Chiến lược theo dõi xu hướng dải Bollinger thích ứng hai chiều

1

Follow

1802

Followers

Tổng quan

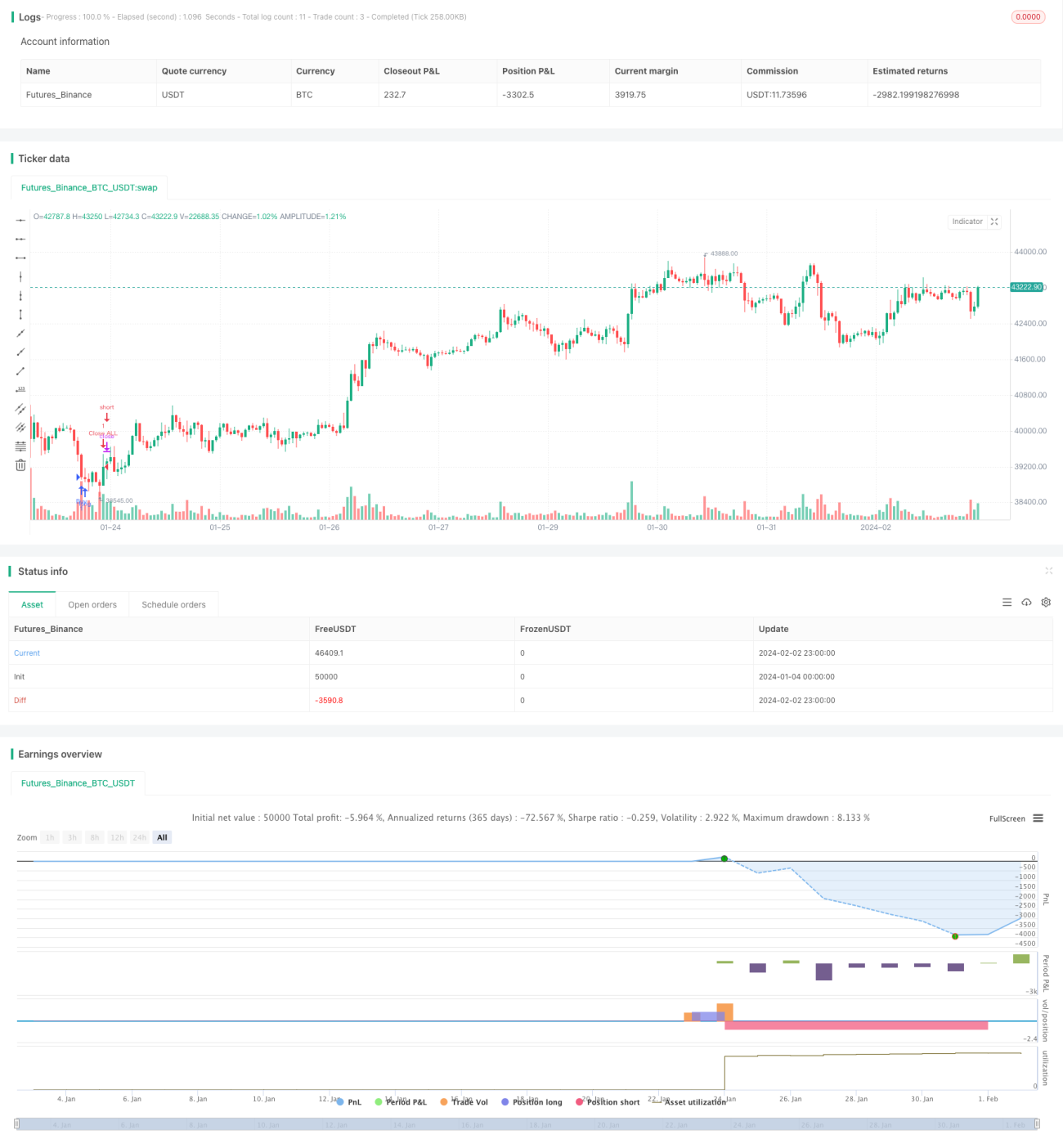

Chiến lược này sử dụng chỉ báo Bollinger Bands thích ứng hai chiều để xác định hướng xu hướng, kết hợp với lệnh thị trường để thực hiện trailing stop, đạt được giao dịch theo xu hướng hiệu quả cao.

Nguyên lý chiến lược

- Tính đường trung bình (Middle), dải trên (Upper) và dải dưới (Lower) của Bollinger Bands dựa trên một chu kỳ nhất định.

- Nếu giá phá vỡ dải trên thì thực hiện mua theo xu hướng (long trailing), phá vỡ dải dưới thì thực hiện bán theo xu hướng (short trailing).

- Sử dụng lệnh thị trường để vào lệnh nhanh chóng.

- Thiết lập vị trí stop loss và take profit để quản lý vị thế.

Phân tích ưu điểm

- Chỉ báo Bollinger Bands thích ứng nhạy cảm với biến động thị trường, có thể nhanh chóng nhận biết sự đảo chiều xu hướng.

- Sử dụng lệnh thị trường để vào lệnh nhanh, giảm rủi ro trượt giá.

- Tự động stop loss và take profit, kiểm soát rủi ro chặt chẽ, khóa lợi nhuận.

Phân tích rủi ro

- Bản thân Bollinger Bands có độ trễ nhất định, không thể tránh hoàn toàn các phá vỡ giả.

- Sử dụng lệnh thị trường không thể kiểm soát giá khớp lệnh.

- Cần thiết lập hợp lý các mức stop loss và take profit.

Hướng tối ưu hóa

- Điều chỉnh tham số của Bollinger Bands để tối ưu độ nhạy trong việc xác định xu hướng.

- Thêm các chỉ báo như khối lượng giao dịch hoặc MACD để lọc các phá vỡ giả.

- Tối ưu hóa việc thiết lập các mức stop loss và take profit.

Tổng kết

Chiến lược này tận dụng tối đa lợi thế của Bollinger Bands trong việc xác định hướng và sự thay đổi của xu hướng, kết hợp với lệnh thị trường vào/ra nhanh chóng để thực hiện giao dịch theo xu hướng hai chiều, đạt được lợi nhuận vượt trội trong khi kiểm soát rủi ro. Bằng cách tiếp tục tối ưu hóa tham số Bollinger Bands, thêm các chỉ báo lọc phụ trợ, điều chỉnh logic stop loss/take profit, có thể đạt được hiệu suất chiến lược tốt hơn. Chiến lược này có tư duy rõ ràng, dễ thực hiện, là một chiến lược giao dịch theo xu hướng hiệu quả và đáng tin cậy.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1