Chiến lược theo dõi xu hướng dựa trên chỉ báo SMA đa chu kỳ

Tổng quan

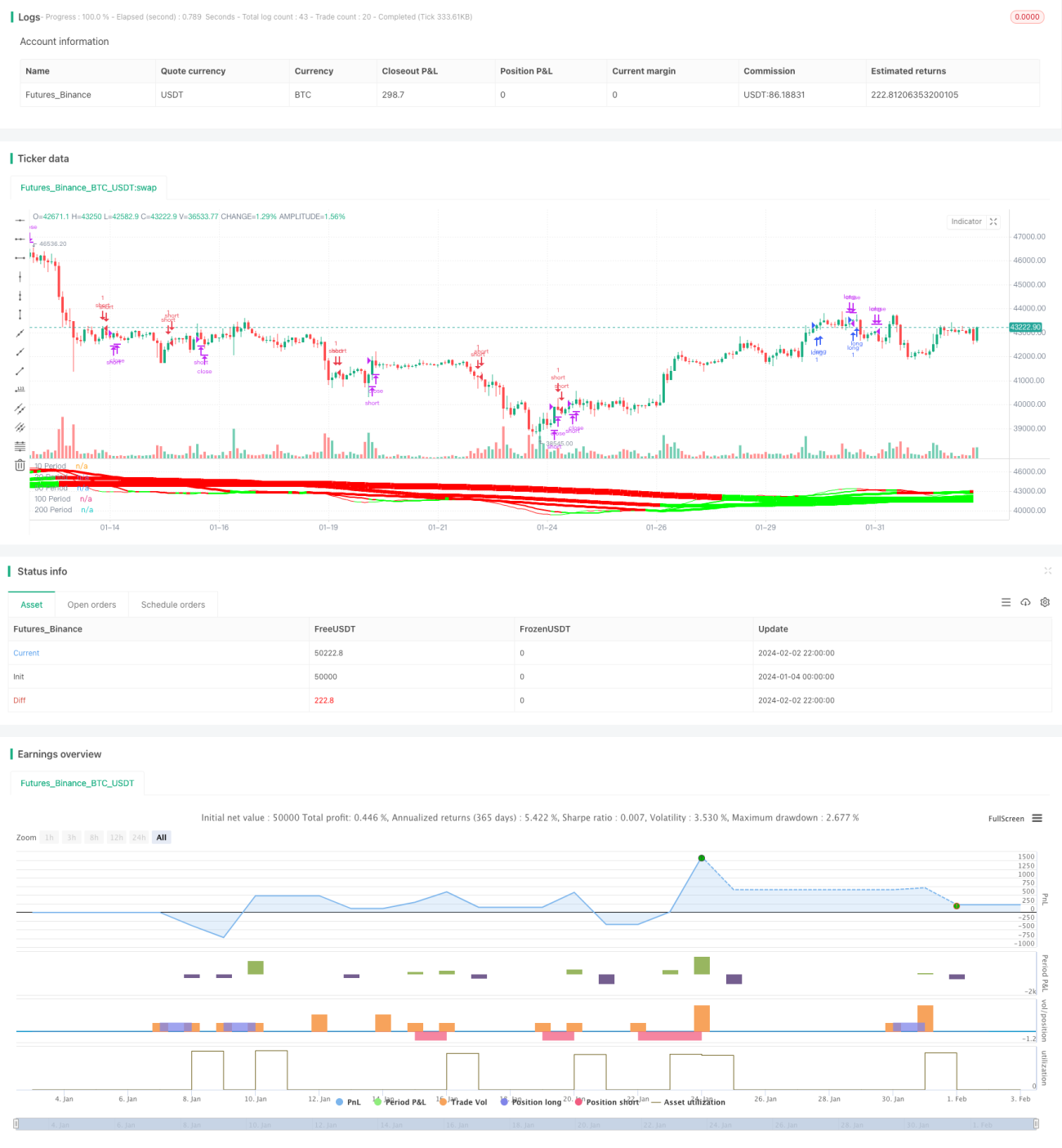

Chiến lược này kết hợp sử dụng nhiều đường SMA với các chu kỳ khác nhau để đánh giá và bám theo xu hướng. Ý tưởng cốt lõi: so sánh hướng tăng/giảm của các đường SMA với chu kỳ khác nhau để xác định xu hướng; khi đường SMA chu kỳ ngắn cắt lên đường SMA chu kỳ dài hơn thì mua (long); khi đường SMA chu kỳ ngắn cắt xuống đường SMA chu kỳ dài hơn thì bán (short). Đồng thời, kết hợp chỉ báo ZeroLagEMA để xác nhận điểm vào và thoát lệnh.

Nguyên lý chiến lược

- Sử dụng 5 đường SMA với các chu kỳ khác nhau: 10 chu kỳ, 20 chu kỳ, 50 chu kỳ, 100 chu kỳ và 200 chu kỳ.

- So sánh hướng tăng và giảm của 5 đường trung bình này để xác định hướng xu hướng. Ví dụ, khi các đường SMA 10 chu kỳ, 20 chu kỳ, 100 chu kỳ và 200 chu kỳ đồng thời tăng thì nhận định là xu hướng tăng; khi các đường đồng thời giảm thì nhận định là xu hướng giảm.

- So sánh giá trị của các đường SMA với chu kỳ khác nhau để hình thành tín hiệu giao dịch. Ví dụ, khi SMA 10 chu kỳ cắt lên SMA 20 chu kỳ thì mua (long) – tín hiệu vào lệnh; khi SMA 10 chu kỳ cắt xuống SMA 20 chu kỳ thì bán (short) – tín hiệu vào lệnh.

- Sử dụng ZeroLagEMA làm tín hiệu xác nhận vào lệnh và thoát lệnh. Khi ZeroLagEMA chu kỳ nhanh cắt lên chu kỳ chậm thì mua (long); cắt xuống thì đóng vị thế long. Cách xác định tín hiệu bán (short) ngược lại.

Ưu điểm của chiến lược

- Sử dụng tổ hợp nhiều đường SMA với các chu kỳ khác nhau giúp đánh giá hiệu quả hướng xu hướng thị trường.

- Việc so sánh giá trị các đường SMA chu kỳ có thể tạo ra tín hiệu giao dịch, hình thành các quy tắc vào và thoát lệnh định lượng.

- Bộ lọc ZeroLagEMA giúp tránh các giao dịch không cần thiết, nâng cao độ ổn định của chiến lược.

- Kết hợp đánh giá xu hướng và tín hiệu giao dịch, thực hiện giao dịch bám theo xu hướng.

Rủi ro và giải pháp

- Khi thị trường bước vào giai đoạn tích lũy dao động, tín hiệu từ các đường SMA có thể xuất hiện giao cắt thường xuyên, dẫn đến nhiều giao dịch không hiệu quả và rủi ro thua lỗ.

- Giải pháp: Tăng tham số lọc của ZeroLagEMA để tránh vào lệnh theo các tín hiệu không hiệu quả.

- Vì tham khảo nhiều chu kỳ SMA, tín hiệu có độ trễ nhất định, không thể phản ứng kịp thời với các biến động giá mạnh trong ngắn hạn.

- Giải pháp: Kết hợp các chỉ báo nhạy hơn như MACD để hỗ trợ đánh giá.

Hướng tối ưu hóa chiến lược

- Tối ưu hóa tham số chu kỳ SMA để tìm ra tổ hợp tham số tốt nhất.

- Bổ sung chiến lược dừng lỗ, như trailing stop, để kiểm soát thêm mức thua lỗ trên mỗi lệnh.

- Thêm cơ chế quản lý khối lượng vị thế, để chiến lược tăng quy mô khi xu hướng mạnh và giảm quy mô khi thị trường dao động.

- Kết hợp thêm các chỉ báo hỗ trợ khác như MACD, KDJ để nâng cao độ ổn định tổng thể của chiến lược.

Tổng kết

Chiến lược này thông qua tổ hợp nhiều đường SMA với các chu kỳ khác nhau đã đánh giá hiệu quả hướng xu hướng thị trường và tạo ra các tín hiệu giao dịch định lượng. Đồng thời, việc áp dụng ZeroLagEMA đã nâng cao tỷ lệ thành công của chiến lược. Nhìn chung, chiến lược đã thực hiện được ý tưởng giao dịch định lượng dựa trên bám theo xu hướng, hiệu quả rõ rệt. Thông qua việc tối ưu hóa thêm tham số chu kỳ SMA, chiến lược dừng lỗ, quản lý vị thế,... có thể nâng cao hơn nữa hiệu quả của chiến lược, đáng để kiểm chứng và ứng dụng trong giao dịch thực tế.

/*backtest

start: 2024-01-04 00:00:00

end: 2024-02-03 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Forex MA Racer - SMA Performance /w ZeroLag EMA Trigger", shorttitle = "FX MA Racer (5x SMA, 2x zlEMA)", overlay=false )

// === INPUTS ===- 1