Chiến lược giao dịch đường xu hướng độ dốc động

Tổng quan

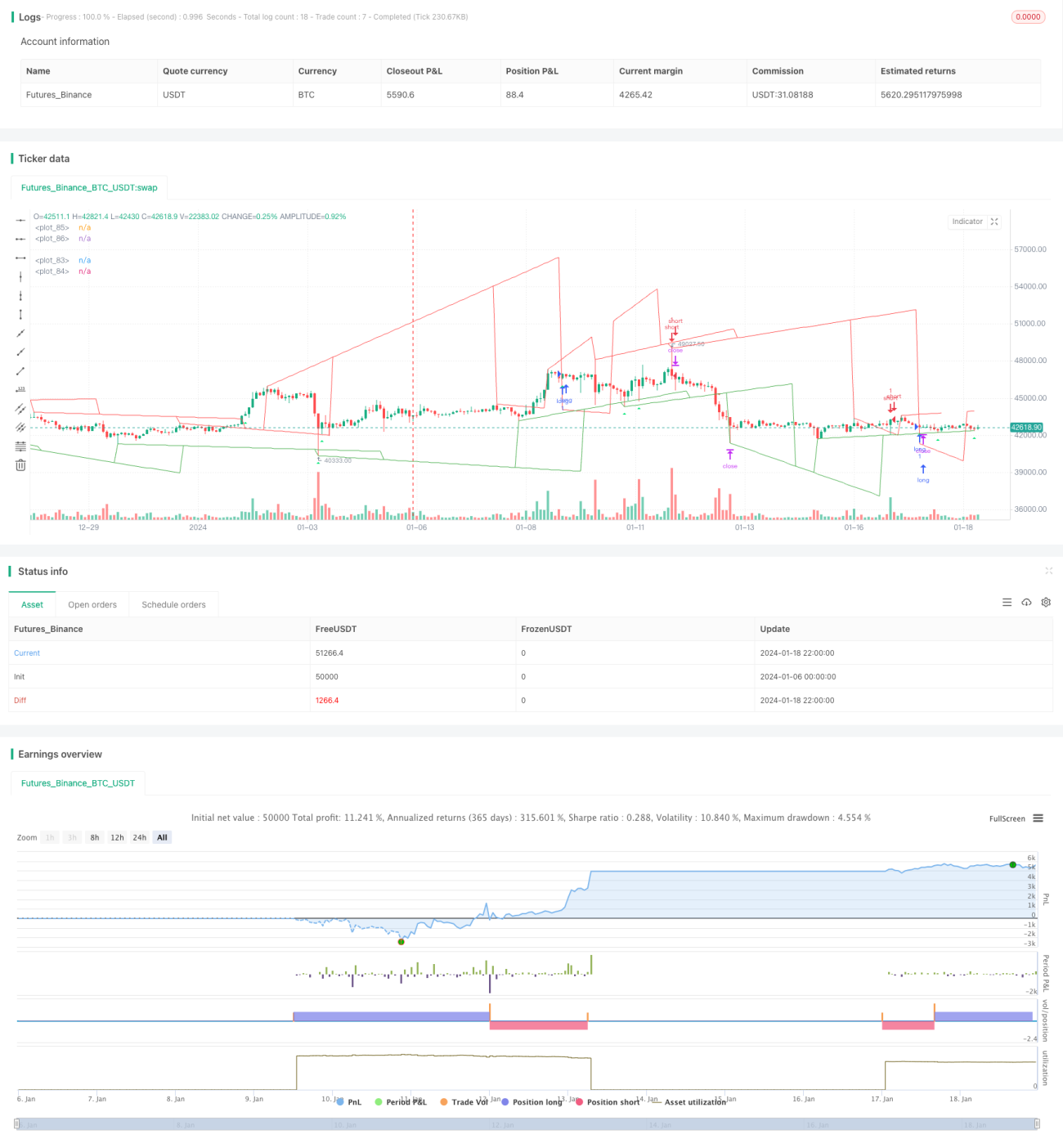

Ý tưởng cốt lõi của chiến lược này là sử dụng độ dốc động để đánh giá hướng xu hướng giá, kết hợp phá vỡ để tạo ra tín hiệu giao dịch. Cụ thể, nó sẽ theo dõi các đỉnh và đáy mới nhất của giá theo thời gian thực, tính toán độ dốc động dựa trên sự thay đổi giá trong các khung thời gian khác nhau, sau đó kết hợp với việc giá phá vỡ đường xu hướng để xác định tín hiệu mua/bán.

Nguyên lý chiến lược

Chiến lược này chủ yếu được chia thành các bước sau:

-

Xác định giá cao nhất và giá thấp nhất: Theo dõi giá cao nhất và thấp nhất trong một chu kỳ nhất định (ví dụ: 20 nến) để xác định xem có tạo đỉnh mới hoặc đáy mới hay không.

-

Tính toán độ dốc động: Ghi lại số thứ tự nến hình thành đỉnh mới hoặc đáy mới, tính toán độ dốc động từ điểm đỉnh/đáy mới đến một chu kỳ nhất định sau đó (ví dụ: 9 nến).

-

Vẽ đường xu hướng: Dựa trên độ dốc động, vẽ các đường xu hướng tăng và giảm.

-

Kéo dài và cập nhật đường xu hướng: Khi giá phá vỡ đường xu hướng, sẽ kéo dài và cập nhật đường xu hướng.

-

Tín hiệu giao dịch: Kết hợp việc giá phá vỡ đường xu hướng để xác định tín hiệu mua và bán.

Ưu điểm của chiến lược

Chiến lược này có những ưu điểm sau:

-

Đánh giá động hướng xu hướng, linh hoạt ứng phó với biến động thị trường.

-

Có thể kiểm soát cắt lỗ hợp lý, drawdown nhỏ.

-

Tín hiệu giao dịch phá vỡ rõ ràng, dễ thực hiện.

-

Có thể tùy chỉnh tham số, khả năng thích ứng cao.

-

Cấu trúc mã rõ ràng, dễ hiểu và dễ phát triển thêm.

Rủi ro và giải pháp

Chiến lược này cũng tồn tại một số rủi ro:

-

Khi xu hướng dao động, tín hiệu mua/bán có thể sai, khuyến nghị thêm bộ lọc điều kiện.

-

Tín hiệu phá vỡ giả có thể nhiều, có thể điều chỉnh tham số hoặc thêm bộ lọc phù hợp.

-

Rủi ro cắt lỗ khi thị trường biến động mạnh, có thể tăng biên độ cắt lỗ.

-

Không gian tối ưu hạn chế, lợi nhuận bị giới hạn, phù hợp giao dịch ngắn hạn.

Hướng tối ưu hóa

Chiến lược này có thể tối ưu ở các điểm sau:

-

Thêm nhiều chỉ báo kỹ thuật để đánh giá và lọc tín hiệu.

-

Tối ưu hóa tổ hợp tham số để tìm tham số tốt nhất.

-

Thử cải thiện chiến lược cắt lỗ để giảm rủi ro.

-

Bổ sung chức năng tự động điều chỉnh biên độ vào lệnh.

-

Thử kết hợp với các chiến lược khác để khám phá thêm cơ hội.

Kết luận

Nhìn chung, chiến lược này là một chiến lược ngắn hạn hiệu quả dựa trên độ dốc động để đánh giá xu hướng và giao dịch phá vỡ. Nó có độ chính xác cao, rủi ro có thể kiểm soát, thích hợp để nắm bắt các cơ hội ngắn hạn trên thị trường. Bằng cách tối ưu hóa tham số và thêm bộ lọc điều kiện, có thể nâng cao tỷ lệ thắng và mức lợi nhuận của chiến lược.

/*backtest

start: 2024-01-06 00:00:00

end: 2024-01-19 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © pune3tghai

//Originally posted by matsu_bitmex- 1