Chiến lược giao dịch lưới hai chiều bám theo nến

Tổng quan

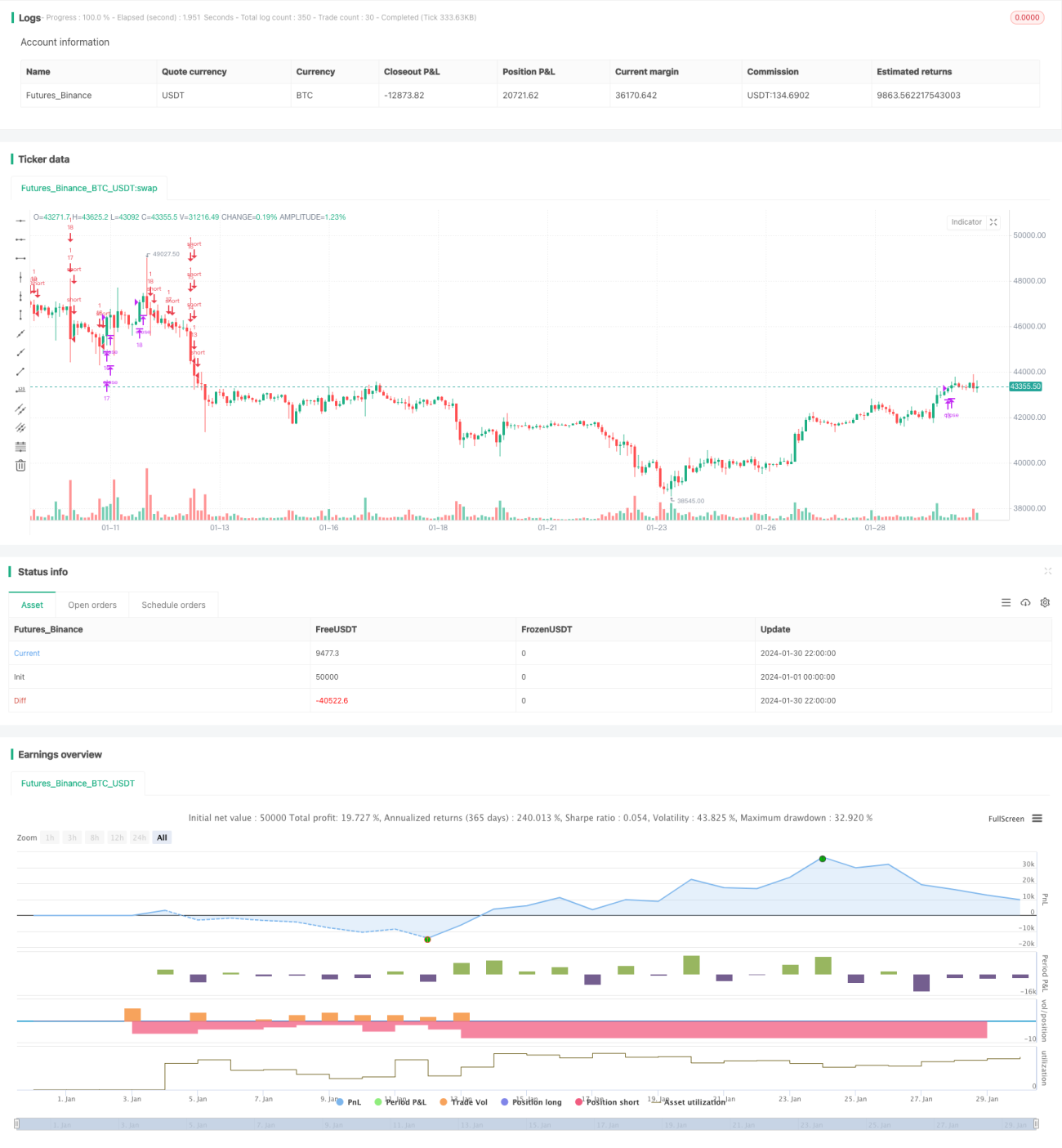

Chiến lược này là một chiến lược giao dịch lưới hai chiều dựa trên sự biến động thời gian thực của nến. Nó có thể mang lại lợi nhuận ổn định cả trong thị trường tăng và thị trường giảm.

Nguyên lý chiến lược

-

Dựa trên số lượng lưới do người dùng cài đặt, tự động tính toán khoảng giá lưới và từng mức giá lưới.

-

Khi giá vượt qua mức giá lưới, mở vị thế mua với số lượng cố định; khi giá phá vỡ mức giá lưới, đóng vị thế mua và mở vị thế bán.

-

Nhờ đó, khi giá dao động trong khoảng lưới, có thể thu lợi nhuận bằng cách theo dõi biến động giá.

Phân tích ưu điểm

-

Tự động tính toán khoảng lưới hợp lý, không cần xác định hỗ trợ/kháng cự thủ công.

-

Giao dịch hai chiều, có thể thích ứng với môi trường thị trường biến động.

-

Số lượng mở vị thế cố định, có lợi cho việc kiểm soát rủi ro.

-

Mã nguồn trực quan, đơn giản, dễ hiểu và dễ sửa đổi.

Phân tích rủi ro

-

Biến động giá mạnh có thể dẫn đến khoản lỗ gia tăng.

-

Phí giao dịch tích lũy cũng ảnh hưởng đến lợi nhuận cuối cùng.

-

Cần xác định số lượng lưới hợp lý; quá nhiều lưới làm tăng số lần giao dịch nhưng mỗi lần lợi nhuận hạn chế.

Hướng tối ưu hóa

-

Thêm chiến lược cắt lỗ để tránh lỗ lan rộng.

-

Bổ sung chức năng điều chỉnh động số lượng lưới.

-

Cân nhắc thêm đòn bẩy để khuếch đại khối lượng giao dịch.

Kết luận

Chiến lược này có tư tưởng tổng thể rõ ràng và đơn giản, đạt được lợi nhuận ổn định thông qua giao dịch lưới hai chiều, nhưng cũng tồn tại một số rủi ro giao dịch nhất định. Thông qua tối ưu hóa liên tục, có thể đạt được hiệu quả tốt hơn.

- 1