Multi-Trend-Strategie

Überblick

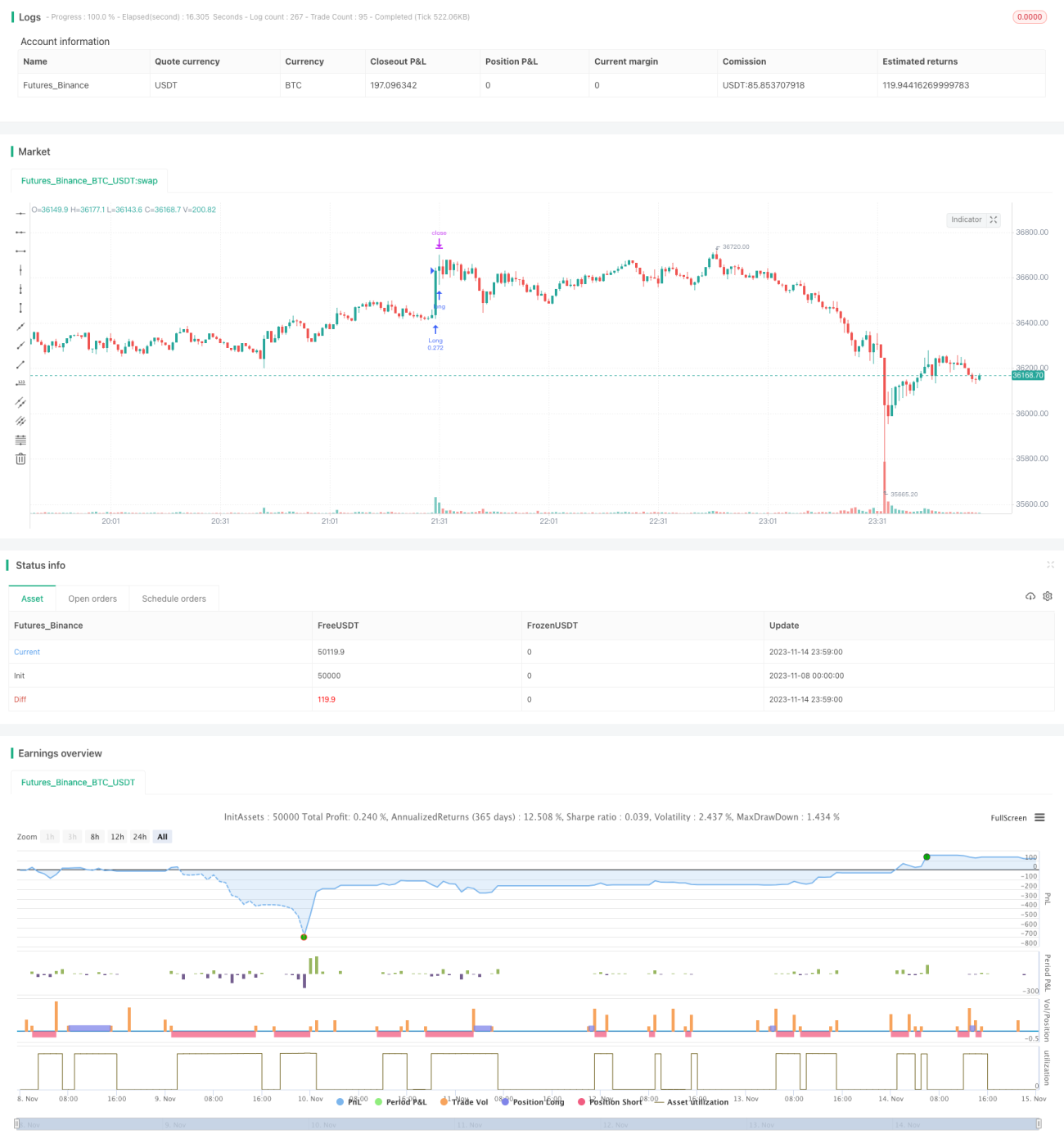

Diese Strategie kombiniert mehrere Indikatoren, um die Trendrichtung zu identifizieren. Sie verfolgt einen Trendfolge-Ansatz, um mittel- bis kurzfristige Trendchancen zu nutzen. Die Strategie ist speziell für das Verfolgen von Trends konzipiert und zielt darauf ab, die Trefferquote zu erhöhen und die Verluste zu reduzieren.

Strategieprinzip

- Verwendung des WVAP-Indikators zur Bestimmung des Preisverhältnisses;

- RSI-Indikator zur Beurteilung des bullischen/bärischen Momentums;

- QQE-Indikator zur Erkennung von Preisausbrüchen;

- ADX-Indikator zur Bewertung der Trendstärke;

- Coral Trend Indicator zur Bestimmung des fundamentalen Trends;

- LSMA-Indikator als Hilfsmittel zur Trendbeurteilung;

- Kombination der Signale mehrerer Indikatoren zur Auslösung von Handelssignalen.

Die Strategie stützt sich hauptsächlich auf mehrere Indikatoren wie RSI, QQE und ADX, um Trendrichtung und -stärke zu beurteilen, wobei die Kurve des Coral Trend Indicators als Maßstab für den fundamentalen Trend dient. Wenn Indikatoren wie der RSI ein Kaufsignal geben und der Coral Trend Indicator ebenfalls eine ansteigende Kurve zeigt, ist die Wahrscheinlichkeit eines Aufwärtstrends hoch, und die Strategie wird einen Kauf auslösen. Indikatoren wie der WVAP dienen hauptsächlich dazu, die Angemessenheit des Preisniveaus zu beurteilen und Käufe auf Höchstständen zu vermeiden.

Vorteile der Strategie

- Mehrere Indikatoren in Kombination erhöhen die Genauigkeit der Beurteilung;

- Fokus auf Trendfolge erhöht die Wahrscheinlichkeit von Gewinnen;

- Verwendung eines Ausbruchsansatzes filtert Trading-Range-Märkte heraus;

- Einbeziehung fundamentaler Indikatoren vermeidet Handel gegen den Trend;

- Angemessene Handelszeiten und Positionsgrößen senken das Risiko;

- Klare Strategielogik, leicht verständlich und optimierbar.

Der größte Vorteil dieser Strategie ist die Kombination mehrerer Indikatoren, die die Wahrscheinlichkeit von Fehlentscheidungen eines einzelnen Indikators verringert und die Beurteilungsgenauigkeit erhöht. Gleichzeitig wird durch die Betonung von Trendfolge und Ausbruchsansätzen die Auswahl zuverlässiger mittel- bis kurzfristiger Chancen unterstützt. Darüber hinaus hilft die Einbeziehung fundamentaler Indikatoren, gegen den Trend gerichtete Aktionen zu vermeiden. Diese Gestaltungsmerkmale verbessern die Stabilität und Gewinnwahrscheinlichkeit der Strategie.

Risiken der Strategie

- Die bullisch/bärische Beurteilung kann zeitlich verzögert sein, sodass optimale Einstiegspunkte verpasst werden könnten;

- Das Drawdown-Management ist nicht vollständig ausgearbeitet, es besteht ein erhebliches Drawdown-Risiko;

- Bei fundamentalen Wendepunkten könnte die Strategie Signale übersehen;

- Die Transaktionskosten werden nicht berücksichtigt, sodass die tatsächlichen Erträge unter Abwärtsrisiken leiden könnten.

Das größte Risiko der Strategie liegt in der möglichen zeitlichen Verzögerung durch die Kombination mehrerer Indikatoren, die zum Verpassen des optimalen Einstiegszeitpunkts und damit zu geringeren Gewinnspannen führen kann. Zudem ist die Drawdown-Kontrolle nicht ideal, was ein beträchtliches Drawdown-Risiko birgt. Wenn sich die fundamentalen Marktbedingungen ändern, bevor die Indikatoren dies widerspiegeln, können ebenfalls Verluste entstehen. In der praktischen Anwendung haben auch die Transaktionskosten einen gewissen Einfluss auf die Rendite.

Optimierungsmöglichkeiten

- Einführung einer Stop-Loss-Strategie zur Verbesserung der Drawdown-Kontrolle;

- Optimierung der Parametereinstellungen zur Verkürzung der Indikatorverzögerungen;

- Erweiterung der Anwendung fundamentaler Indikatoren zur Steigerung der Genauigkeit;

- Integration maschineller Lernalgorithmen zur dynamischen Parameteroptimierung.

Bei der Optimierung dieser Strategie sollte der Schwerpunkt auf der Drawdown-Kontrolle liegen. Es könnte eine nachlaufende Stop-Loss-Strategie (Trailing Stop) eingeführt werden, um Gewinne zu sichern und Drawdowns zu reduzieren. Gleichzeitig können die Parametereinstellungen optimiert werden, um die Indikatorverzögerungen zu verkürzen und die Empfindlichkeit der Strategie gegenüber Marktveränderungen zu erhöhen. Darüber hinaus können weitere fundamentale Beurteilungsindikatoren hinzugefügt werden, um die Genauigkeit zu verbessern. Wenn es gelingt, maschinelle Lernmethoden zur dynamischen Parameteroptimierung einzusetzen, könnte dies die Stabilität der Strategie erheblich steigern.

Zusammenfassung

Diese Strategie kombiniert mehrere Indikatoren zur Bestimmung der Trendrichtung und ist nach dem Trendfolgeprinzip konzipiert, um die Beurteilungsgenauigkeit zu erhöhen und die Gewinnwahrscheinlichkeit zu steigern. Die Strategie bietet Vorteile wie die Kombination von Indikatoren, die Betonung der Trendfolge und die Einbeziehung fundamentaler Faktoren, weist jedoch auch Nachteile wie Verzögerungen bei Fehleinschätzungen und eine unzureichende Drawdown-Kontrolle auf. Zukünftig kann die Strategie durch Optimierung der Parametereinstellungen, Verbesserung der Stop-Loss-Strategie und Hinzufügung weiterer fundamentaler Indikatoren weiterentwickelt werden, um in der praktischen Anwendung bessere Ergebnisse zu erzielen.

- 1