiện phân tích đa khung thời gian, có thể xác định hiệu quả hướng xu hướng và kịp thời cắt lỗ.

Nguyên lý chiến lược

Cốt lõi của chiến lược này nằm ở cơ chế dừng lỗ đa ATR. Nó thiết lập 3 nhóm dừng lỗ động ATR, với các tham số lần lượt là ATR gấp 5 lần, ATR gấp 10 lần và ATR gấp 15 lần. Khi giá phá vỡ các đường dừng lỗ này, điều đó cho thấy xu hướng đã thay đổi và lúc đó sẽ đóng vị thế. Thiết lập đa dừng lỗ như vậy có thể lọc hiệu quả các tín hiệu giả do biến động ngắn hạn gây ra.

Phần cốt lõi khác là gạch Renko cải tiến. Loại gạch này phân chia mức tăng dựa trên giá trị ATR, kết hợp với chỉ báo SMA để xác định hướng xu hướng. Nó nhạy hơn so với gạch Renko thông thường, có thể xác nhận sự thay đổi xu hướng sớm hơn. Khi màu sắc của gạch thay đổi, điều đó cho thấy xu hướng chuyển biến, có thể dùng làm tín hiệu dừng lỗ.

Điều kiện vào lệnh: khi giá phá vỡ lên trên 3 nhóm dừng lỗ ATR thì mua lên (long), khi giá phá vỡ xuống dưới 3 nhóm dừng lỗ ATR thì bán xuống (short). Điều kiện thoát lệnh: khi giá chạm vào bất kỳ một trong các nhóm dừng lỗ ATR hoặc màu sắc gạch Renko thay đổi thì đóng vị thế.

Lợi thế của chiến lược

- Đa dừng lỗ ATR, kiểm soát rủi ro hiệu quả.

- Gạch Renko cải tiến, nhạy hơn, có thể cắt lỗ sớm.

- Kết hợp chỉ báo xu hướng và chỉ báo gạch, đảm bảo bắt kịp xu hướng.

- Phân tích đa khung thời gian, xác định hướng xu hướng đáng tin cậy hơn.

- Các tham số có thể điều chỉnh, thích ứng với các môi trường thị trường khác nhau.

Rủi ro chiến lược và tối ưu hóa

Rủi ro chính của chiến lược này nằm ở việc lỗ có thể mở rộng do dừng lỗ bị phá vỡ. Có thể tối ưu hóa bằng các phương pháp sau:

- Điều chỉnh bội số dừng lỗ ATR: ở thị trường xu hướng mạnh có thể nới lỏng phù hợp; khi xu hướng yếu nên thắt chặt hơn.

- Điều chỉnh tham số chu kỳ ATR của gạch Renko để cân bằng giữa độ nhạy và độ ổn định.

- Thêm các chỉ báo dừng lỗ khác, như kênh Donchian, để đảm bảo dừng lỗ đáng tin cậy hơn.

- Thêm bộ lọc để tránh giao dịch quá thường xuyên trong giai đoạn đi ngang.

Tổng kết

Nhìn chung chiến lược này phù hợp với các đợt xu hướng mạnh trong ngày (Intraday), đặc điểm là thiết lập dừng lỗ khoa học, chỉ báo gạch có thể nhận biết sớm sự thay đổi xu hướng. Bằng cách điều chỉnh tham số, nó có thể thích ứng với các môi trường thị trường khác nhau, là một chiến lược theo xu hướng đáng được kiểm chứng thực tế.

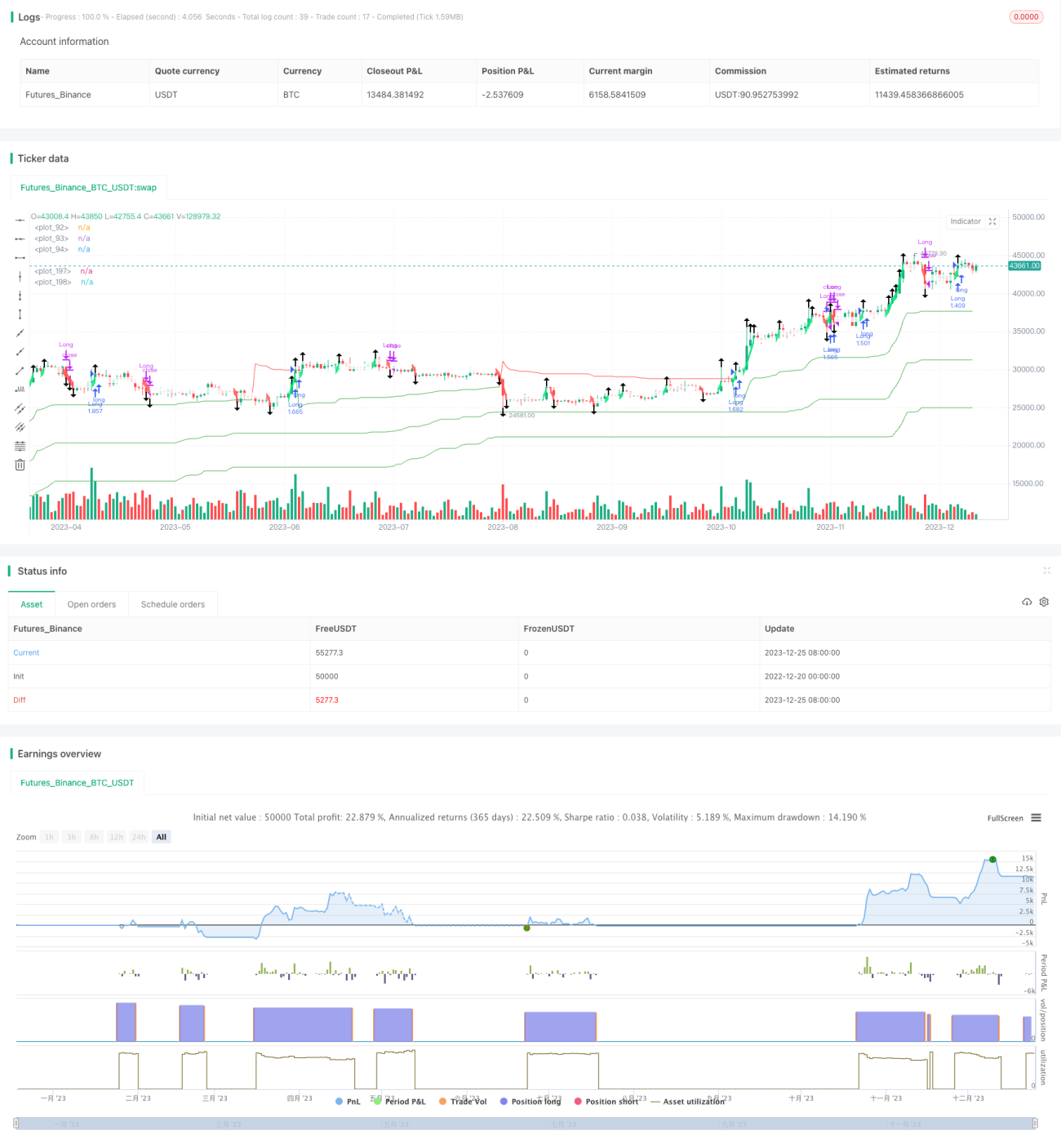

/*backtest

start: 2022-12-20 00:00:00

end: 2023-12-26 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Lancelot vstop intraday strategy", overlay=true, currency=currency.NONE, initial_capital = 100, commission_type=strategy.commission.percent,

commission_value=0.075, default_qty_type = strategy.percent_of_equity, default_qty_value = 100)

- 1