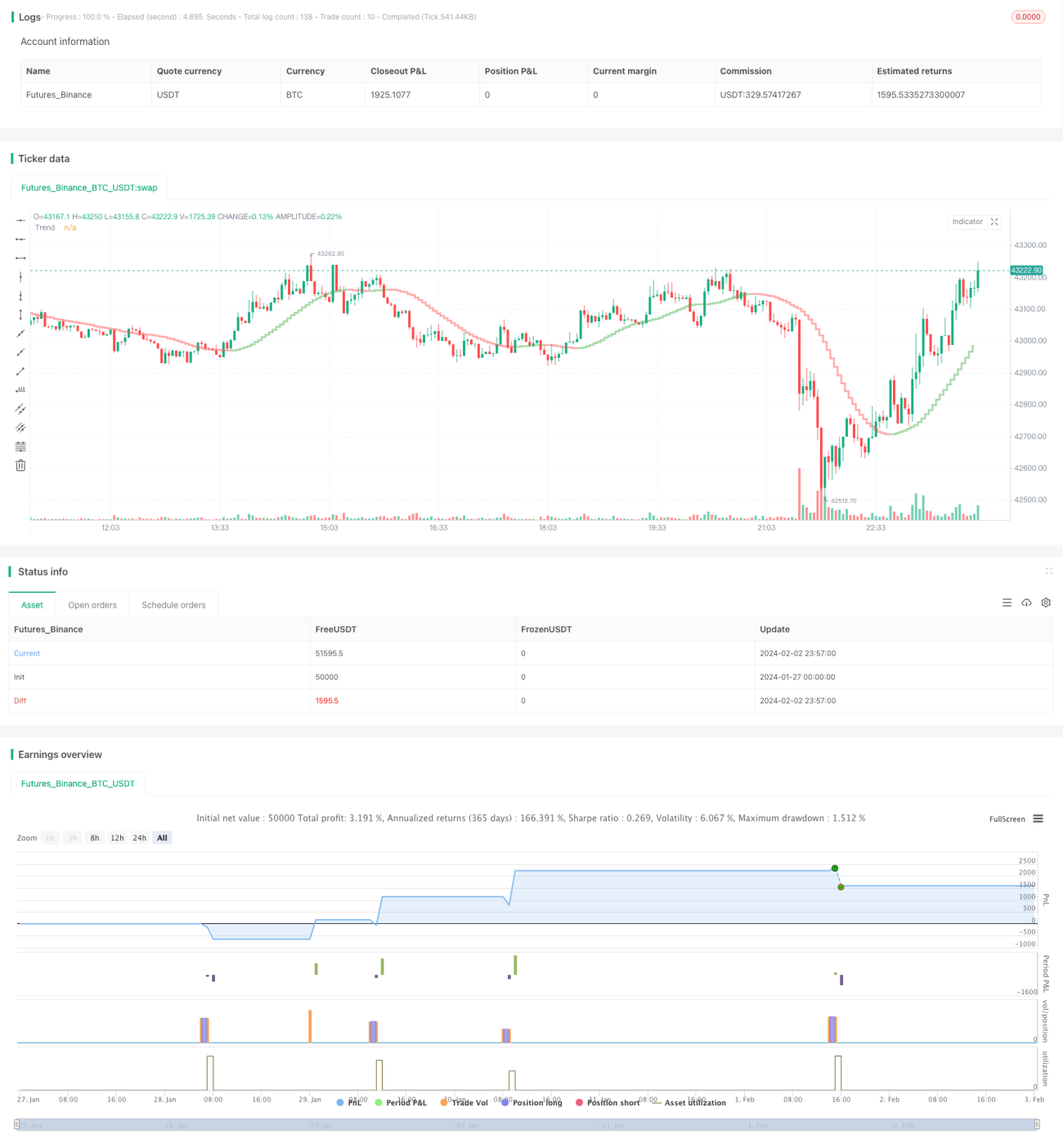

Chiến lược Ripple dựa trên chỉ báo Coral Trend trong phạm vi backtest

Tổng quan

Chiến lược này sử dụng chỉ báo Coral Trend của LazyBear để xác định hướng xu hướng giá, thông qua việc nhận diện sự đảo chiều của chỉ báo Coral Trend để phát hiện điểm vào lệnh tiềm năng. Để lọc các phá vỡ giả, chiến lược này sử dụng kết hợp chỉ báo ADX hoặc Absolute Strength Histogram và HawkEye Volume làm chỉ báo xác nhận, giúp điểm vào lệnh đáng tin cậy hơn.

Cơ chế thoát lệnh sử dụng mức giá cao nhất/thấp nhất của N nến gần nhất nhân với tỷ lệ rủi ro/lợi nhuận có thể cấu hình để thiết lập điểm cắt lỗ và chốt lời.

Nguyên lý chiến lược

Sau khi xác định hướng xu hướng chính dựa trên chỉ báo Coral Trend, khi chỉ báo giữ nguyên màu sắc, giá xuất hiện một đợt điều chỉnh nhỏ (pullback) ngược chiều. Nếu đợt điều chỉnh kết thúc và giá quay trở lại hướng xu hướng chính mà Coral Trend chỉ ra, thì đó được coi là thời điểm vào lệnh tốt.

Điều kiện vào lệnh bao gồm:

-

Hướng của chỉ báo Coral Trend phù hợp với hướng giao dịch (dài = xanh lục, ngắn = đỏ)

-

Kể từ lần cuối giá phá vỡ hoàn toàn chỉ báo Coral Trend (đỉnh của thanh cuối cùng vượt quá đường Coral Trend), đã có ít nhất 1 nến có đáy nằm hoàn toàn trên đường Coral Trend (đối với vị thế dài) hoặc đỉnh nằm hoàn toàn dưới đường Coral Trend (đối với vị thế ngắn)

-

Xảy ra đợt điều chỉnh nhỏ ngược chiều (pullback), trong đợt điều chỉnh này giá đóng cửa luôn nằm ở phía ngược lại của Coral Trend

-

Sau khi đợt điều chỉnh nhỏ kết thúc, giá đóng cửa quay trở lại hướng xu hướng chính mà Coral Trend chỉ ra

Trên đây là các điều kiện chính. Đồng thời, chiến lược sử dụng chỉ báo ADX hoặc kết hợp Absolute Strength Histogram và HawkEye Volume làm điều kiện xác nhận khi vào lệnh.

Chỉ báo ADX yêu cầu giá trị > 20 và nến gần nhất tăng. Đồng thời thứ tự của đường DI xanh và đỏ phù hợp với hướng giao dịch.

Absolute Strength Histogram yêu cầu màu sắc phù hợp với hướng giao dịch (dài = xanh lam, ngắn = đỏ). HawkEye Volume yêu cầu màu sắc phù hợp với hướng giao dịch (dài = xanh lục, ngắn = đỏ).

Cơ chế thoát lệnh sử dụng mức giá cao nhất hoặc thấp nhất của N nến gần nhất nhân với tỷ lệ rủi ro/lợi nhuận để thiết lập điểm cắt lỗ và chốt lời. Giá trị N và tỷ lệ rủi ro/lợi nhuận đều có thể cấu hình qua tham số.

Phân tích ưu điểm

Ưu điểm lớn nhất của chiến lược này là sử dụng chỉ báo Coral Trend để xác định hướng xu hướng chính, sau đó thông qua nhận diện sự đảo chiều của nó để tìm cơ hội vào lệnh, tránh bị cuốn theo thị trường không có xu hướng. Đồng thời, sử dụng chỉ báo xác nhận có thể lọc được nhiều phá vỡ giả, nhờ đó tăng tỷ lệ thành công khi vào lệnh.

Ngoài ra, chiến lược này cung cấp cơ chế quản lý rủi ro hoàn chỉnh, bao gồm thiết lập mức cắt lỗ và kiểm soát tỷ lệ rủi ro theo phần trăm, giúp ngay cả khi một giao dịch riêng lẻ thua lỗ cũng không gây tác động lớn đến tổng vốn.

Phân tích rủi ro

Rủi ro lớn nhất của chiến lược này là việc sử dụng chỉ báo để xác định điểm vào lệnh dễ gây ảo tưởng rằng hoàn toàn phụ thuộc vào cấu hình tham số là có thể tự động sinh lời. Trên thực tế, việc tối ưu hóa tham số và cấu hình quy tắc cần kết hợp với quy luật biến động giá cơ bản, trực quan đánh giá hiệu quả liên kết giữa chỉ báo và giá, mới có thể thiết lập được cấu hình phù hợp hơn với phong cách giao dịch và sản phẩm của riêng mình.

Ngoài ra, việc thiết lập điểm cắt lỗ và chốt lời cũng cần phù hợp: tỷ lệ chốt lời quá lớn có thể dẫn đến không thể chốt lời thoát lệnh, trong khi mức cắt lỗ quá nhỏ lại khiến rủi ro quá cao. Điều này cần được thiết lập dựa trên mức độ biến động của từng sản phẩm và khả năng chịu rủi ro cá nhân.

Hướng tối ưu hóa

Các hướng có thể tối ưu hóa chiến lược này bao gồm:

-

Điều chỉnh tham số của chỉ báo Coral Trend để nó phản ứng nhạy hơn với sự thay đổi giá của các sản phẩm khác nhau

-

Thử nghiệm các chỉ báo xác nhận hoặc tổ hợp chỉ báo khác như KDJ, MACD, … để tín hiệu vào lệnh chính xác hơn

-

Dựa trên mức độ biến động của từng sản phẩm, điều chỉnh phương pháp tính điểm cắt lỗ và chốt lời để kiểm soát rủi ro tốt hơn

-

Thêm mô-đun quản lý vốn, có thể điều chỉnh khối lượng lệnh dựa trên số lượng vị thế, kiểm soát hiệu quả tổng thua lỗ

-

Thêm mô-đun kiểm soát thời gian giao dịch, cho phép chiến lược chỉ chạy trong khung giờ nhất định, tránh thua lỗ trong giai đoạn biến động mạnh

Tổng kết

Chiến lược này trước hết sử dụng Coral Trend để xác định xu hướng trung và dài hạn của giá, sau đó thông qua nhận diện sự đảo chiều kết hợp với tín hiệu xác nhận để lọc phá vỡ giả, xây dựng một chiến lược bám xu hướng khá đáng tin cậy. Đồng thời, thiết lập quản lý rủi ro hoàn chỉnh giúp chiến lược có thể chạy dài hạn với vốn ổn định. Thông qua tối ưu hóa tham số và mô-đun tiếp theo, chiến lược có tiềm năng thích ứng với nhiều sản phẩm hơn, mang lại độ ổn định và khả năng sinh lời tốt hơn.

- 1