Chiến lược theo dõi đảo chiều mô hình nến

Tổng quan

Chiến lược này xác định các mô hình nến, thực hiện tín hiệu giao dịch theo dõi, và kết hợp cơ chế chốt lời cắt lỗ để giao dịch tự động. Khi phát hiện mô hình đảo chiều, nó sẽ vào lệnh mua hoặc bán, và đóng lệnh khi đạt mức chốt lời hoặc cắt lỗ.

Nguyên lý chiến lược

-

Xác định mô hình nến: Khi kích thước thân nến nhỏ hơn ngưỡng đã đặt và giá mở cửa bằng giá đóng cửa, xác nhận là tín hiệu giao dịch theo dõi.

-

Vào lệnh mua/bán: Khi phát hiện mô hình nến đảo chiều, nếu giá đóng cửa của ngày trước cao hơn hai ngày trước đó thì mua; nếu giá đóng cửa của ngày trước thấp hơn hai ngày trước đó thì bán.

-

Chốt lời cắt lỗ: Sau khi mua, chốt lời khi giá đạt mức giá vào lệnh cộng với điểm chốt lời; sau khi bán, chốt lời khi giá đạt mức giá vào lệnh trừ điểm chốt lời; sau khi mua hoặc bán, cắt lỗ khi giá chạm mức cắt lỗ.

Ưu điểm chiến lược

-

Sử dụng mô hình nến đảo chiều có thể nắm bắt hiệu quả các điểm xoay chiều của giá cổ phiếu, tăng cường hiệu quả của tín hiệu giao dịch.

-

Kết hợp cơ chế chốt lời cắt lỗ có thể kiểm soát rủi ro hiệu quả, khóa lợi nhuận, tránh thua lỗ mở rộng.

-

Giao dịch tự động, không cần can thiệp thủ công, giảm chi phí giao dịch, nâng cao hiệu quả giao dịch.

Rủi ro chiến lược

-

Việc xác định mô hình nến có tính chủ quan nhất định, có thể xảy ra sai sót.

-

Cài đặt điểm chốt lời cắt lỗ không phù hợp có thể bỏ lỡ biến động lớn hoặc cắt lỗ quá sớm.

-

Các tham số chiến lược cần liên tục kiểm tra và tối ưu, nếu không có thể dẫn đến quá khớp.

Hướng tối ưu chiến lược

-

Tối ưu điều kiện xác định mô hình nến, kết hợp nhiều chỉ báo nến hơn để nâng cao độ chính xác.

-

Kiểm tra các sản phẩm giao dịch khác nhau, điều chỉnh điểm chốt lời cắt lỗ, tối ưu tham số.

-

Thêm thuật toán xác định nhiều tín hiệu giao dịch hơn, làm phong phú logic chiến lược.

-

Thêm mô-đun quản lý vị thế, có thể điều chỉnh linh hoạt quy mô vị thế dựa trên các chỉ báo tham chiếu.

Tổng kết

Chiến lược này xác định tín hiệu đảo chiều thông qua mô hình nến, thiết lập quy tắc chốt lời cắt lỗ, thực hiện giao dịch tự động. Chiến lược đơn giản, dễ hiểu, có giá trị thực tiễn nhất định. Tuy nhiên độ chính xác nhận diện và không gian tối ưu tham số vẫn cần được cải thiện, khuyến nghị kiểm tra và tối ưu thêm trước khi áp dụng vào tài khoản thực.

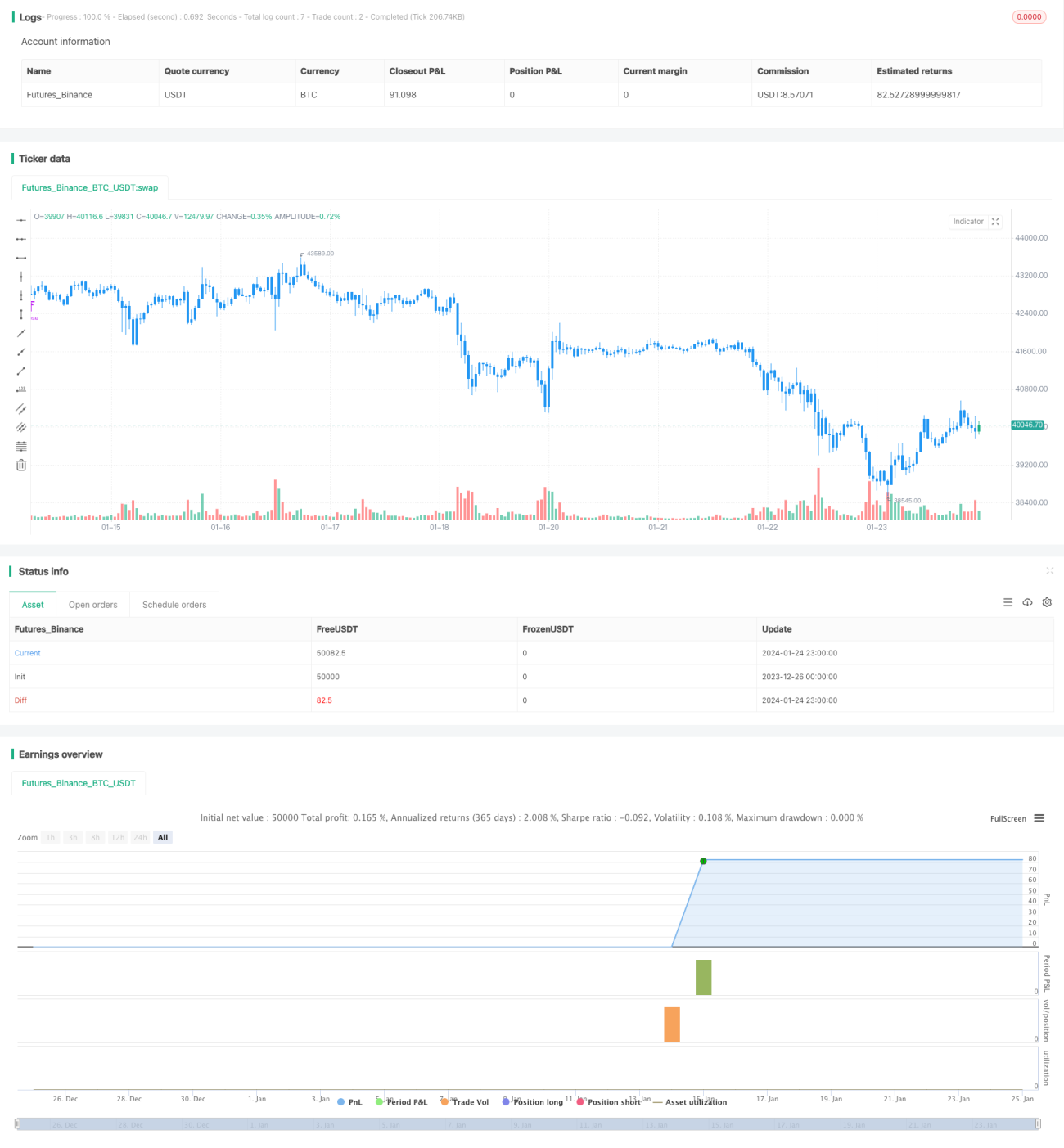

/*backtest

start: 2023-12-26 00:00:00

end: 2024-01-25 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 30/01/2019

// This is a candlestick where the open and close are the same. - 1