Chiến lược giao dịch dựa trên sự giao cắt của hai đường trung bình động

Tổng quan

Chiến lược này dựa trên giao cắt vàng và giao cắt tử thần của đường trung bình động để tạo ra tín hiệu mua và bán. Cụ thể, chiến lược sử dụng đồng thời đường trung bình động hàm mũ 5 ngày (EMA) và đường trung bình động hàm mũ kép 34 ngày (DEMA). Khi EMA ngắn hạn 5 ngày vượt lên trên DEMA dài hạn 34 ngày từ dưới lên, tín hiệu mua được tạo ra; khi EMA ngắn hạn 5 ngày cắt xuống dưới DEMA dài hạn 34 ngày từ trên xuống, tín hiệu bán được tạo ra.

Nguyên lý chiến lược

- Tính toán EMA 5 ngày và DEMA 34 ngày

- Khi EMA ngắn hạn 5 ngày vượt lên trên DEMA dài hạn 34 ngày từ dưới lên, tín hiệu mua được tạo ra

- Khi EMA ngắn hạn 5 ngày cắt xuống dưới DEMA dài hạn 34 ngày từ trên xuống, tín hiệu bán được tạo ra

- Có thể lựa chọn chỉ giao dịch trong khung thời gian giao dịch cụ thể

- Có thể lựa chọn có sử dụng trailing stop loss hay không

Chiến lược này kết hợp đồng thời hai yếu tố là theo xu hướng và giao cắt đường trung bình, mang lại hiệu quả ổn định. Đường trung bình động, với tư cách là một chỉ báo theo xu hướng, có thể nhận diện hiệu quả xu hướng thị trường; sự kết hợp giữa EMA và DEMA có thể làm mượt dữ liệu giá để tạo ra tín hiệu giao dịch; giao cắt giữa đường trung bình ngắn hạn và dài hạn có thể đưa ra tín hiệu giao dịch sớm khi xu hướng lớn thay đổi.

Phân tích ưu điểm

- Tư tưởng chiến lược đơn giản, rõ ràng, dễ hiểu và thực hiện

- Kết hợp các đường trung bình động, vừa xét đến việc đánh giá xu hướng, vừa xét đến việc làm mượt dữ liệu giá

- Giao cắt giữa đường trung bình ngắn hạn và dài hạn có thể đưa ra tín hiệu giao dịch sớm tại các điểm đảo chiều lớn của thị trường

- Có thể tối ưu hóa tham số, điều chỉnh độ dài đường trung bình để phù hợp với các loại tài sản và chu kỳ khác nhau

- Tích hợp hai yếu tố có thể tăng tính ổn định của chiến lược

Phân tích rủi ro

- Trong thị trường đi ngang (sideways), có thể xuất hiện nhiều tín hiệu sai

- Độ dài đường trung bình không phù hợp có thể dẫn đến độ trễ tín hiệu

- Cài đặt thời gian giao dịch và stop loss không phù hợp có thể ảnh hưởng đến lợi nhuận của chiến lược

Có thể giảm thiểu các rủi ro này bằng cách điều chỉnh độ dài đường trung bình, tối ưu hóa thời gian giao dịch và thiết lập stop loss hợp lý.

Hướng tối ưu hóa

- Điều chỉnh tham số độ dài đường trung bình để phù hợp với các loại tài sản và chu kỳ giao dịch khác nhau

- Tối ưu hóa tham số thời gian giao dịch, giao dịch trong các khung thời gian hoạt động chính

- So sánh ưu nhược điểm giữa stop loss cố định và trailing stop loss

- Kiểm tra ảnh hưởng của các phương pháp lấy giá khác nhau đối với chiến lược

Tổng kết

Chiến lược này tạo ra tín hiệu giao dịch dựa trên giao cắt của hai đường trung bình động, đồng thời kết hợp theo dõi xu hướng và làm mượt dữ liệu, là một chiến lược theo xu hướng đơn giản và thiết thực. Thông qua việc tối ưu hóa tham số và điều chỉnh quy tắc, có thể thích ứng với các loại tài sản và chu kỳ giao dịch khác nhau, đưa ra tín hiệu giao dịch sớm khi xu hướng lớn thay đổi, tránh các tín hiệu sai. Đáng để giới thiệu và áp dụng.

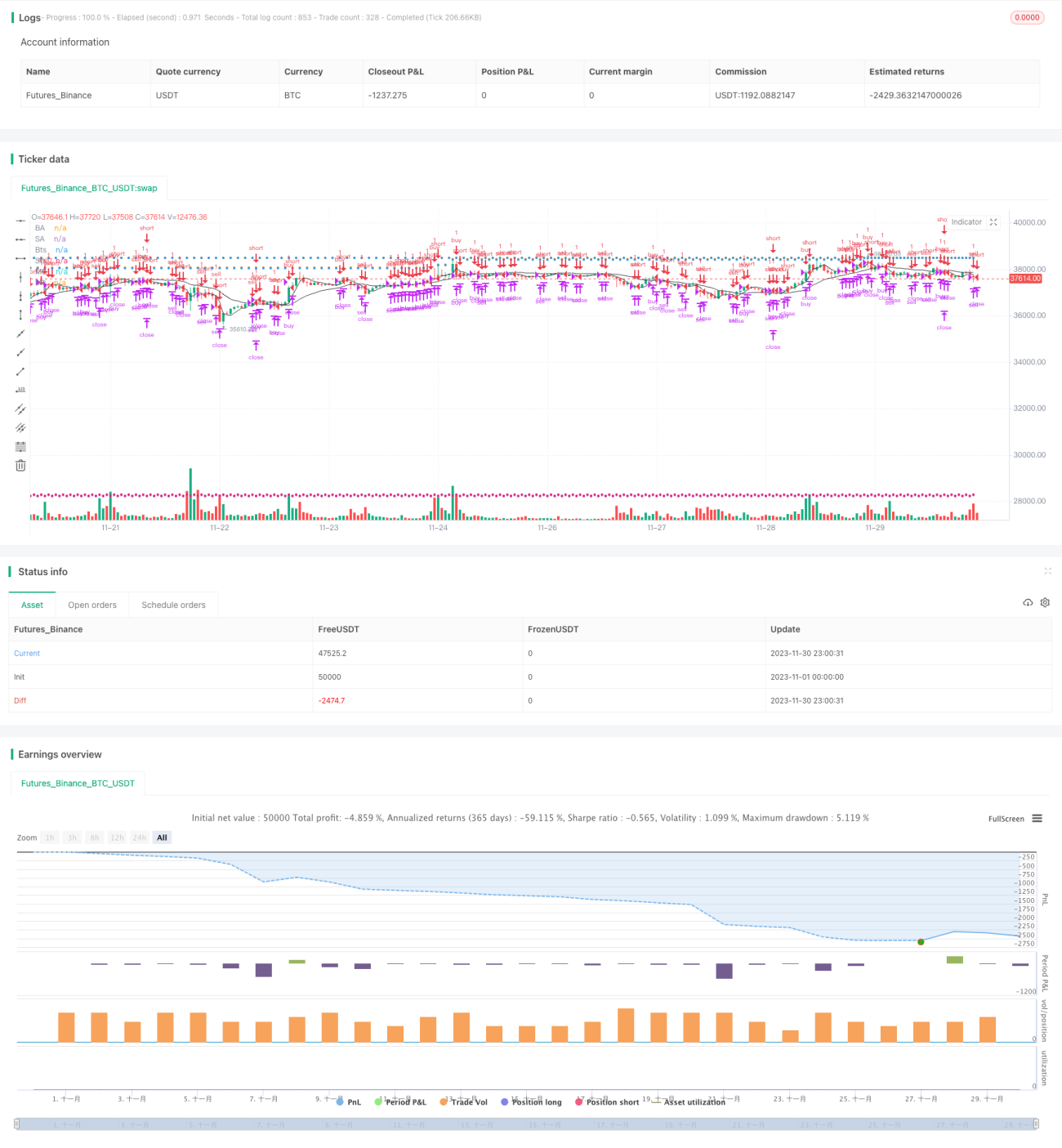

/*backtest

start: 2023-11-01 00:00:00

end: 2023-11-30 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

args: [["v_input_1",false]]

*/

//@version=2

strategy(title='[STRATEGY][RS]MicuRobert EMA cross V2', shorttitle='S', overlay=true)

USE_TRADESESSION = input(title='Use Trading Session?', type=bool, defval=true)- 1