Chiến lược đột phá giá với stop loss động cho vị thế mua và bộ lọc theo mùa

Tổng quan

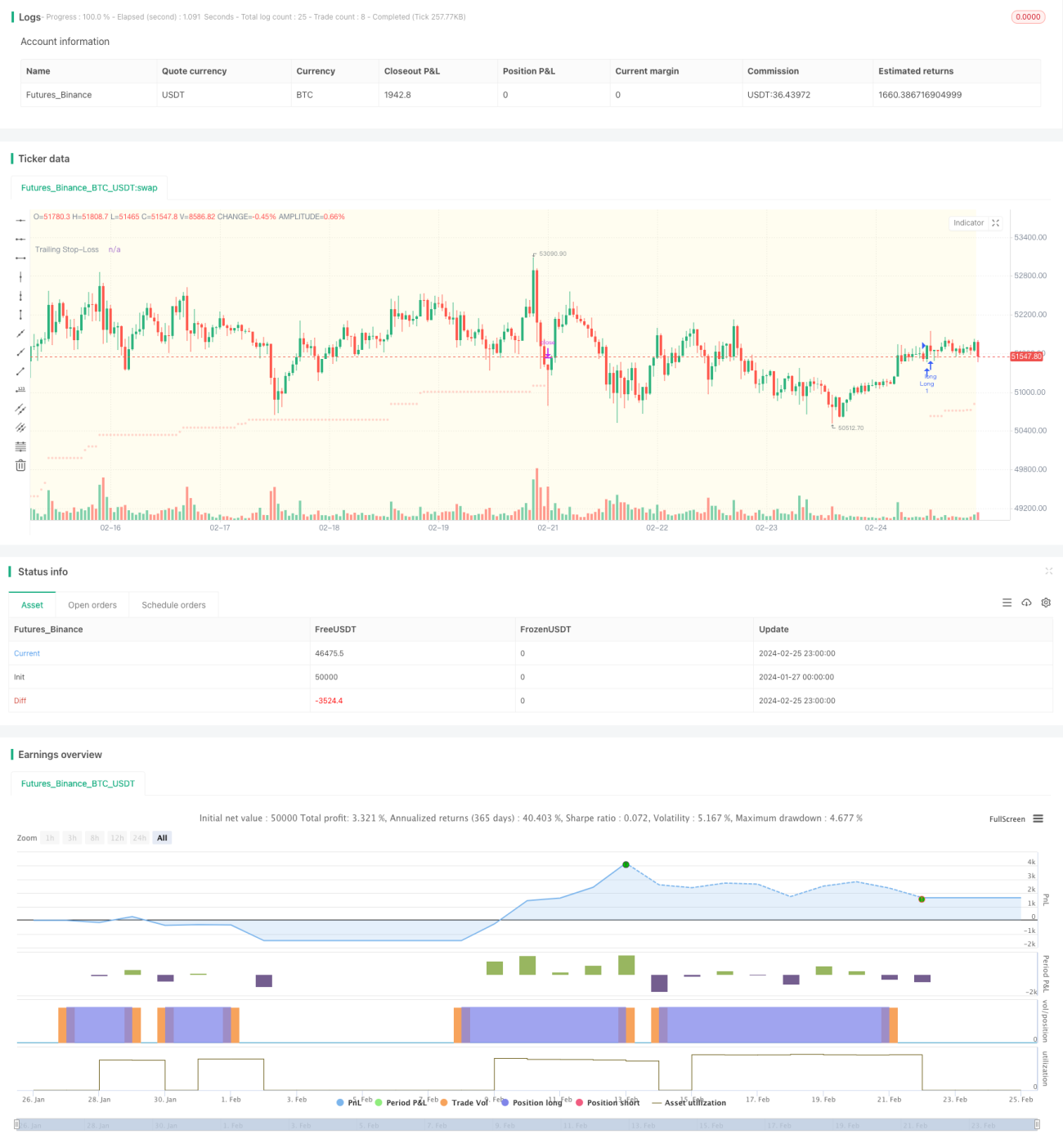

Chiến lược này được thiết kế dựa trên Chỉ số chuyển động động (DMI) cho một chiến lược dài hạn chỉ mua, đồng thời kết hợp với dải biên độ thực trung bình (ATR) để thực hiện lệnh cắt lỗ trailing, nhằm kiểm soát rủi ro thua lỗ. Để tối ưu hóa hơn nữa, chiến lược còn tích hợp các bộ lọc về thời gian giao dịch và tính mùa vụ của chỉ số S&P 500, mang lại những lợi thế nhất định.

Nguyên lý chiến lược

-

Chiến lược chỉ mở vị thế vào các ngày giao dịch được chỉ định (Thứ Hai đến Thứ Sáu) và trong khung giờ giao dịch (mặc định là 9:30-20:30 theo giờ địa phương).

-

Khi ADX lớn hơn 27, cho thấy thị trường đang trong trạng thái xu hướng giá. Lúc này nếu đường +DI cắt lên trên đường -DI, sẽ phát ra tín hiệu mua.

-

Sau khi mở vị thế, đặt mức dừng lỗ bằng 5,5 lần ATR, và đường dừng lỗ sẽ dịch chuyển lên theo khi giá tăng, đảm bảo chốt lời.

-

Tùy chọn áp dụng quy tắc mùa vụ của chỉ số S&P 500, chỉ mở vị thế trong những giai đoạn có diễn biến lịch sử tốt hơn.

Phân tích ưu điểm

-

Kết hợp chỉ báo xu hướng và cơ chế dừng lỗ, có thể theo dõi xu hướng hiệu quả và kiểm soát thua lỗ của từng vị thế.

-

Sử dụng các bộ lọc thời gian giao dịch và tính mùa vụ có thể tránh được các giai đoạn biến động bất thường của thị trường, giảm tỷ lệ tín hiệu sai.

-

DMI và ATR đều là các chỉ báo kỹ thuật đã trưởng thành, có tham số linh hoạt, phù hợp để tối ưu hóa định lượng.

Phân tích rủi ro

-

Tham số DMI và ATR cài đặt không phù hợp có thể dẫn đến quá nhiều hoặc quá ít tín hiệu. Cần điều chỉnh tham số và kiểm tra.

-

Mức dừng lỗ quá rộng có thể gây ra các lệnh dừng lỗ không cần thiết. Quá hẹp có thể không kiểm soát được thua lỗ hiệu quả.

-

Các quy tắc thời gian giao dịch và mùa vụ có thể lọc bỏ một số cơ hội lợi nhuận. Cần đánh giá hiệu quả lọc.

Hướng tối ưu hóa

-

Có thể xem xét kết hợp các chỉ báo khác như MACD, Bollinger Bands để thiết kế quy tắc vào và ra lệnh.

-

Có thể thử nghiệm các phương pháp dừng lỗ với bội số ATR khác nhau, hoặc xem xét điều chỉnh biên độ dừng lỗ động.

-

Có thể thử nghiệm điều chỉnh khung giờ giao dịch hoặc tối ưu hóa thời gian bắt đầu/kết thúc giao dịch mùa vụ.

-

Có thể thử áp dụng các phương pháp học máy để tự động tối ưu hóa tham số.

Tổng kết

Chiến lược này tích hợp công nghệ phân tích xu hướng và quản lý rủi ro, ở một mức độ nhất định đã khắc phục được vấn đề dao động mạnh của chiến lược bám xu hướng. Đồng thời bổ sung bộ lọc thời gian giao dịch và tính mùa vụ có thể giảm tín hiệu sai. Thông qua tối ưu hóa tham số và mở rộng chức năng, chiến lược này có thể đạt được lợi nhuận ổn định tốt hơn.

/*backtest

start: 2024-01-27 00:00:00

end: 2024-02-26 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="DMI Strategy with ADX and ATR-based Trailing SL (Long Only) and Seasonality", shorttitle="MBV-SP500-CLIMBER", overlay=true)

// Eingabeparameter für Long-Positionen- 1