Bollinger Bänder ATR Trailing-Stop Strategie

Überblick

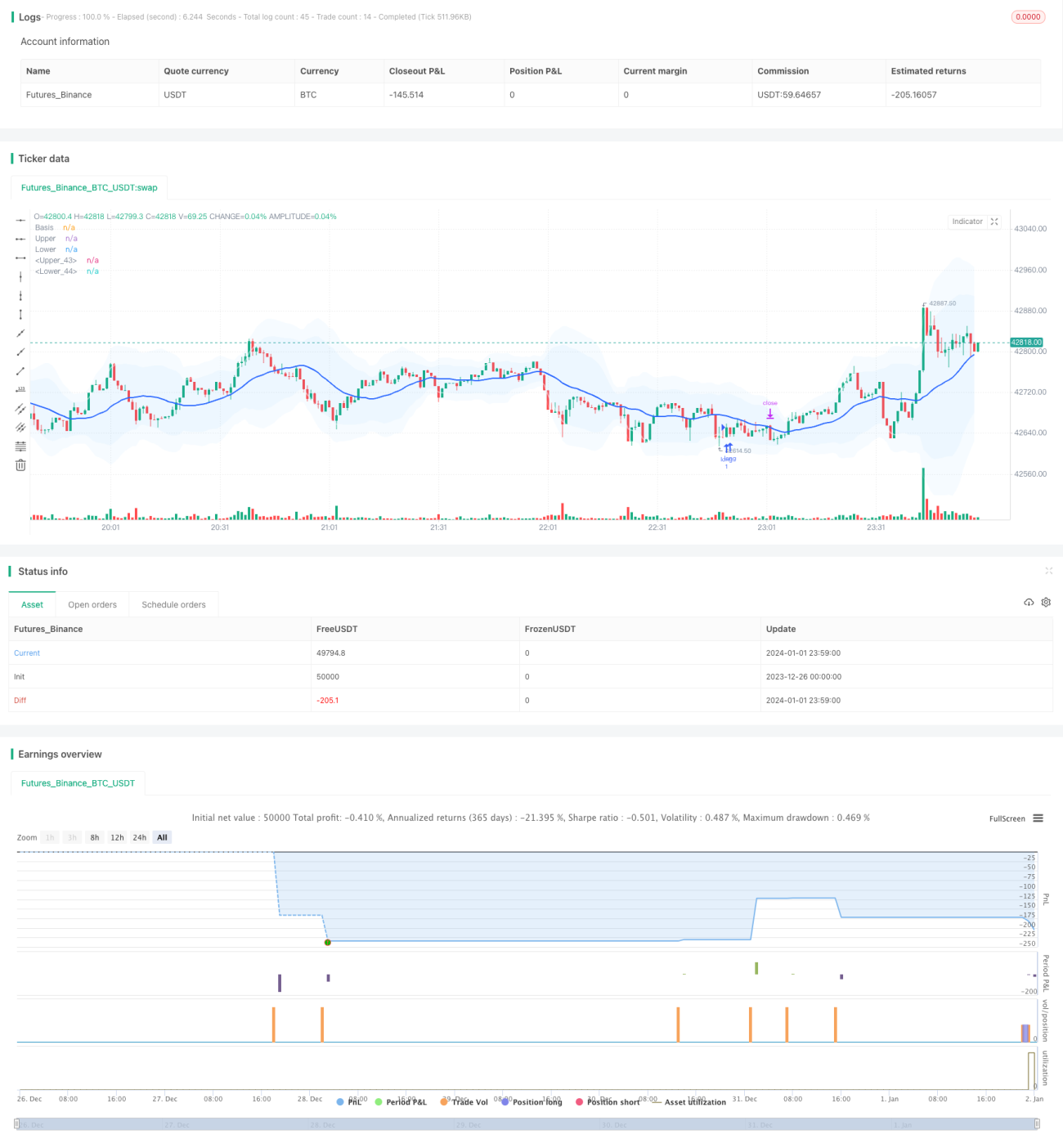

Diese Strategie kombiniert den Bollinger-Bänder-Indikator mit dem Average True Range (ATR)-Indikator, um eine Breakout-Handelsstrategie mit nachlaufendem Stop-Loss zu bilden. Wenn der Preis das obere oder untere Bollinger-Band mit der angegebenen Standardabweichung durchbricht, wird ein Handelssignal generiert. Gleichzeitig werden mit dem ATR-Indikator die Stop-Loss- und Take-Profit-Niveaus berechnet, um ein kontrolliertes Verhältnis von Gewinn zu Verlust zu ermöglichen. Darüber hinaus verfügt die Strategie über Funktionen wie Zeitfilter und Parameteroptimierung.

Funktionsweise der Strategie

Im ersten Schritt werden die Mittellinie, die obere Linie und die untere Linie berechnet. Die Mittellinie ist der einfache gleitende Durchschnitt (SMA) des Preises, während die oberen und unteren Linien ein ganzzahliges Vielfaches der Preisstandardabweichung darstellen. Wenn der Preis die untere Linie nach oben durchbricht, wird eine Long-Position eröffnet; wenn er die obere Linie nach unten durchbricht, wird eine Short-Position eröffnet.

Im zweiten Schritt wird der ATR-Indikator berechnet. Der ATR spiegelt die durchschnittliche Preisschwankungsbreite wider. Basierend auf dem ATR-Wert werden die Stop-Loss-Niveaus für Long- und Short-Positionen festgelegt. Gleichzeitig werden die Take-Profit-Niveaus basierend auf dem ATR-Wert festgelegt, um ein kontrolliertes Gewinn-Verlust-Verhältnis zu erzielen.

Im dritten Schritt wird ein Zeitfilter eingesetzt, um nur in bestimmten Zeiträumen zu handeln und starke Schwankungen bei wichtigen Nachrichtenereignissen zu vermeiden.

Im vierten Schritt kommt der nachlaufende Stop-Loss (Trailing Stop) zum Einsatz. Basierend auf dem aktuellen ATR-Wert wird der Stop-Loss in Echtzeit angepasst, um mehr Gewinne zu sichern.

Vorteile

- Die Bollinger-Bänder selbst geben den Preiskern besser wieder als ein einzelner gleitender Durchschnitt;

- Der ATR-Stop-Loss sorgt für ein kontrollierbares Risiko pro Trade;

- Der nachlaufende Stop-Loss passt sich automatisch an die Marktvolatilität an und sichert mehr Gewinne;

- Die Strategie bietet zahlreiche Parameter für individuelle Anpassungen.

Risikoanalyse

- In Seitwärtsmärkten können häufig mehrere kleine Verluste auftreten;

- Ein Ausbruch aus den Bollinger-Bändern kann als Umkehrsignal fehlschlagen;

- Der Handel während der Nachtstunden und bei wichtigen Nachrichten birgt hohe Risiken und sollte vermieden werden.

Gegenmaßnahmen:

- Strikte Einhaltung der Risikomanagement-Prinzipien, Kontrolle des Einzelverlusts;

- Optimierung der Parameter zur Verbesserung der Trefferquote;

- Einsatz des Zeitfilters zur Vermeidung risikoreicher Zeiträume.

Optimierungsmöglichkeiten

- Testen verschiedener Parameterkombinationen zur Optimierung der Konfiguration

- Hinzufügen von Volumenindikatoren wie OBV zum Timing

- Integration eines maschinellen Lernmoduls zur Optimierung

Zusammenfassung

Diese Strategie nutzt die Bollinger-Bänder zur Bestimmung des Preiskerns und der Ausbruchsrichtung, den ATR-Indikator zur Berechnung von Take-Profit und Stop-Loss zur Sicherung des Gewinn-Verlust-Verhältnisses sowie einen nachlaufenden Stop-Loss zur Gewinnsicherung. Der Vorteil der Strategie liegt in ihrer hohen Anpassbarkeit und dem kontrollierten Risiko, was sie für den kurzfristigen Intraday-Handel geeignet macht. Parameteroptimierung und maschinelles Lernen können die Trefferquote und Rentabilität der Strategie weiter verbessern.

- 1