Auf Bollinger-Bändern und VWAP basierende Long-Breakout-Strategie

Übersicht

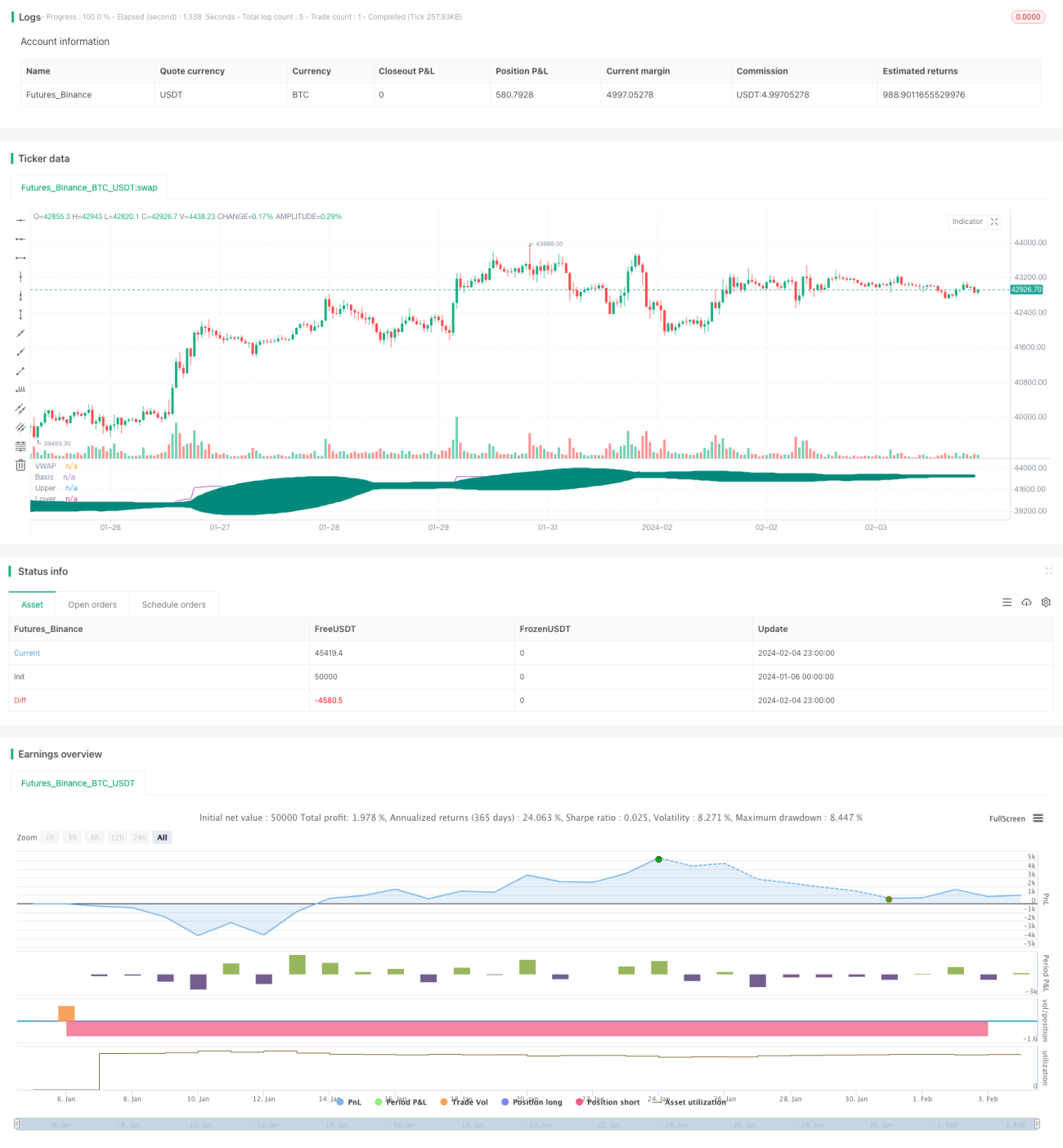

Diese Strategie nutzt Bollinger-Bänder zur Verfolgung des VWAP. Wenn der VWAP die mittlere Linie des Bollinger-Bandes nach oben durchbricht, wird dies als bullischer Ausbruch gewertet und eine Long-Strategie verfolgt. Sinkt der VWAP dagegen unter die untere Linie des Bollinger-Bandes, wird dies als bärische Bestätigung angesehen und die Position geschlossen. Zusätzlich wird der wichtige Unterstützungs-Pivot-Point als zusätzliche Bedingung für Einstiegssignale herangezogen, um falsche Ausbrüche zu filtern.

Funktionsweise der Strategie

- Berechnung des VWAP.

- Berechnung der Bollinger-Bänder des VWAP, bestehend aus oberer Linie, mittlerer Linie und unterer Linie.

- Überprüfung, ob der VWAP die mittlere Linie des Bollinger-Bandes nach oben durchbrochen hat. Ist dies der Fall und liegt der Kurs über dem wichtigen Pivot-Point-Unterstützungsniveau, wird eine Long-Position eröffnet.

- Der Stop-Loss beträgt 5 %.

- Sinkt der VWAP unter die untere Linie des Bollinger-Bandes, wird dies als bärische Bestätigung betrachtet und die Position geschlossen. Wird der Stop-Loss ausgelöst, wird die Position ebenfalls geschlossen.

Vorteile

- Der VWAP bietet eine starke Trendfolge und kann in Kombination mit Bollinger-Bändern den Start eines Trends präzise identifizieren.

- Die Einbeziehung des Pivot-Points als Zusatzbedingung filtert viele falsche Ausbrüche und vermeidet unnötige Verluste.

- Die teilweise Positionsschließung sichert einen Teil der Gewinne und begrenzt das Risiko.

- Backtests zeigen, dass die Strategie in Bullenmärkten hervorragend abschneidet und eine hohe Stabilität aufweist.

Risikoanalyse

- In Seitwärtsmärkten kann es leicht zu falschen Ausbrüchen kommen, die zu Verlusten führen.

- Der Pivot-Point kann falsche Ausbrüche nicht vollständig vermeiden; zusätzliche Indikatoren zur Signalfilterung sind erforderlich.

- Die teilweise Positionsschließung erhöht die Handelsfrequenz und damit die Transaktionskosten.

- In Bärenmärkten ist die Strategie weniger effektiv; ein Risikomanagement ist daher wichtig.

Optimierungsmöglichkeiten

- Es können weitere Indikatoren wie MACD oder KDJ zur Filterung von Ein- und Ausstiegssignalen hinzugezogen werden.

- Die Länge und Standardabweichung der Bollinger-Bänder können optimiert werden, um die beste Parametergruppe zu finden.

- Maschinelles Lernen könnte zur dynamischen Optimierung der Bollinger-Band-Parameter eingesetzt werden.

- Unterschiedliche Stop-Loss-Niveaus könnten getestet werden, um den optimalen Punkt zu finden.

- Ein adaptiver Ausstiegsmechanismus könnte integriert werden, der das Zielgewinnniveau an die Marktvolatilität anpasst.

Zusammenfassung

Insgesamt handelt es sich bei dieser Strategie um ein stabiles Ausbruchssystem. Durch die standardisierte Vorgehensweise und den großen Spielraum für Parameteroptimierung eignet sie sich gut für den quantitativen Handel. Gleichzeitig muss jedoch auf das Risikomanagement geachtet werden, um Verluste durch außergewöhnliche Marktsituationen zu vermeiden. Insgesamt ist sie eine ausbruchsorientierte Strategie, die es wert ist, eingehend erforscht und kontinuierlich verbessert zu werden.

- 1