Một chiến lược giao dịch định lượng sử dụng nhiều chỉ báo kỹ thuật

Tổng quan

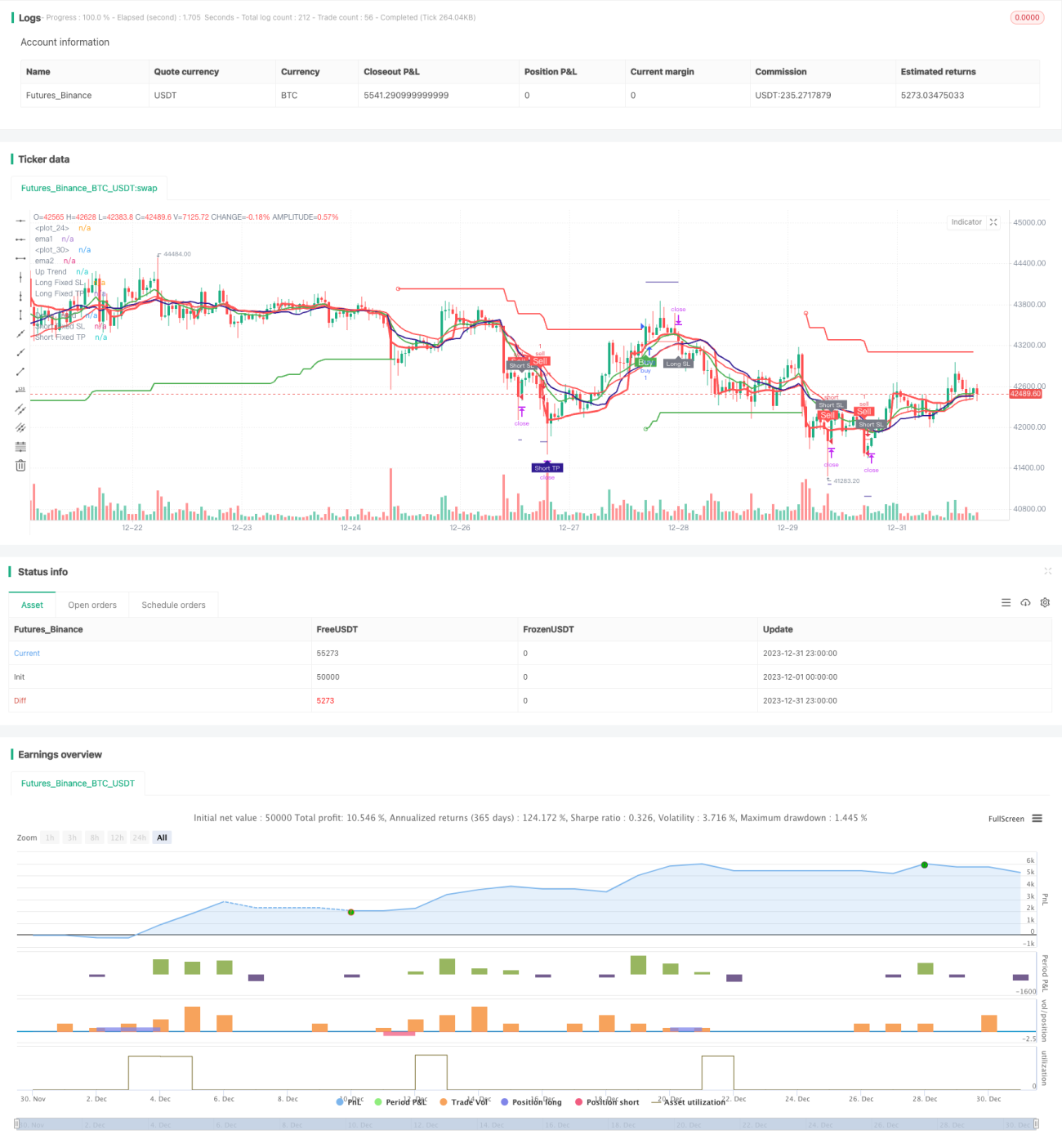

Chiến lược này là một chiến lược giao dịch định lượng sử dụng nhiều chỉ báo kỹ thuật. Chủ yếu sử dụng sự kết hợp của các chỉ báo như đường trung bình động EMA, chỉ báo SuperTrend, chỉ báo RSI, chỉ báo MACD để hình thành tín hiệu giao dịch.

Nguyên lý chiến lược

Logic giao dịch cốt lõi của chiến lược này dựa trên các khía cạnh sau:

-

Giao cắt đường EMA: Tính đường EMA nhanh (EMA1) và đường EMA chậm (EMA2). Khi đường nhanh cắt lên trên đường chậm, tạo tín hiệu mua; khi đường nhanh cắt xuống dưới đường chậm, tạo tín hiệu bán.

-

Đường trung bình VWMA: Tính đường VWMA. Khi giá đóng cửa cắt lên trên đường này, coi là tín hiệu mua; khi cắt xuống dưới, coi là tín hiệu bán.

-

Chỉ báo SuperTrend: Tính toán dải trên và dải dưới của SuperTrend dựa trên ATR và tham số multiplier, xác định hướng xu hướng. Trong xu hướng tăng, tạo tín hiệu mua; trong xu hướng giảm, tạo tín hiệu bán.

-

Chỉ báo RSI: Tính chỉ báo RSI. Khi RSI cao hơn đường quá mua, coi là tín hiệu bán; khi RSI thấp hơn vùng quá bán, coi là tín hiệu mua.

-

Chỉ báo MACD: Tính đường nhanh, đường chậm và đường tín hiệu của MACD. Khi đường nhanh cắt lên trên đường tín hiệu, tạo tín hiệu mua; khi đường nhanh cắt xuống dưới đường tín hiệu, tạo tín hiệu bán.

Sau khi có tín hiệu giao dịch từ nhiều chỉ báo trên, chiến lược sử dụng logic "AND" để đánh giá, nghĩa là chỉ khi nhiều chỉ báo đồng thời phát tín hiệu thì mới tạo tín hiệu mua và bán cuối cùng.

Ưu điểm của chiến lược

Chiến lược này kết hợp nhiều chỉ báo để đánh giá thị trường, có thể giảm hiệu quả các tín hiệu giả. Các ưu điểm chính bao gồm:

-

Sử dụng nhiều chỉ báo để lọc phức hợp, giảm thiểu tín hiệu sai do một chỉ báo duy nhất gây ra.

-

Kết hợp chỉ báo xu hướng và chỉ báo dao động, có thể thu được lợi nhuận bổ sung trong thị trường xu hướng.

-

Áp dụng logic cắt lỗ hoàn chỉnh, có thể kiểm soát hiệu quả mức thua lỗ tối đa cho mỗi giao dịch.

-

Logic gấp thếp cho phép sau khi thua lỗ có thể tăng vị thế để có cơ hội hồi vốn.

Rủi ro của chiến lược

Chiến lược này chủ yếu tồn tại các rủi ro sau:

-

Sự kết hợp nhiều chỉ báo có thể quá thận trọng, bỏ lỡ một số cơ hội giao dịch. Có thể đơn giản hóa tổ hợp chỉ báo một cách phù hợp.

-

Logic gấp thếp tăng vị thế có thể dẫn đến thua lỗ mở rộng. Cần thiết lập giới hạn số lần tăng vị thế hợp lý.

-

Vị trí cắt lỗ được thiết lập không phù hợp có thể dẫn đến cắt lỗ không cần thiết. Nên tùy chỉnh vị trí cắt lỗ thích ứng.

-

Cài đặt tham số chỉ báo không phù hợp có thể tạo ra quá nhiều tín hiệu sai. Cần tối ưu hóa tham số để có được tổ hợp tham số tốt nhất.

Hướng tối ưu hóa chiến lược

Chiến lược này có thể được tối ưu hóa thêm từ các khía cạnh sau:

-

Đánh giá hiệu quả của các tổ hợp tham số chỉ báo khác nhau, lựa chọn trọng số chỉ báo.

-

Kiểm tra các cài đặt tham số chỉ báo khác nhau.

-

Thêm logic cắt lỗ thích ứng.

-

Đưa vào cơ chế quản lý vị thế động.

-

Sử dụng phương pháp học máy để tối ưu hóa tham số và mô hình.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược giao dịch định lượng rất thực tế. Nó kết hợp ưu điểm của nhiều chỉ báo kỹ thuật kinh điển, có thể đánh giá thị trường một cách hiệu quả. Thông qua tối ưu hóa tham số và lặp lại mô hình, chiến lược này có thể đạt được hiệu quả giao dịch tốt hơn.

- 1