K-লাইন ভিত্তিক বুলিশ ব্রেকআউট কৌশল

সারসংক্ষেপ

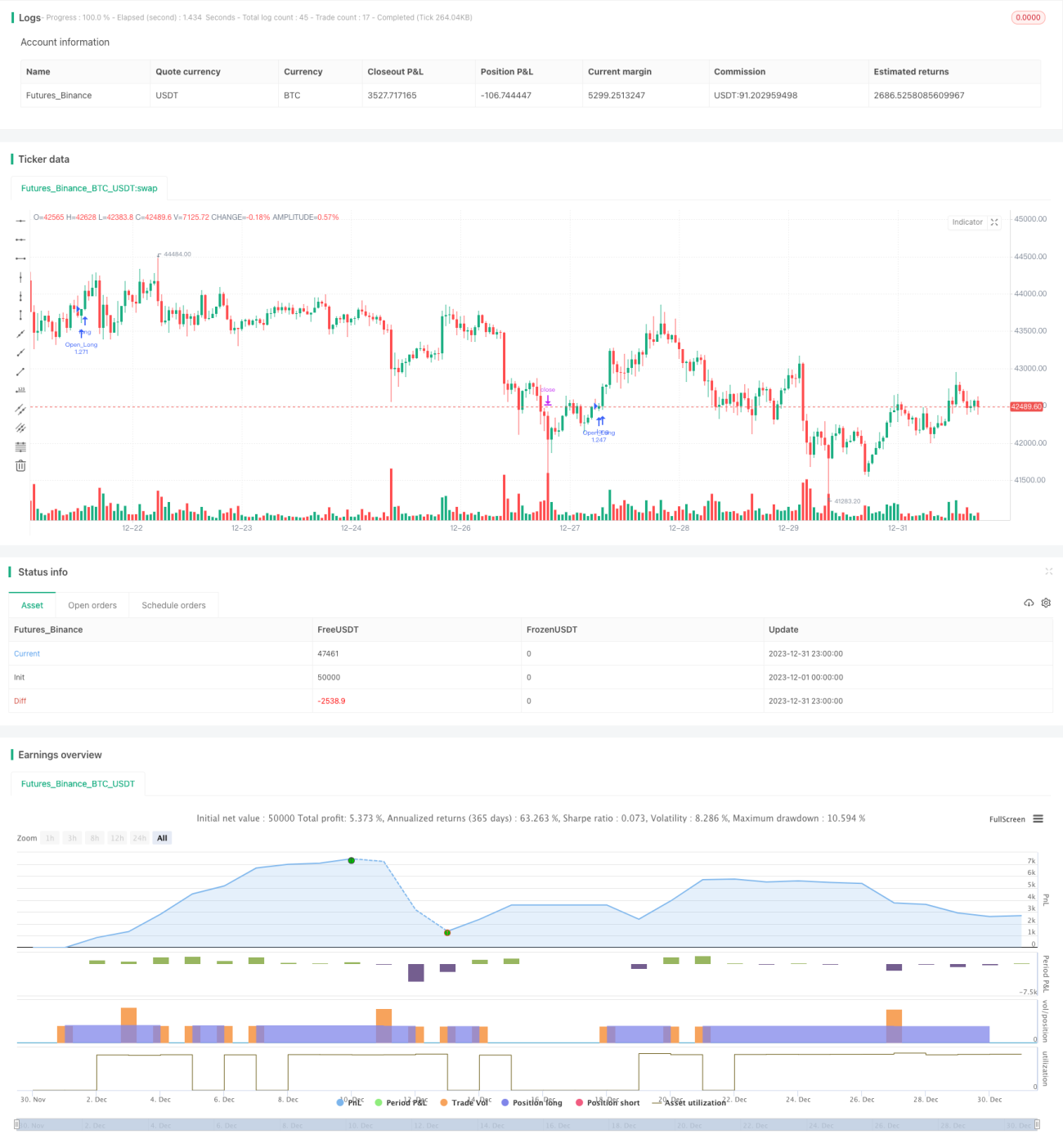

এই কৌশলটি সহজ ক্যান্ডেলস্টিক প্যাটার্ন শনাক্তকরণ নিয়ম নির্ধারণের মাধ্যমে টেসলার ৪-ঘন্টার চার্টে লং পজিশন ব্রেকআউট ট্রেডিং বাস্তবায়ন করে। কৌশলটির বাস্তবায়ন সহজ, যুক্তি স্পষ্ট এবং বোঝা সহজ।

কৌশলের মূলনীতি

কৌশলের মূল সিদ্ধান্ত গ্রহণের যুক্তি নিম্নলিখিত ৪টি ক্যান্ডেলস্টিক প্যাটার্ন নিয়মের উপর ভিত্তি করে:

- বর্তমান ক্যান্ডেলের সর্বনিম্ন দাম উদ্বোধনী মূল্যের চেয়ে কম।

- বর্তমান ক্যান্ডেলের সর্বনিম্ন দাম আগের ক্যান্ডেলের সর্বনিম্ন দামের চেয়ে কম।

- বর্তমান ক্যান্ডেলের সমাপনী মূল্য উদ্বোধনী মূল্যের চেয়ে বেশি।

- বর্তমান ক্যান্ডেলের সমাপনী মূল্য আগের ক্যান্ডেলের উদ্বোধনী মূল্য এবং সমাপনী মূল্যের চেয়ে বেশি।

যখন একই সাথে উপরের ৪টি নিয়ম পূর্ণ হয়, তখন লং পজিশন খোলা হবে।

এছাড়াও, কৌশলটিতে স্টপ-লস এবং টেক-প্রফিট স্তর নির্ধারণ করা আছে; যখন দাম এই স্তর স্পর্শ করে, তখন পজিশন বন্ধ করা হবে।

সুবিধা বিশ্লেষণ

কৌশলটির নিম্নলিখিত কিছু সুবিধা রয়েছে:

- ব্যবহৃত ক্যান্ডেলস্টিক শনাক্তকরণ নিয়মগুলি খুব সহজ এবং সরাসরি, বোঝা এবং প্রয়োগ করা সহজ।

- সম্পূর্ণরূপে দামের কাঠামোর উপর ভিত্তি করে, অতিরিক্ত জটিল প্রযুক্তিগত সূচক ব্যবহার না করায় ব্যাকটেস্টিং ফলাফল সরাসরি পাওয়া যায়।

- বাস্তবায়নের কোড আকার ছোট, কার্যকারিতার দক্ষতা বেশি এবং সহজেই অপ্টিমাইজ ও উন্নত করা যায়।

- প্যারামিটার সমন্বয়ের মাধ্যমে স্বাধীনভাবে স্টপ-লস ও টেক-প্রফিট শর্ত নির্ধারণ করে ঝুঁকি নিয়ন্ত্রণ করা যায়।

ঝুঁকি বিশ্লেষণ

যে ঝুঁকিগুলি লক্ষ্য করা প্রয়োজন:

- নির্দিষ্ট সংখ্যক কন্ট্রাক্ট ব্যবহার করে পজিশন খোলা, পজিশন ম্যানেজমেন্ট বিবেচনায় না নেওয়ায় অতিরিক্ত ট্রেডিংয়ের ঝুঁকি থাকতে পারে।

- কোনো ফিল্টার না থাকায় অস্থির বাজারে অকার্যকর ট্রেডের সংখ্যা বেশি হতে পারে।

- পর্যাপ্ত ব্যাকটেস্টিং ডেটা না থাকায় কৌশলের কার্যকারিতা মূল্যায়নে পক্ষপাতিত্ব দেখা দিতে পারে।

নিম্নলিখিত পদ্ধতিতে ঝুঁকি হ্রাস করা যেতে পারে:

- পজিশন ম্যানেজমেন্ট মডিউল যুক্ত করে মূলধনের আকারের ভিত্তিতে ট্রেডের আকার গতিশীলভাবে নির্ধারণ করা।

- ট্রেড ফিল্টারিং শর্ত যোগ করে অস্থির বাজারে অকার্যকর পজিশন খোলা এড়ানো।

- আরও ঐতিহাসিক ডেটা সংগ্রহ করে ব্যাকটেস্টিংয়ের সময়কাল বাড়ানো এবং ফলাফলের নির্ভরযোগ্যতা উন্নত করা।

অপ্টিমাইজেশন সম্ভাবনা

এই কৌশলটির অপ্টিমাইজেশনের সম্ভাব্য দিকগুলি:

- পজিশন ম্যানেজমেন্ট মডিউল যোগ করে মূলধনের ব্যবহারের অনুপাতের ভিত্তিতে ট্রেডের আকার নির্ধারণ করা।

- স্টপ-লস ও টেক-প্রফিট ট্র্যাকিং মেকানিজম ডিজাইন করে নমনীয় এক্সিট নিশ্চিত করা।

- ট্রেড ফিল্টারিং মডিউল যোগ করে অকার্যকর ট্রেড এড়ানো।

- মেশিন লার্নিং পদ্ধতি ব্যবহার করে প্যারামিটার স্বয়ংক্রিয়ভাবে অপ্টিমাইজ করা।

- একাধিক পণ্যের মধ্যে আর্বিট্রেজ ট্রেডিং সমর্থন করা।

সারসংক্ষেপ

এই কৌশলটি সহজ ক্যান্ডেলস্টিক প্যাটার্ন শনাক্তকরণ নিয়মের মাধ্যমে লং ব্রেকআউট ট্রেডিং বাস্তবায়ন করে। যদিও উন্নতির কিছু সুযোগ রয়েছে, তবে সরলতা এবং স্পষ্টতার দৃষ্টিকোণ থেকে এটি নতুন ট্রেডারদের জন্য বোঝা এবং ব্যবহার করার জন্য একটি অত্যন্ত উপযুক্ত লং কৌশল। ক্রমাগত অপ্টিমাইজেশনের মাধ্যমে কৌশলটির কার্যকারিতা আরও উন্নত করা যেতে পারে।

- 1