Chiến lược định lượng bám xu hướng dựa trên Wave Trend và VWMA

Tổng quan

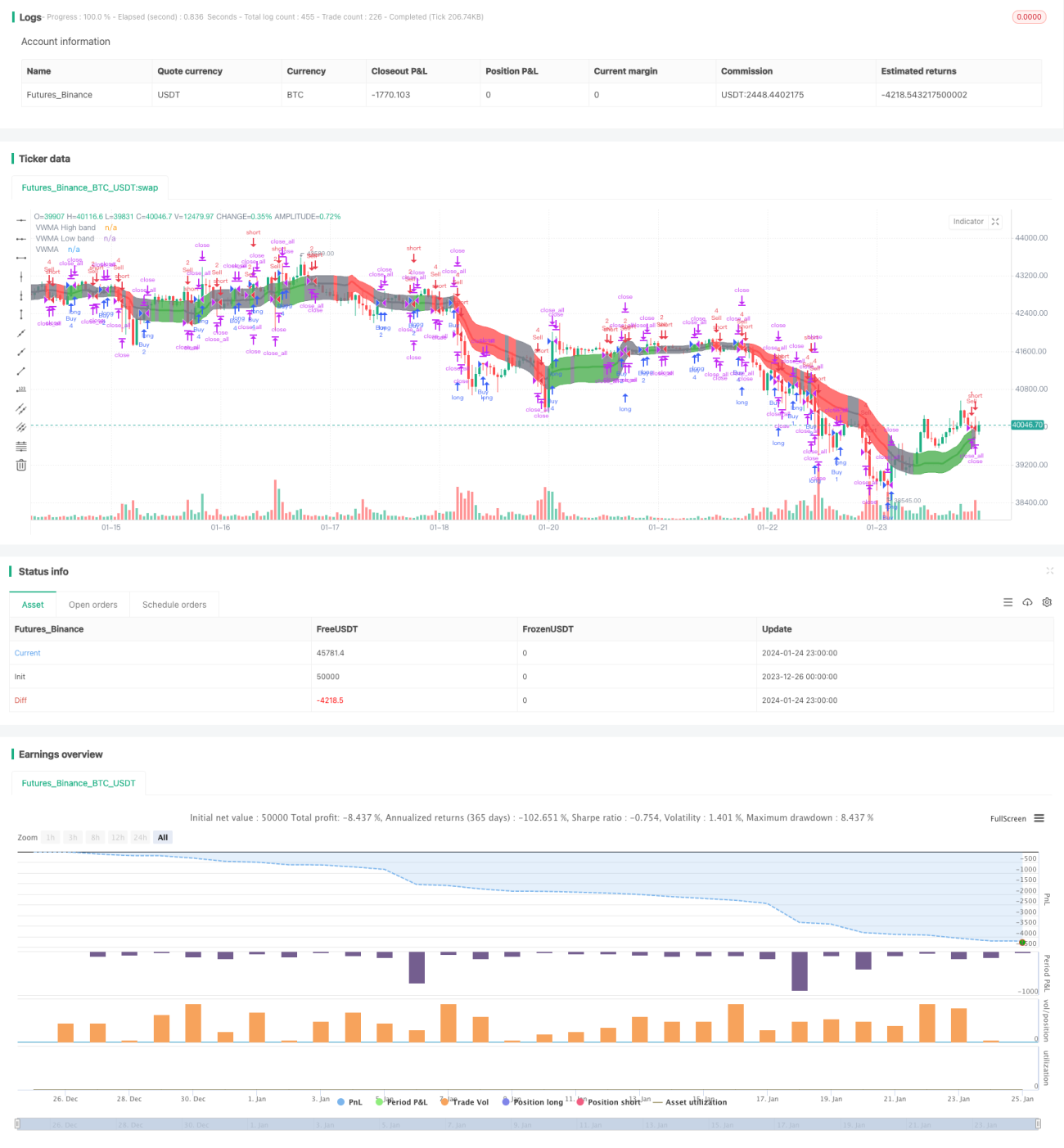

Chiến lược này kết hợp chỉ bộ dao động Wave Trend và chỉ báo VWMA để tạo thành một chiến lược giao dịch định lượng bám theo xu hướng. Chiến lược có thể nhận diện xu hướng thị trường và đưa ra tín hiệu mua hoặc bán dựa trên tín hiệu từ chỉ bộ dao động Wave Trend. Ngoài ra, khối lượng giao dịch được xác định dựa trên tín hiệu của chỉ báo VWMA.

Nguyên lý chiến lược

Chiến lược chủ yếu dựa trên hai chỉ báo sau:

-

Chỉ bộ dao động Wave Trend: Đây là chỉ báo được LazyBear chuyển sang TradingView, có thể nhận diện các "sóng" biến động giá và tạo ra tín hiệu mua/bán. Cách tính cụ thể: Đầu tiên tính giá trị trung bình ap, sau đó tính EMA của ap (gọi là esa), tiếp theo tính EMA của giá trị tuyệt đối chênh lệch giữa ap và esa (gọi là d), cuối cùng tính chỉ số nhất quán ci=(ap-esa)/(0.015*d), EMA của ci chính là Wave Trend (wt1), SMA 4 kỳ của wt1 là wt2. Khi wt1 cắt lên trên wt2 là tín hiệu mua, cắt xuống dưới là tín hiệu bán.

-

Chỉ báo VWMA: Đây là đường trung bình động có trọng số tính đến khối lượng giao dịch. Dựa vào giá nằm trong hay ngoài VWMABands (dải trên và dưới của VWMA), tạo ra tín hiệu +1 (dài hạn), 0 (trung tính) hoặc -1 (ngắn hạn).

Dựa trên tín hiệu của Wave Trend để xác định thời điểm mua và bán. Dựa trên tín hiệu dài/ngắn của chỉ báo VWMA để xác định khối lượng cụ thể cho mỗi giao dịch.

Lợi thế của chiến lược

- Kết hợp tín hiệu của hai chỉ báo giúp tăng độ chính xác khi ra quyết định

- Chỉ báo VWMA dựa trên khối lượng có thể đánh giá sức mạnh của thị trường

- Có thể tùy chỉnh khung thời gian giao dịch, tránh biến động mạnh do các sự kiện tin tức quan trọng

- Khối lượng giao dịch được điều chỉnh theo tín hiệu VWMA, giúp giảm rủi ro giao dịch

Rủi ro của chiến lược

- Chỉ bộ dao động Wave Trend có thể tạo ra tín hiệu giả

- Dữ liệu khối lượng không chính xác có thể ảnh hưởng đến chỉ báo VWMA

- Cần dữ liệu lịch sử dài để tính toán chỉ báo

- Chưa xem xét chiến lược cắt lỗ

Hướng tối ưu hóa

- Thử nghiệm các bộ tham số khác nhau để tìm ra tham số tối ưu

- Thêm chiến lược cắt lỗ

- Cân nhắc kết hợp các chỉ báo khác để lọc tín hiệu

- Thử nghiệm các cài đặt khung thời gian giao dịch khác nhau

- Điều chỉnh linh hoạt cách tính khối lượng giao dịch

Tổng kết

Chiến lược này tích hợp chỉ báo xu hướng và chỉ báo khối lượng, tạo thành một chiến lược bám theo xu hướng khá tiên tiến. Chiến lược có những lợi thế nhất định, nhưng cũng tồn tại một số rủi ro cần lưu ý. Thông qua việc tối ưu hóa tham số và quy tắc, có thể nâng cao hơn nữa tính ổn định và tỷ suất lợi nhuận của chiến lược.

- 1