গতিশীল প্রশস্ততা ক্যাপচার RSI-বলিঞ্জার ব্যান্ড কৌশল

সারসংক্ষেপ

ডায়নামিক ভোলাটিলিটি ক্যাপচার RSI-বলিঞ্জার ব্যান্ড কৌশলটি একটি ট্রেডিং কৌশল যা বলিঞ্জার ব্যান্ড (BB), রিলেটিভ স্ট্রেংথ ইনডেক্স (RSI) এবং সিম্পল মুভিং এভারেজ (SMA) -এর ধারণাগুলিকে একীভূত করে। এই কৌশলটির বিশেষত্ব হলো এটি ক্লোজিং প্রাইসের উপর ভিত্তি করে উপরের ও নিচের ব্যান্ডের মধ্যে একটি গতিশীল স্তর গণনা করে। এই অনন্য বৈশিষ্ট্যটি কৌশলটিকে বাজারের অস্থিরতা এবং মূল্য পরিবর্তনের সাথে খাপ খাইয়ে নিতে সক্ষম করে।

ক্রিপ্টোকারেন্সি এবং স্টক মার্কেটগুলি অত্যন্ত অস্থির, তাই বলিঞ্জার ব্যান্ড কৌশল ব্যবহারের জন্য এগুলি অত্যন্ত উপযুক্ত। RSI এই প্রায়শই স্পেকুলেটিভ বাজারে ওভারবট/ওভারসোল্ড পরিস্থিতি চিহ্নিত করতে সাহায্য করে।

কৌশলের নীতি

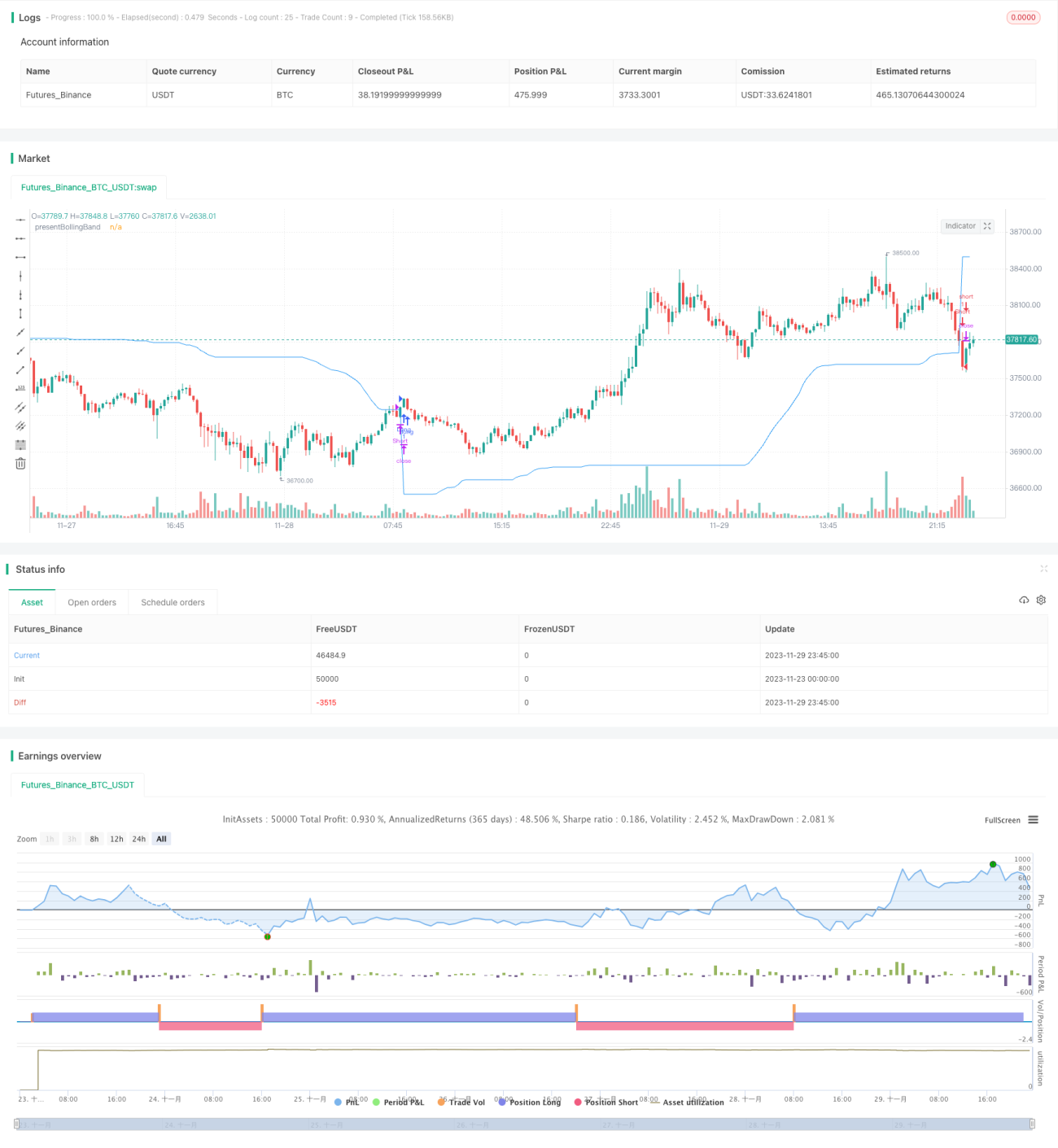

ডায়নামিক বলিঞ্জার ব্যান্ড: এই কৌশলটি প্রথমে ব্যবহারকারীর নির্ধারিত দৈর্ঘ্য এবং গুণক অনুসারে উপরের ও নিচের বলিঞ্জার ব্যান্ড গণনা করে। তারপর বলিঞ্জার ব্যান্ড এবং ক্লোজিং প্রাইস একত্রিত করে presentBollingBand-এর মান গতিশীলভাবে সামঞ্জস্য করে। শেষে, যখন মূল্য presentBollingBand-কে অতিক্রম করে তখন লং সিগন্যাল তৈরি হয় এবং যখন মূল্য presentBollingBand-কে অতিক্রম করে তখন শর্ট সিগন্যাল তৈরি হয়।

RSI: যদি ব্যবহারকারী সিগন্যাল তৈরি করতে RSI ব্যবহার করতে চান, তাহলে কৌশলটি RSI এবং এর SMA-ও গণনা করে এবং অতিরিক্ত লং ও শর্ট সিগন্যাল তৈরি করতে সেগুলি ব্যবহার করে। শুধুমাত্র যখন "সিগন্যাল তৈরি করতে RSI ব্যবহার করুন" অপশনটি true-তে সেট করা থাকে, তখনই RSI-ভিত্তিক সিগন্যাল ব্যবহার করা হয়।

এরপর কৌশলটি নির্বাচিত ট্রেডিং দিক পরীক্ষা করে এবং সেই অনুযায়ী লং বা শর্ট পজিশনে প্রবেশ করে। যদি ট্রেডিং দিক "দ্বিমুখী" এ সেট করা থাকে, তাহলে কৌশলটি একইসাথে লং ও শর্ট উভয় পজিশনেই প্রবেশ করতে পারে।

সবশেষে, যখন ক্লোজিং প্রাইস presentBollingBand-কে অতিক্রম করে তখন লং পজিশন বন্ধ হয়; এবং যখন ক্লোজিং প্রাইস presentBollingBand-কে অতিক্রম করে তখন শর্ট পজিশন বন্ধ হয়।

সুবিধা বিশ্লেষণ

এই কৌশলটি বলিঞ্জার ব্যান্ড, RSI এবং SMA সূচকের সুবিধাগুলিকে একত্রিত করে, যা বাজারের অস্থিরতার সাথে খাপ খাইয়ে নিতে, গতিশীলভাবে অস্থিরতা ধরতে এবং ওভারবট/ওভারসোল্ড পরিস্থিতিতে ট্রেডিং সিগন্যাল তৈরি করতে সক্ষম।

RSI সূচকটি বলিঞ্জার ব্যান্ডের ট্রেডিং সিগন্যালকে পরিপূরক করে, যা সাইডওয়ে মার্কেটে ভুল এন্ট্রি এড়াতে সাহায্য করে। শুধুমাত্র লং, শুধুমাত্র শর্ট বা দ্বিমুখী ট্রেডিং নির্বাচনের অনুমতি দেয়, যা বিভিন্ন বাজার অবস্থার সাথে খাপ খাইয়ে নেয়।

প্যারামিটারগুলি কাস্টমাইজ করা যায়, যা ব্যক্তিগত ঝুঁকি সহনশীলতা অনুযায়ী সামঞ্জস্য করতে সক্ষম।

ঝুঁকি বিশ্লেষণ

এই কৌশলটি টেকনিক্যাল সূচকের উপর নির্ভর করে, যা মৌলিক কারণে সৃষ্ট বড় পরিবর্তন মোকাবেলা করতে পারে না।

বলিঞ্জার ব্যান্ডের প্যারামিটারগুলি সঠিকভাবে সেট না করলে খুব ঘন ঘন বা খুব কম ট্রেডিং সিগন্যাল তৈরি হতে পারে।

দ্বিমুখী ট্রেডিংয়ের ঝুঁকি বেশি থাকে এবং বিপরীতমুখী শর্ট করার ক্ষেত্রে লোকসানের বিষয়ে সতর্ক থাকতে হবে।

ঝুঁকি নিয়ন্ত্রণের জন্য স্টপ লস ব্যবহার করার পরামর্শ দেওয়া হচ্ছে।

অপটিমাইজেশনের দিকনির্দেশনা

- অন্যান্য সূচক যেমন MACD-এর সাথে সিগন্যাল ফিল্টার করা।

- স্টপ লস কৌশল যুক্ত করা।

- বলিঞ্জার ব্যান্ড এবং RSI-এর প্যারামিটার অপটিমাইজ করা।

- বিভিন্ন ট্রেডিং পণ্য এবং সময়কাল অনুসারে প্যারামিটার সামঞ্জস্য করা।

- রিয়েল ট্রেডিং অপটিমাইজেশন বিবেচনা করা এবং প্রকৃত পরিস্থিতির সাথে খাপ খাইয়ে প্যারামিটার সামঞ্জস্য করা।

উপসংহার

ডায়নামিক ভোলাটিলিটি ক্যাপচার RSI-বলিঞ্জার ব্যান্ড কৌশলটি একটি টেকনিক্যাল সূচক-চালিত কৌশল, যা বলিঞ্জার ব্যান্ড, RSI এবং SMA সূচকের সুবিধাগুলিকে একত্রিত করে এবং বলিঞ্জার ব্যান্ডকে গতিশীলভাবে সামঞ্জস্য করে বাজারের অস্থিরতা ধরে। এই কৌশলটিতে কাস্টমাইজেশন এবং অপটিমাইজেশনের যথেষ্ট সুযোগ রয়েছে, তবে এটি মৌলিক পরিবর্তনের পূর্বাভাস দিতে পারে না। রিয়েল ট্রেডিংয়ে ফলাফল যাচাই করার পরামর্শ দেওয়া হচ্ছে এবং প্রয়োজনে প্যারামিটার সামঞ্জস্য করা বা অন্যান্য সূচক যুক্ত করে ঝুঁকি কমানোর জন্য ব্যবহার করা।

- 1