Dynamische Volatilitätserfassung mit RSI-Bollinger-Bänder-Strategie

Überblick

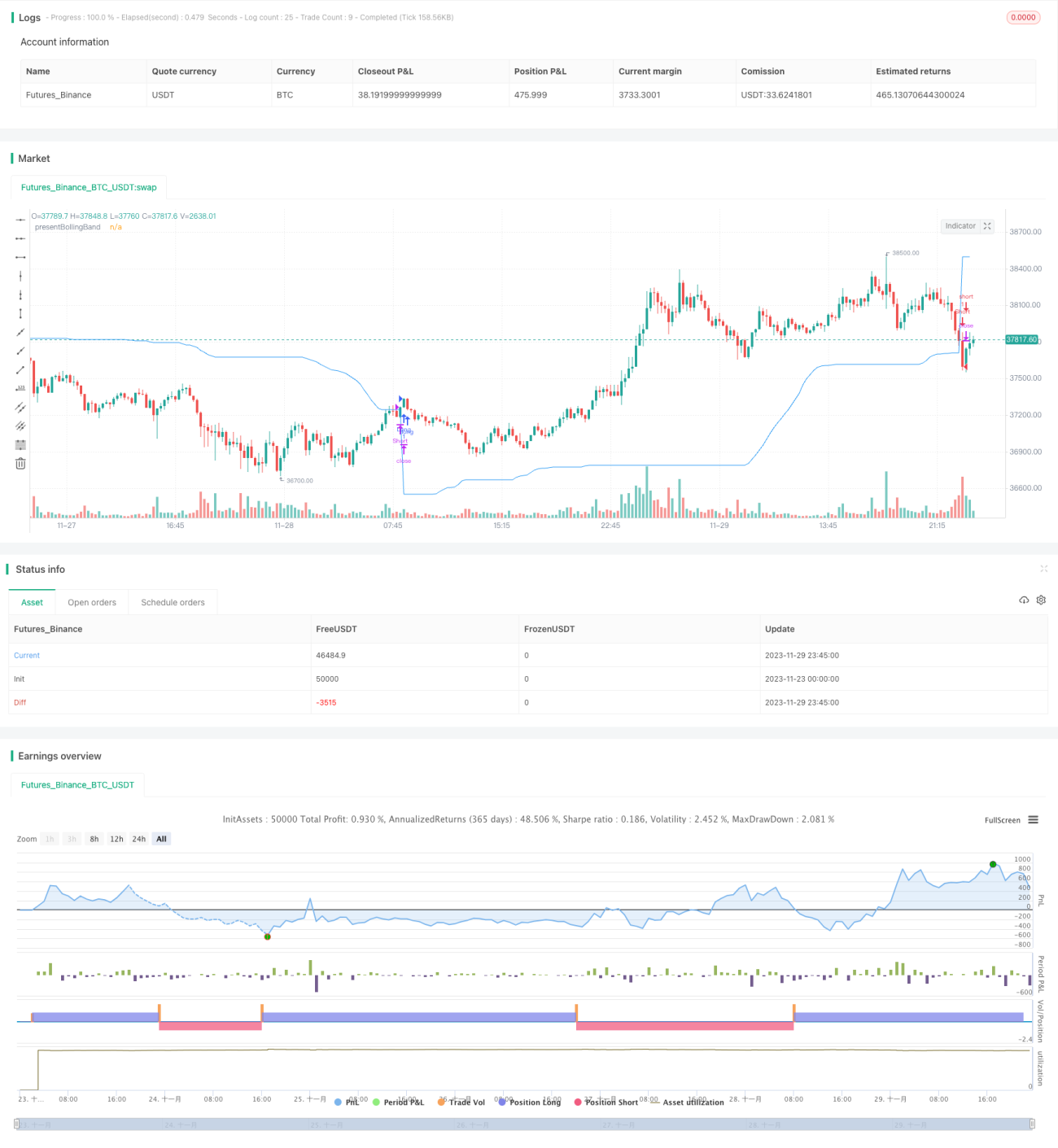

Die Dynamische Volatilitätserfassungs-RSI-Bollinger-Bänder-Strategie ist eine Handelsstrategie, die die Konzepte der Bollinger-Bänder (BB), des Relative-Stärke-Index (RSI) und des Simple Moving Average (SMA) integriert. Das Besondere an dieser Strategie ist, dass sie auf Grundlage des Schlusskurses zwischen dem oberen und unteren Band ein dynamisches Niveau berechnet. Diese einzigartige Funktion ermöglicht es der Strategie, sich an die Marktvolatilität und Preisbewegungen anzupassen.

Kryptowährungs- und Aktienmärkte sind sehr volatil und eignen sich daher hervorragend für Bollinger-Bänder-Strategien. Der RSI hilft dabei, überkaufte und überverkaufte Zustände in diesen oft spekulativen Märkten zu identifizieren.

Strategieprinzip

Dynamische Bollinger-Bänder: Die Strategie berechnet zunächst die oberen und unteren Bollinger-Bänder basierend auf einer benutzerdefinierten Länge und einem Multiplikator. Anschließend wird der Wert der presentBollingBand dynamisch unter Einbeziehung der Bollinger-Bänder und des Schlusskurses angepasst. Schließlich wird ein Long-Signal erzeugt, wenn der Kurs das presentBollingBand überschreitet, und ein Short-Signal, wenn der Kurs das presentBollingBand unterschreitet.

RSI: Wenn der Benutzer die Verwendung des RSI zur Signalerzeugung wählt, berechnet die Strategie auch den RSI und dessen SMA und verwendet diese zur Generierung zusätzlicher Long- und Short-Signale. Die auf dem RSI basierenden Signale werden nur verwendet, wenn die Option „RSI zur Signalerzeugung verwenden“ auf „true“ gesetzt ist.

Anschließend prüft die Strategie die gewählte Handelsrichtung und geht entsprechend eine Long- oder Short-Position ein. Wenn die Handelsrichtung auf „Beide Richtungen“ gesetzt ist, kann die Strategie sowohl Long- als auch Short-Positionen eingehen.

Schließlich werden Long-Positionen geschlossen, wenn der Schlusskurs das presentBollingBand unterschreitet; Short-Positionen werden geschlossen, wenn der Schlusskurs das presentBollingBand überschreitet.

Vorteilsanalyse

Die Strategie kombiniert die Stärken der Bollinger-Bänder, des RSI und des SMA-Indikators, passt sich der Marktvolatilität an, erfasst dynamisch Schwankungen und generiert Handelssignale in überkauften/überverkauften Situationen.

Der RSI-Indikator ergänzt die Bollinger-Bänder-Handelssignale und vermeidet Fehleinstiege in Seitwärtsmärkten. Ermöglicht die Wahl zwischen nur Long, nur Short oder beiden Richtungen, um sich an unterschiedliche Marktbedingungen anzupassen.

Die Parameter sind anpassbar und können auf individuelle Risikopräferenzen abgestimmt werden.

Risikoanalyse

Die Strategie basiert auf technischen Indikatoren und kann fundamentale Trendwenden nicht vorhersagen.

Eine ungeeignete Parametereinstellung der Bollinger-Bänder kann zu zu häufigen oder zu seltenen Handelssignalen führen.

Das Handeln in beide Richtungen birgt ein erhöhtes Risiko; Verluste aus Short-Positionen sind zu beachten.

Es wird empfohlen, einen Stop-Loss zur Risikokontrolle zu verwenden.

Optimierungsmöglichkeiten

-

Kombination mit anderen Indikatoren zur Signalfilterung, z. B. MACD.

-

Hinzufügen einer Stop-Loss-Strategie.

-

Optimierung der Parameter von Bollinger-Bändern und RSI.

-

Anpassung der Parameter an verschiedene Handelsinstrumente und Zeitrahmen.

-

Berücksichtigung von Live-Optimierungen und Anpassung der Parameter an die tatsächlichen Gegebenheiten.

Zusammenfassung

Die Dynamische Volatilitätserfassungs-RSI-Bollinger-Bänder-Strategie ist eine technisch indikatorgesteuerte Strategie, die die Stärken von Bollinger-Bändern, RSI und SMA kombiniert. Durch die dynamische Anpassung der Bollinger-Bänder wird die Marktvolatilität erfasst. Die Strategie bietet großen Spielraum für Anpassungen und Optimierungen, kann aber fundamentale Veränderungen nicht vorhersagen. Es wird empfohlen, die Wirkung im Live-Handel zu testen und bei Bedarf Parameter anzupassen oder weitere Indikatoren hinzuzufügen, um das Risiko zu reduzieren.

- 1