Chiến lược giao dịch đột phá dựa trên động lượng

Tổng quan

Chiến lược này là một chiến lược giao dịch phá vỡ dựa trên các chỉ báo động lượng. Nó sử dụng nhiều chỉ báo như đường trung bình động, ATR, RSI để đánh giá xu hướng thị trường và biến động, kết hợp với các thiết lập cắt lỗ và chốt lời nghiêm ngặt để thực hiện giao dịch. Chiến lược chủ yếu xác định tín hiệu giao dịch khi giá phá vỡ lên trên hoặc xuống dưới đường trung bình cộng với phạm vi ATR.

Nguyên lý chiến lược

Chiến lược này chủ yếu dựa trên các điểm sau:

-

Sử dụng đường EMA để xác định hướng xu hướng giá. Giá vượt lên trên đường trung bình là tín hiệu tăng, vượt xuống dưới là tín hiệu giảm.

-

Chỉ báo ATR đánh giá biến động thị trường. ATR nhân với một hệ số được sử dụng làm phạm vi cắt lỗ. Điều này có thể kiểm soát hiệu quả tổn thất cho mỗi giao dịch.

-

Chỉ báo RSI xác định tình trạng quá mua/quá bán. Giao dịch phá vỡ dựa trên mức cắt lỗ ATR và đường trung bình chỉ được kích hoạt khi RSI không ở vùng quá mua hoặc quá bán. Điều này giúp tránh các phá vỡ giả.

-

Sử dụng đỉnh hoặc đáy trước đó làm cơ sở chốt lời. Chốt lời theo dõi có thể khóa thêm lợi nhuận.

-

Quy tắc cắt lỗ và chốt lời nghiêm ngặt. Kết hợp với cắt lỗ ATR dựa trên chỉ báo biến động để kiểm soát rủi ro, trong khi chốt lời giúp khóa lợi nhuận.

Tín hiệu vào lệnh là khi giá phá vỡ đường trung bình cộng với phạm vi cắt lỗ ATR. Nếu là tín hiệu tăng, giá cần vượt lên trên mức cao đó; nếu là tín hiệu giảm, giá cần phá xuống dưới mức thấp đó.

Phân tích ưu điểm

Chiến lược này có những ưu điểm sau:

-

Đánh giá đa chỉ báo giúp tránh phá vỡ giả, nâng cao độ chính xác của tín hiệu.

-

Thiết lập phạm vi cắt lỗ ATR giữ cho tổn thất ở mức hợp lý.

-

Chốt lời theo dõi linh hoạt giúp tối đa hóa lợi nhuận.

-

Quy tắc cắt lỗ và chốt lời nghiêm ngặt hỗ trợ kiểm soát rủi ro.

-

Có nhiều không gian tối ưu hóa chỉ báo và tham số, có thể điều chỉnh theo các thị trường khác nhau.

Phân tích rủi ro

Chiến lược này cũng có những rủi ro sau:

-

Khả năng sinh lời phụ thuộc vào biến động thị trường. Khi thị trường không có xu hướng rõ ràng hoặc chu kỳ dài, không gian lợi nhuận bị hạn chế.

-

Có thể xảy ra trường hợp giá dao động quanh mức cắt lỗ rồi lại phá vỡ. Khi đó không thể kịp thời vào lệnh để theo dõi xu hướng. Có thể nới lỏng mức cắt lỗ một chút.

-

Rủi ro đuổi theo giá.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

-

Điều chỉnh tham số đường trung bình, tham số ATR theo từng sản phẩm và khung thời gian khác nhau.

-

Có thể đưa thêm nhiều chỉ báo đánh giá hơn như MACD, KDJ để xác định quá mua/quá bán.

-

Có thể điều chỉnh hệ số cắt lỗ theo thời gian thực dựa trên giá trị ATR, giúp cắt lỗ thích ứng hơn với biến động thị trường.

-

Xây dựng tổ hợp nhiều khung thời gian. Kết hợp các chỉ báo từ các khung thời gian khác nhau có thể nâng cao chất lượng tín hiệu.

-

Sử dụng công nghệ học máy để kiểm tra và tối ưu hóa các chỉ báo và tham số, đưa tham số chiến lược đạt mức tối ưu.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược giao dịch phá vỡ sử dụng các chỉ báo để đánh giá, với cắt lỗ và chốt lời nghiêm ngặt. Nó tận dụng hiệu quả ưu điểm của các chỉ báo như đường trung bình, ATR và RSI, có thể đánh giá hiệu quả hướng xu hướng thị trường. Kết hợp với các thiết lập cắt lỗ và chốt lời nghiêm ngặt, nó có thể nắm bắt xu hướng để kiếm lợi nhuận đồng thời kiểm soát rủi ro. Thông qua tối ưu hóa tham số và quy tắc, chiến lược này có thể trở thành một chiến lược giao dịch định lượng đáng sử dụng lâu dài.

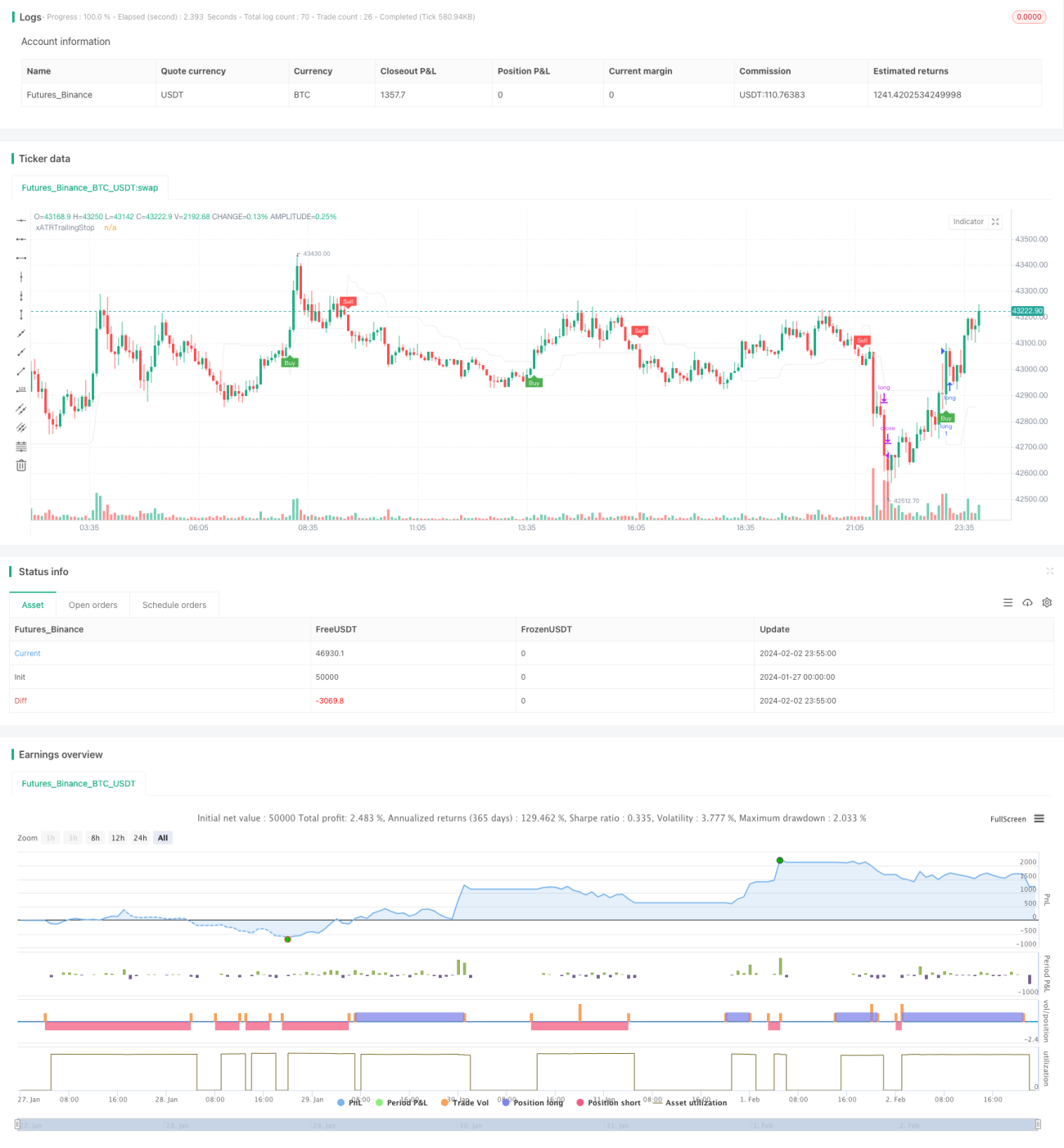

/*backtest

start: 2024-01-27 00:00:00

end: 2024-02-03 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="UT Bot Strategy", overlay = true)

//CREDITS to HPotter for the orginal code. The guy trying to sell this as his own is a scammer lol.

// Inputs- 1