EMA-basierte Handelsstrategie

Überblick

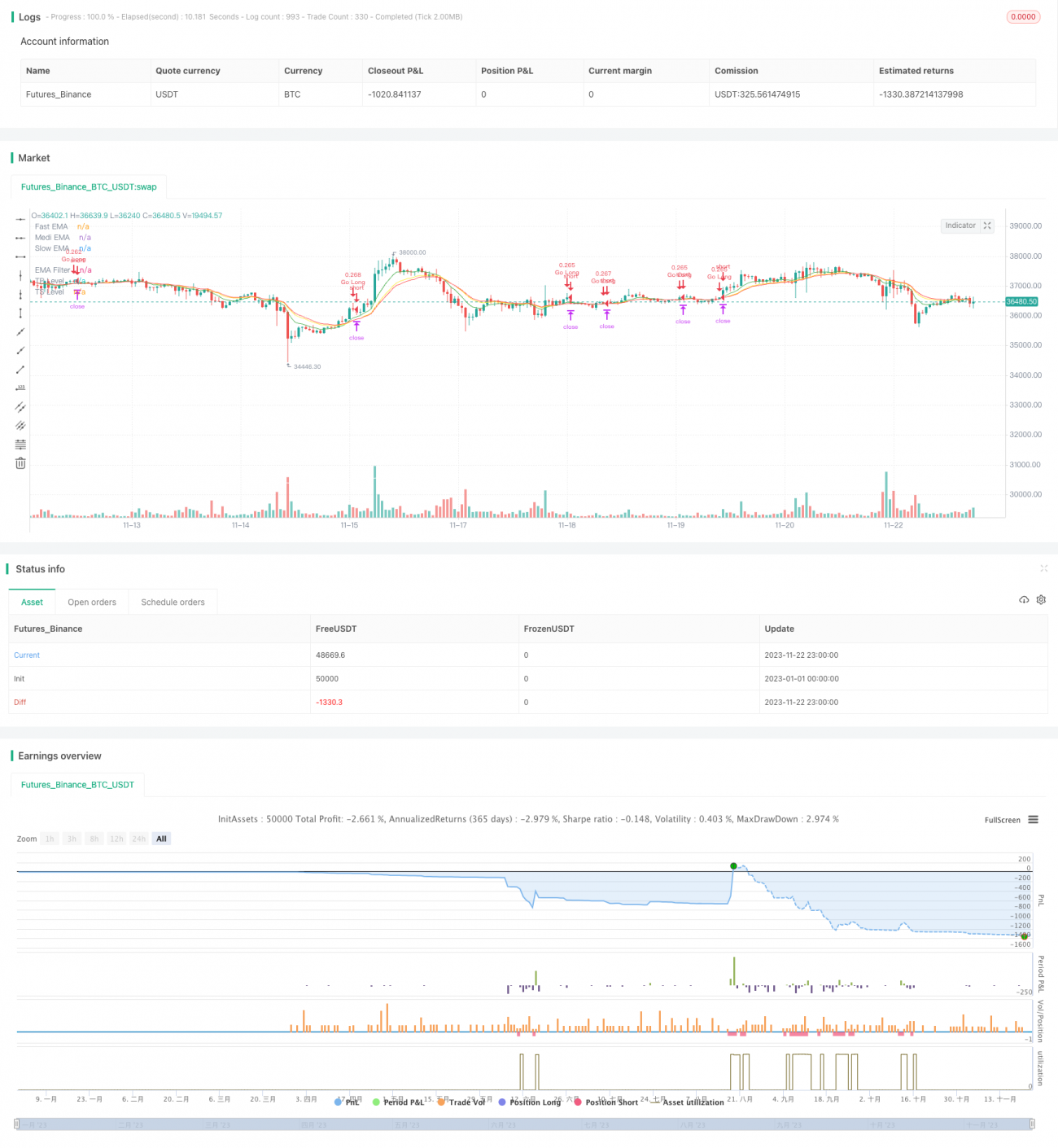

Diese Strategie verwendet vier EMA-Gleitende-Durchschnitte mit unterschiedlichen Zeiträumen und generiert Handelssignale basierend auf ihrer Anordnung, ähnlich den Farben Rot, Gelb und Grün einer Verkehrsampel. Daher wird sie als „Ampel-Trading-Strategie“ bezeichnet. Sie bewertet den Markt aus den Perspektiven Trend und Umkehr, um die Genauigkeit der Handelsentscheidungen zu verbessern.

Strategieprinzip

-

Es werden drei EMA-Linien eingerichtet: eine schnelle Linie (8 Perioden), eine mittlere Linie (14 Perioden) und eine langsame Linie (16 Perioden). Zusätzlich wird ein langer EMA (100 Perioden) als Filter verwendet.

-

Die Anordnung der drei EMA-Linien (schnell, mittel, langsam) und ihre Kreuzungen mit dem Filter werden ausgewertet, um Long- und Short-Einstiege zu bestimmen:

-

Wenn die schnelle Linie die mittlere Linie nach oben kreuzt oder die mittlere Linie die langsame Linie nach oben kreuzt, wird ein Long-Signal erkannt.

-

Wenn die mittlere Linie die schnelle Linie nach unten kreuzt, wird ein Long-Schließsignal erkannt.

-

Wenn die schnelle Linie die mittlere Linie nach unten kreuzt oder die mittlere Linie die langsame Linie nach unten kreuzt, wird ein Short-Signal erkannt.

-

Wenn die mittlere Linie die schnelle Linie nach oben kreuzt, wird ein Short-Schließsignal erkannt.

-

-

Durch die Anordnung der drei EMA-Linien wird die Trendrichtung und -stärke beurteilt, und durch die Kreuzungen mit dem Filter werden Umkehrpunkte erkannt. So wird eine Kombination aus Trendfolge und Umkehrerfassung erreicht.

Vorteilsanalyse

Diese Strategie vereint die Vorteile von Trendfolge und Umkehrhandel und kann Marktchancen gut nutzen. Die Hauptvorteile sind:

- Die Verwendung mehrerer EMA-Linien verbessert die Beurteilungskraft und reduziert Fehlsignale.

- Flexible Festlegung der Long/Short-Bedingungen vermeidet das Verpassen von Handelsmöglichkeiten.

- Die dreidimensionale Verwendung von kurz- und langfristigen Durchschnitten bietet eine umfassende Beurteilung.

- Anpassbare Take-Profit- und Stop-Loss-Bedingungen sorgen für ein angemessenes Risikomanagement.

Durch Parameteroptimierung kann die Strategie an verschiedene Instrumente angepasst werden und zeigt im Backtest eine starke Rentabilität und Stabilität.

Risikoanalyse

Die Hauptrisiken der Strategie sind:

- Bei chaotischer Anordnung der mehreren EMA-Linien wird die Beurteilung schwieriger, was zu Handelszögern führen kann.

- Fehlsignale durch ungewöhnliche Marktschwankungen, wie z. B. in stark schwankenden Märkten, können Verluste verursachen.

- Ungünstige Parametereinstellungen können dazu führen, dass Take-Profit- oder Stop-Loss-Bedingungen zu locker oder zu streng sind, was zu entgangenen Gewinnen oder übermäßigen Verlusten führt.

Es wird empfohlen, durch Parameteroptimierung, Festlegung von Stop-Loss-Niveaus und vorsichtiges Handeln die Stabilität der Strategie weiter zu verbessern und Risiken zu kontrollieren.

Optimierungsrichtungen

Die wichtigsten Optimierungsrichtungen der Strategie:

- Anpassung der Periodenparameter der EMA-Linien, um sie an weitere Instrumente anzupassen.

- Hinzufügen weiterer Indikatoren wie MACD, Bollinger-Bänder usw., um die Treffsicherheit zu erhöhen.

- Optimierung des Take-Profit/Stop-Loss-Verhältnisses, um ein optimales Gleichgewicht zwischen Risiko und Ertrag zu erzielen.

- Einführung adaptiver Stop-Loss-Mechanismen wie ATR-Stop-Loss, um das Abwärtsrisiko weiter zu kontrollieren.

Durch vielseitige Parameteranpassung und Einführung von Risikokontrollmechanismen kann die Stabilität und Rentabilität der Strategie kontinuierlich verbessert werden.

Zusammenfassung

Diese Ampel-Trading-Strategie kombiniert Trendfolge und Umkehrbewertung, verwendet vier EMA-Linien zur Generierung von Handelssignalen, passt sich durch Parameteroptimierung an verschiedene Instrumente an und zeigt im Backtest eine starke Rentabilität. Durch weitere Risikokontrolle und Einführung diverser Indikatoren kann sie sich zu einer stabilen und effizienten quantitativen Handelsstrategie entwickeln.

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © maxits

// 4HS Crypto Market Strategy- 1