Erweiterte SuperTrend-Strategie

Überblick

Die erweiterte Super-Trend-Strategie basiert auf einer Optimierung und Weiterentwicklung des klassischen Super-Trend-Indikators. Sie kombiniert Preisbewegung, Volatilität und mehrere technische Indikatoren, um die Signalqualität zu verbessern, Rauschen zu reduzieren und Markttrends präziser zu erfassen.

Strategieprinzip

Kern der erweiterten Super-Trend-Strategie ist die Super-Trend-Linie. Sie wird auf Basis der True Range und der Preisdynamik berechnet, um potenzielle Preistrends und Wendepunkte zu bestimmen. Liegt der Kurs über der Super-Trend-Linie, deutet dies auf einen Aufwärtstrend hin; darunter zeigt sich ein Abwärtstrend.

Im Gegensatz zum klassischen Super-Trend-Indikator, der nur Schlusskurs und True Range berücksichtigt, integriert die erweiterte Strategie auch Volumen, Momentum-Oszillatoren und fundamentale Daten, um die Zuverlässigkeit der Signale zu validieren. Dieser multivariate Ansatz stellt sicher, dass die erzeugten Handelssignale genauer und robuster gegenüber Marktrauschen sind.

Vorteile

Die Hauptvorteile der erweiterten Super-Trend-Strategie sind:

-

Präzisere Marktrichtungserkennung und Filterung falscher Ausbrüche. Durch die Abwartung mehrerer übereinstimmender Faktoren und Indikatoren wird die Trefferquote deutlich erhöht.

-

Reduzierung von Marktrauschen. Mit Hilfe kombinierter Filter können unwesentliche Marktdaten ausgeblendet werden, was eine klarere Entscheidungsfindung ermöglicht.

-

Optimiertes Risikomanagement. Klare Handelssignale helfen Händlern, Stop-Loss- und Take-Profit-Niveaus besser zu planen und verbessern so die Risikokontrolle.

-

Hohe Anpassungsfähigkeit. Neben der Trendidentifikation kann die Strategie mit anderen technischen Werkzeugen kombiniert werden, um ein umfassendes und effizientes Handelssystem aufzubauen.

Risikoanalyse

Die erweiterte Super-Trend-Strategie birgt auch folgende Hauptrisiken:

-

Risiko der Parametereinstellung. Eine falsche Kombination von Indikatorparametern kann dazu führen, dass die Strategie unwirksam wird oder zu viele Fehlsignale erzeugt.

-

Risiko von Trendfehleinschätzungen. Keine Strategie kann Fehlentscheidungen vollständig vermeiden; unerwartete Trendänderungen können zu Verlusten führen.

-

Überoptimierungsrisiko. Bei sehr präziser Parameteranpassung wird die Strategie zu stark an historische Daten angepasst und verliert ihre Anpassungsfähigkeit an Marktveränderungen.

-

Transaktionskostenrisiko. Mit zunehmender Handelsfrequenz steigen auch Transaktionskosten wie Gebühren und Slippage.

Entsprechende Lösungen:

-

Optimierung der Parameter und regelmäßige Backtests zur Überprüfung der Robustheit.

-

Setzen von Stop-Loss und Take-Profit zur Begrenzung von Einzelverlusten.

-

Vermeidung von Überoptimierung, um die Generalisierungsfähigkeit der Parameter zu erhalten.

-

Berechnung des Risiko-Ertrags-Verhältnisses der Signale zur Kontrolle der Transaktionskosten.

Optimierungsmöglichkeiten

Die erweiterte Super-Trend-Strategie kann in folgenden Bereichen optimiert werden:

-

Anpassung der Parameter an verschiedene Märkte, um sie besser an deren Eigenschaften anzupassen. In volatilen Märkten kann der Berechnungszeitraum verkürzt werden.

-

Integration eines adaptiven Filtermechanismus. Wenn der Markt in einen bestimmten Zustand eintritt, werden die Indikatorparameter automatisch angepasst oder bestimmte Filter deaktiviert.

-

Erforschung von Methoden des maschinellen Lernens, z. B. durch neuronale Netze, um Parameter dynamisch zu optimieren.

-

Einbeziehung von Sentiment-Indikatoren und Nachrichtenanalysen, um unstrukturierte Daten zur Verbesserung der Strategie zu nutzen.

-

Implementierung einer positionsgrößenabhängigen Skalierungsfunktion. Bei hoher Trefferquote kann durch Nachkauf der Gewinn gesteigert werden.

Zusammenfassung

Die erweiterte Super-Trend-Strategie verbessert den klassischen Super-Trend-Indikator durch die Einführung mehrerer Filter und Bestätigungsindikatoren. Sie ermöglicht eine genauere Marktrichtungserkennung und eine höhere Signalqualität. Im Vergleich zu einem Einzelindikator bietet die Strategie einen robusteren, umfassenderen und effizienteren Handelsansatz. Dennoch müssen die Risiken falscher Parametereinstellungen und Fehleinschätzungen beachtet werden, und es sind angemessene Risikokontrollmaßnahmen zu ergreifen. Durch kontinuierliche Optimierung und Kombination mit anderen Werkzeugen besitzt die erweiterte Super-Trend-Strategie ein großes Anwendungspotenzial.

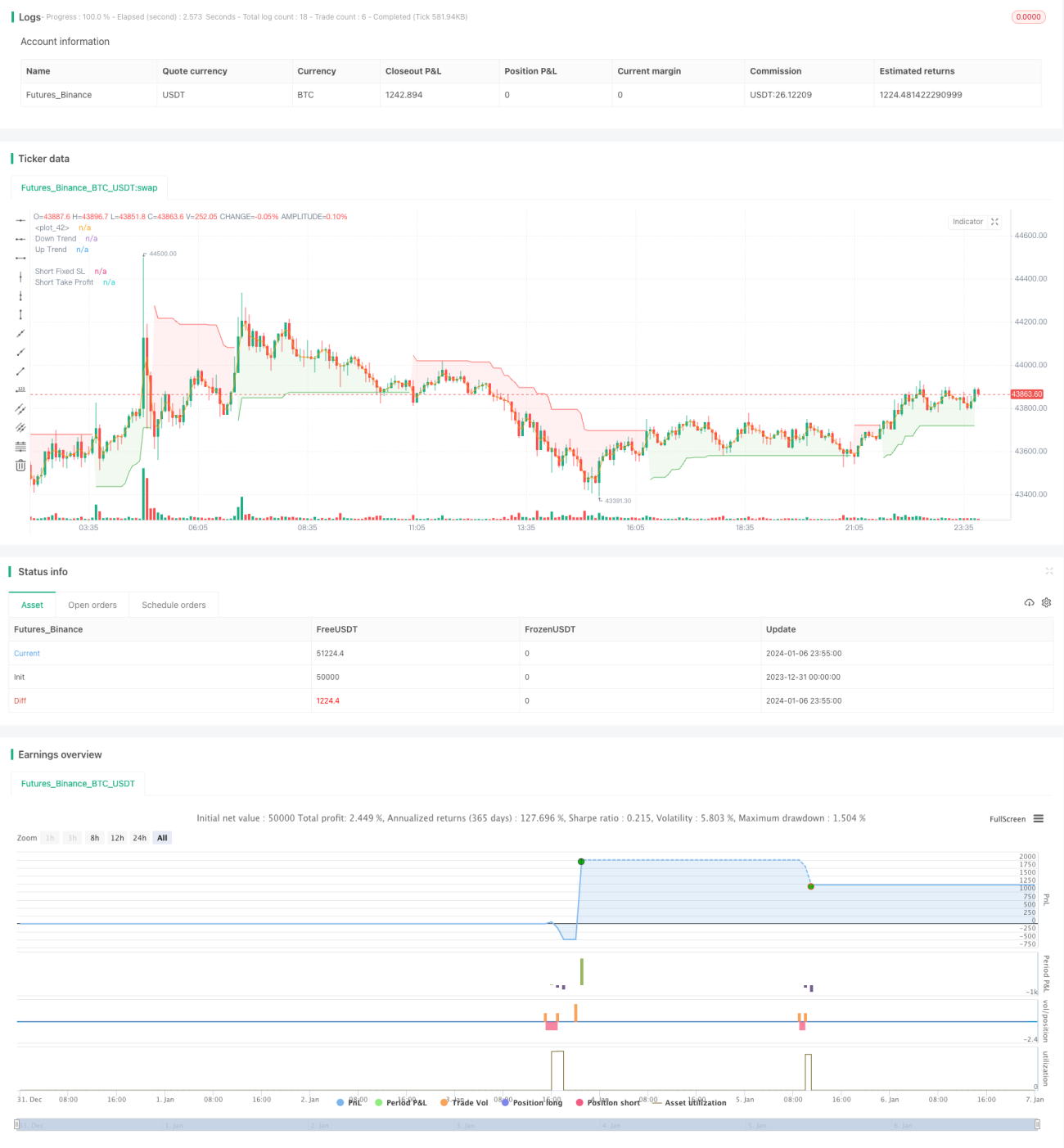

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © JS_TechTrading

//@version=5- 1