Chiến lược kiên nhẫn bám theo xu hướng

Tổng quan

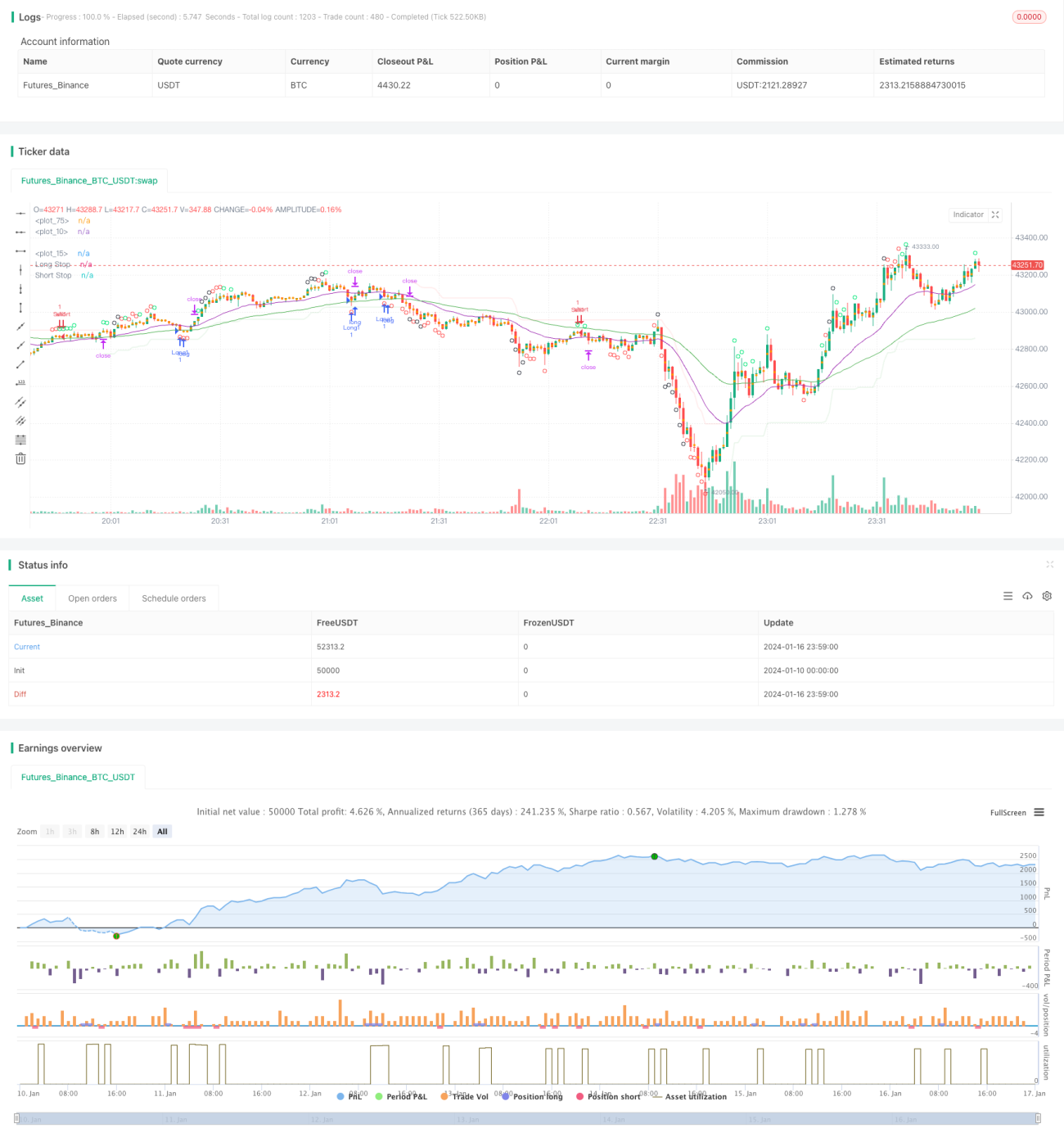

Chiến lược Kiên nhẫn Theo dõi Xu hướng là một chiến lược theo xu hướng. Nó sử dụng tổ hợp các chỉ báo đường trung bình động để xác định hướng xu hướng, kết hợp với chỉ báo quá mua/quá bán CCI để phát tín hiệu giao dịch. Chiến lược này theo đuổi xu hướng lớn và có thể tránh bị mắc kẹt hiệu quả trong thị trường đi ngang.

Nguyên lý chiến lược

Chiến lược này sử dụng tổ hợp EMA chu kỳ 21 và 55 để xác định hướng xu hướng. Khi EMA ngắn hạn nằm trên EMA dài hạn, được xác định là xu hướng tăng; khi EMA ngắn hạn nằm dưới EMA dài hạn, được xác định là xu hướng giảm.

Chỉ báo CCI được sử dụng để xác định tình trạng quá mua/quá bán. CCI cắt lên trên đường -100 là tín hiệu quá bán đáy, cắt xuống dưới đường 100 là tín hiệu quá mua đỉnh. Dựa trên các mức quá mua/quá bán khác nhau của chỉ báo CCI, chiến lược được chia thành ba cấp độ cường độ tín hiệu giao dịch.

Khi xác định là xu hướng tăng, nếu chỉ báo CCI phát ra tín hiệu quá bán đáy mạnh, sẽ thực hiện vào lệnh mua (long). Khi xác định là xu hướng giảm, nếu chỉ báo CCI phát ra tín hiệu quá mua đỉnh mạnh, sẽ thực hiện vào lệnh bán (short).

Đường cắt lỗ được đặt là chỉ báo SuperTrend, mục tiêu lợi nhuận được đặt là số điểm cố định.

Phân tích ưu điểm

Chiến lược này có những ưu điểm chính sau:

- Theo dõi xu hướng lớn, tránh bị mắc kẹt

- Chỉ báo CCI có thể xác định hiệu quả các điểm đảo chiều

- Đường cắt lỗ SuperTrend được thiết lập hợp lý

- Cắt lỗ cố định và chốt lời cố định, rủi ro có thể kiểm soát

Phân tích rủi ro

Chiến lược này tồn tại các rủi ro chính sau:

- Xác suất xác định sai xu hướng lớn

- Xác suất chỉ báo CCI phát ra tín hiệu giả

- Xác suất điểm cắt lỗ quá nông hoặc quá sâu dẫn đến cắt lỗ không cần thiết

- Xác suất chốt lời cố định không thể tiếp tục theo dõi xu hướng để thu lợi

Để đối phó với những rủi ro này, chúng ta có thể tối ưu hóa bằng cách điều chỉnh tham số chu kỳ EMA, tham số CCI cũng như điểm cắt lỗ và chốt lời. Đồng thời, việc đưa thêm nhiều chỉ báo để xác nhận tín hiệu chiến lược cũng rất cần thiết.

Hướng tối ưu

Các hướng tối ưu chính của chiến lược này bao gồm:

-

Kiểm tra tổ hợp của nhiều chỉ báo hơn, tìm kiếm các chỉ báo xác định xu hướng và xác nhận tín hiệu tốt hơn.

-

Sử dụng ATR để cắt lỗ và chốt lời động, nhằm theo dõi xu hướng và kiểm soát rủi ro tốt hơn.

-

Đưa vào mô hình học máy được huấn luyện dựa trên dữ liệu lịch sử để dự đoán xác suất xu hướng.

-

Điều chỉnh và tối ưu tham số cho các sản phẩm khác nhau.

Tổng kết

Chiến lược Kiên nhẫn Theo dõi Xu hướng nhìn chung là một chiến lược theo xu hướng rất thực tế. Nó sử dụng đường trung bình động để xác định hướng xu hướng lớn, chỉ báo CCI để phát hiện tín hiệu điểm đảo chiều, và đường cắt lỗ SuperTrend được thiết lập hợp lý. Thông qua việc điều chỉnh tham số và kết hợp xác nhận với nhiều chỉ báo, chiến lược này có thể được tối ưu hóa thêm và đáng để theo dõi và xác nhận trong giao dịch thực tế dài hạn.

- 1