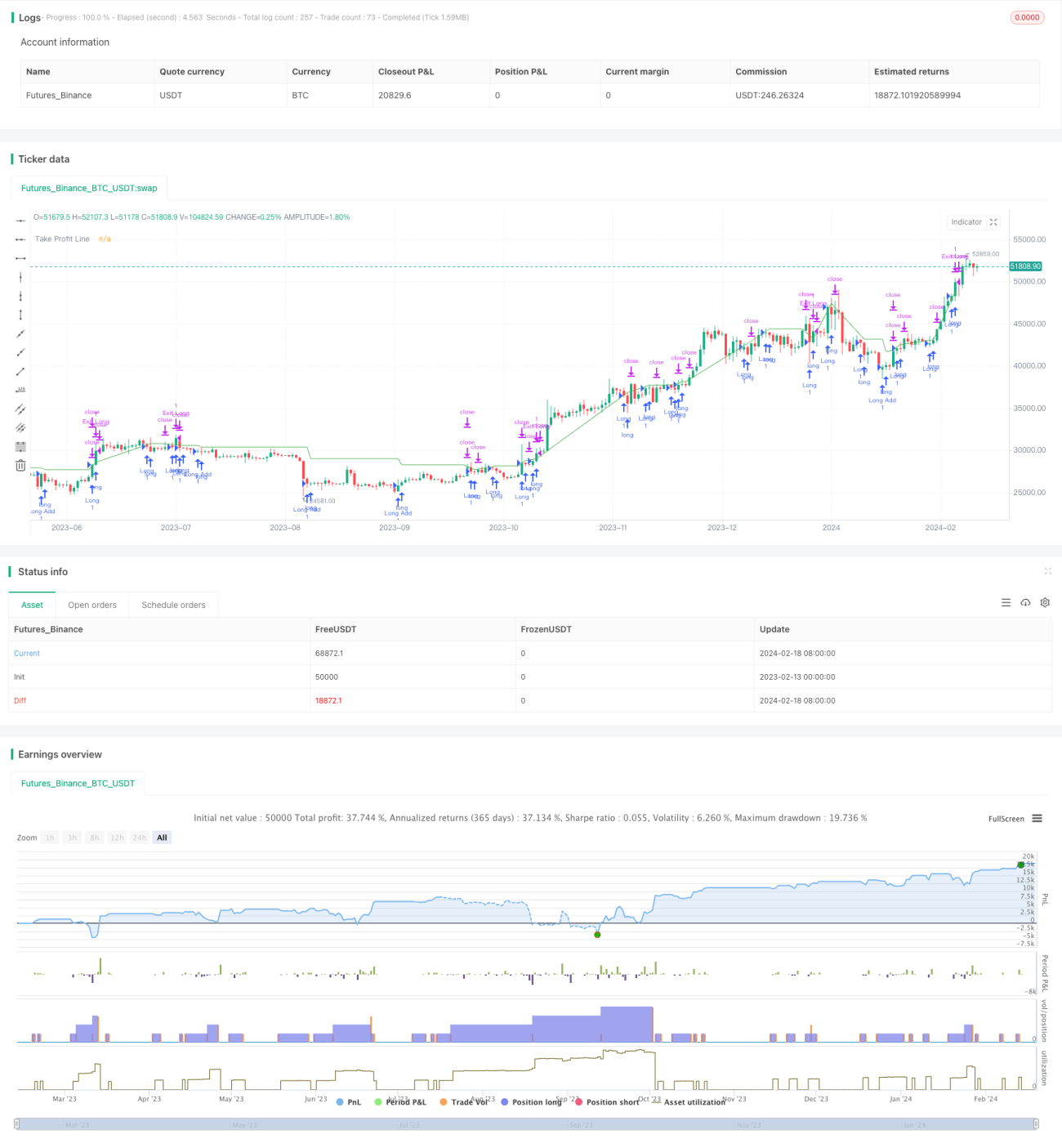

Chiến lược giao dịch định lượng dựa trên đa yếu tố

Tổng quan

Chiến lược này kết hợp nhiều chỉ báo kỹ thuật như RSI, MACD, OBV, CCI, CMF, MFI và VWMACD để phát hiện sự phân kỳ giữa giá và khối lượng, nhằm xác định cơ hội vào lệnh tiềm năng. Chiến lược cũng kết hợp chỉ báo phát hiện sự sụt giảm (dip) do người dùng xác định, phát tín hiệu giao dịch khi thỏa mãn điều kiện biến động cao và độ sâu hoặc chỉ báo VFI. Chiến lược chỉ thực hiện lệnh mua, sử dụng trailing stop và xây dựng vị thế bằng cách tăng dần (gấp thếp).

Nguyên lý chiến lược

- Tính toán các chỉ báo RSI, MACD, OBV, CCI, CMF, MFI và VWMACD, đồng thời phát hiện sự phân kỳ giữa các chỉ báo và giá lịch sử thông qua phương pháp hồi quy tuyến tính thích ứng. Khi chỉ báo tạo đáy mới nhưng giá không đi theo để tạo đáy mới, tín hiệu mua được phát ra.

- Dựa trên ngưỡng biến động và ngưỡng phần trăm độ sâu do người dùng nhập vào, kết hợp với bộ lọc chỉ báo VFI, phát tín hiệu trên các nến đáp ứng điều kiện biến động cao và kiểm tra độ sâu.

- Sau khi mua ban đầu, nếu giá phá vỡ một tỷ lệ nhất định (có thể cấu hình) so với mức giá mua cuối cùng, sẽ thực hiện mua thêm một lần nữa để tăng vị thế.

- Sử dụng trailing stop, đóng vị thế khi đạt tỷ lệ chốt lời đã cấu hình.

Phân tích ưu điểm

- Kết hợp đa yếu tố, sử dụng tổng hợp các chỉ báo giá và khối lượng, giúp tăng độ tin cậy của tín hiệu.

- Phương pháp hồi quy tuyến tính thích ứng phát hiện phân kỳ, loại bỏ tính chủ quan trong phán đoán của con người.

- Kết hợp với chỉ báo biến động và độ sâu/VFI, giúp phát hiện các cơ hội đảo chiều.

- Cơ chế tăng vị thế nhiều lần cho phép tận dụng sự điều chỉnh giá, và trailing stop chốt lời có lợi cho việc khóa lợi nhuận.

Phân tích rủi ro

- Việc kết hợp nhiều yếu tố để phán đoán khá phức tạp, hiệu quả của việc tối ưu hóa tham số và nhận diện phân kỳ có thể ảnh hưởng đến hiệu suất thực tế.

- Rủi ro cao khi chỉ nắm giữ vị thế một chiều, nếu phán đoán sai có thể gây ra tổn thất lớn.

- Trong chế độ tăng vị thế liên tục, thua lỗ cũng sẽ bị khuếch đại, cần kiểm soát vị thế một cách thận trọng.

- Cần chú ý đến ảnh hưởng của phí giao dịch đến lợi nhuận thực tế.

Hướng tối ưu hóa

- Kiểm tra hiệu quả của các tổ hợp tham số và chỉ báo khác nhau để lựa chọn cấu hình tối ưu.

- Thêm chiến lược cắt lỗ, kiểm soát thua lỗ cho từng lệnh và tổng thua lỗ tối đa.

- Cân nhắc các cơ hội giao dịch hai chiều để phân tán rủi ro.

- Kết hợp các phương pháp học máy để tự động tối ưu hóa tham số.

Tổng kết

Chiến lược này tổng hợp nhiều chỉ báo kỹ thuật để nhận diện thời điểm vào lệnh, đồng thời sử dụng các điều kiện do người dùng xác định và chỉ báo VFI để lọc các tín hiệu sai. Chiến lược tận dụng sự điều chỉnh giá để liên tục tăng vị thế mua đuổi theo xu hướng, có lợi trong việc nắm bắt cơ hội trong xu hướng. Tuy nhiên, nó cũng phải đối mặt với rủi ro phán đoán sai và nắm giữ vị thế một chiều, cần tối ưu hóa phù hợp các tham số chỉ báo, chiến lược cắt lỗ, v.v... để giảm rủi ro và tăng không gian lợi nhuận.

- 1