Bidirektionale adaptive Bereichsfilter-Momentum-Tracking-Strategie

1

Follow

1802

Followers

Übersicht

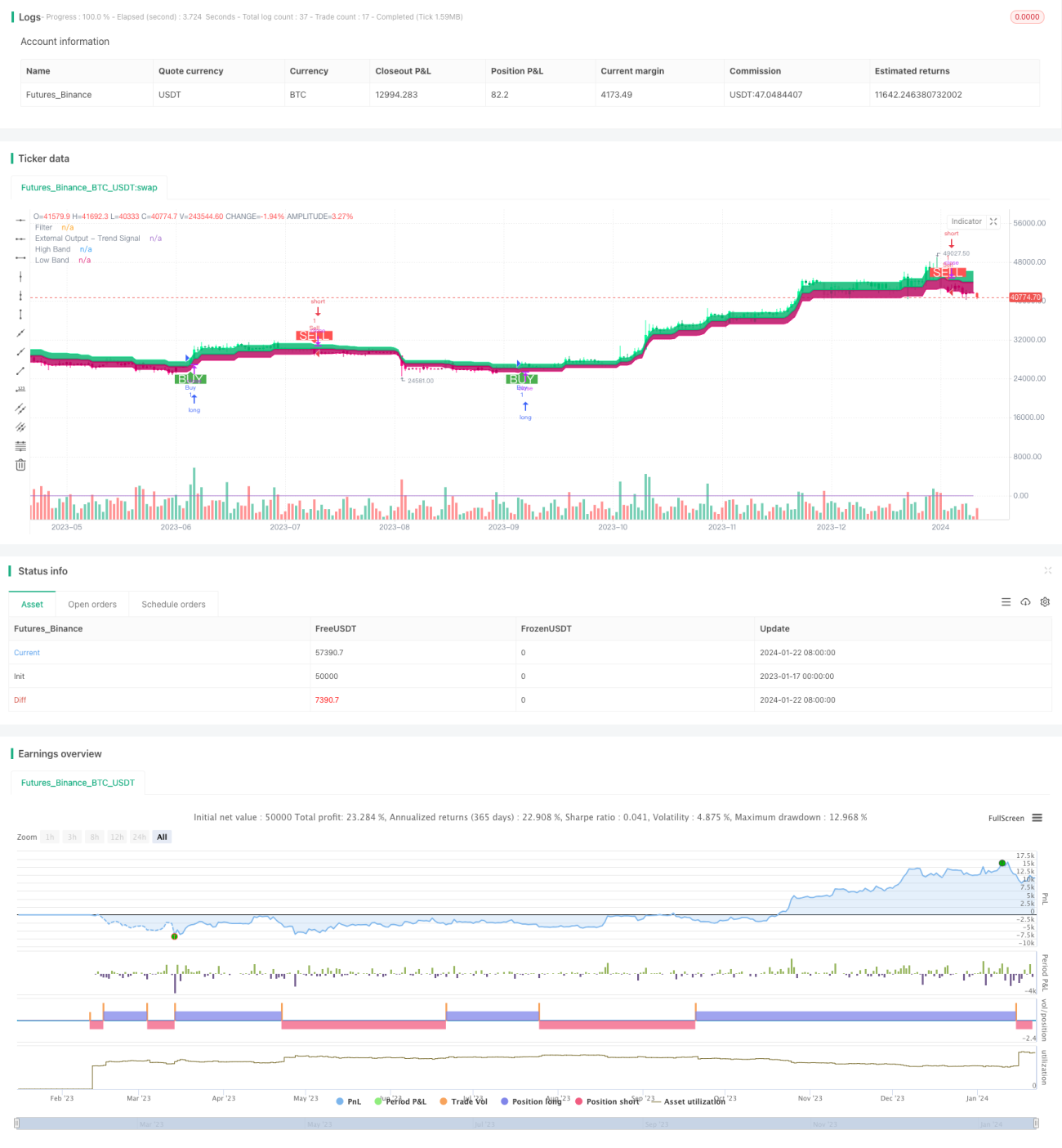

Diese Strategie ist eine bidirektionale adaptive Range-Filter-Momentum-Tracking-Strategie. Sie nutzt einen adaptiven Range-Filter, um Preisbewegungen zu verfolgen, und kombiniert diesen mit Volumenindikatoren, um die Wertrichtung zu bestimmen. So wird niedrig gekauft und hoch verkauft.

Funktionsweise der Strategie

- Ein adaptiver Range-Filter verfolgt die Preisschwankungen. Die Filtergröße passt sich automatisch an, basierend auf dem vom Benutzer festgelegten Range-Zeitraum, der Anzahl und dem Umfang.

- Es gibt zwei Filtertypen: Typ 1 (Standard-Range-Tracking) und Typ 2 (stufenweise gerundet).

- Die Richtung der Preisschwankungen wird anhand der Beziehung zwischen Filter und Schlusskurs bestimmt. Liegt der Preis über der oberen Schranke, gilt er als bullisch, unter der unteren Schranke als bärisch.

- Die Wertrichtung wird anhand der Veränderung des Schlusskurses gegenüber dem Vortag bestimmt. Steigt der Wert, handelt es sich um eine Long-Position, fällt er, um eine Short-Position.

- Ein Kaufsignal wird ausgelöst, wenn der Preis die obere Schranke durchbricht und der Wert steigt; ein Verkaufssignal, wenn der Preis die untere Schranke durchbricht und der Wert fällt.

Vorteile

- Der adaptive Range-Filter erfasst Marktschwankungen präzise.

- Zwei Filtertypen ermöglichen unterschiedliche Handelspräferenzen.

- Die Kombination mit Volumenindikatoren identifiziert die Wertrichtung effektiv.

- Die Strategie ist flexibel und kann an Marktbedingungen angepasst werden.

- Die Logik der Handelsbedingungen kann individuell angepasst werden.

Risikoanalyse

- Ungünstige Parametereinstellungen können zu übermäßigem Handel oder verpassten Signalen führen.

- Breakout-Signale unterliegen einer gewissen Verzögerung.

- Volumenindikatoren bergen ein gewisses Ruckelrisiko.

- Range-Ausbrüche können zu Fehlsignalen führen.

Risikominimierung:

- Geeignete Parameterkombinationen wählen und regelmäßig anpassen.

- Zusätzliche Indikatoren zur Trendbestimmung einsetzen.

- In der Nähe von Schlüsselniveaus und bei Trendumkehrungen vorsichtig handeln.

Optimierungsmöglichkeiten

- Verschiedene Kombinationen von Range-Größen und Glättungsperioden testen, um die optimale Kombination zu finden.

- Verschiedene Filtertypen ausprobieren, um den persönlichen bevorzugten Typ zu wählen.

- Andere Volumenindikatoren oder ergänzende technische Indikatoren testen.

- Die Logik der Handelsbedingungen optimieren und anpassen, um irrationale Trades zu reduzieren.

- Eine adaptive Positionsgrößenanpassung basierend auf der Markttypen-Theorie implementieren.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1