Eine neuartige quantitative Trading-Strategie basierend auf dem ABCD-Muster mit Trailing-Stop-Loss und Trailing-Take-Profit

1. Strategieüberblick

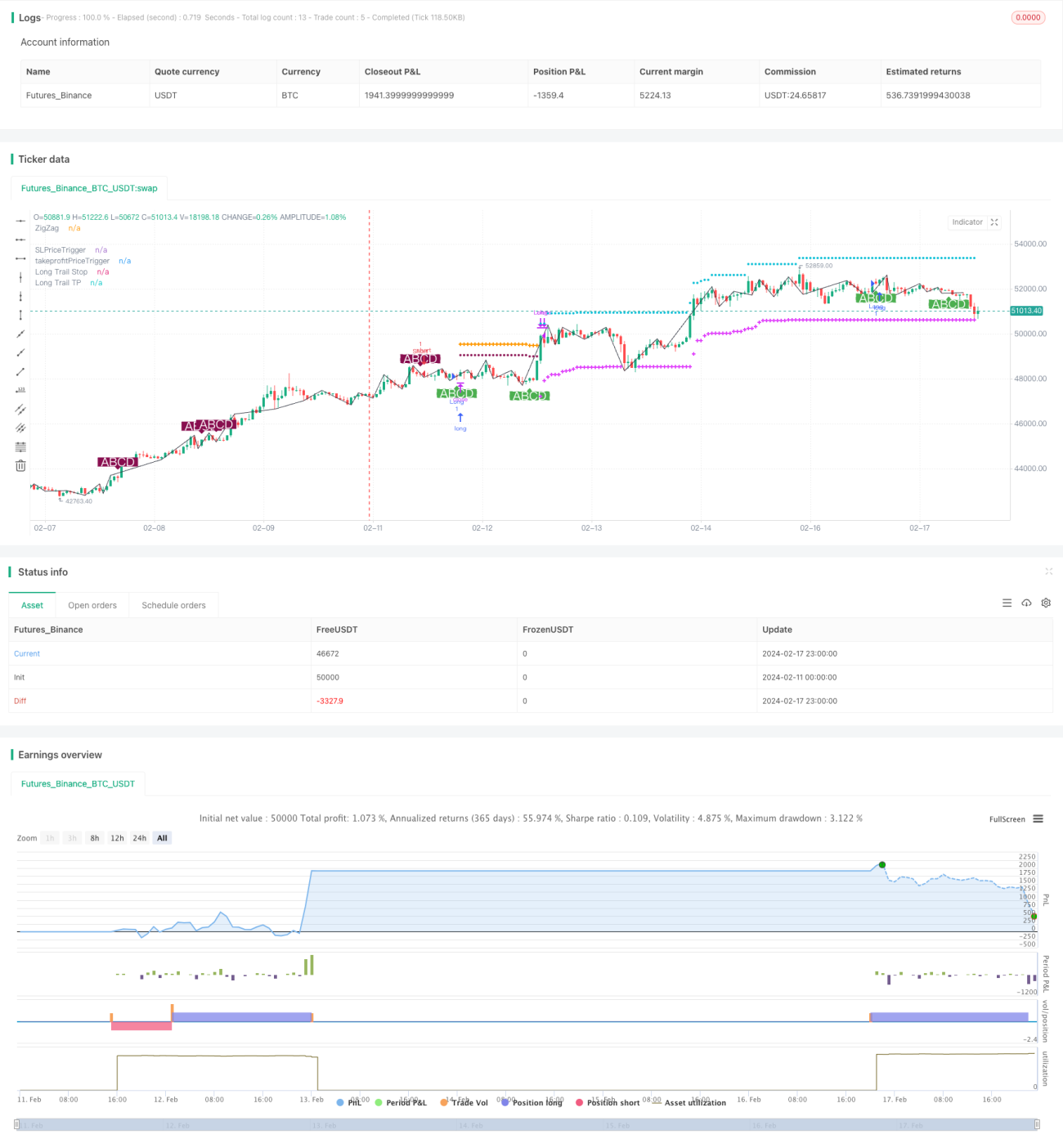

Die Strategie heißt „Beste ABCD-Formationshandelsstrategie (mit Trailing-Stop-Loss und Trailing-Take-Profit)“. Es handelt sich um eine quantitative Handelsstrategie, die auf einem eindeutigen ABCD-Preisformationsmodell basiert. Die Grundidee besteht darin, nach der Identifizierung einer vollständigen ABCD-Formation je nach Richtung der Formation long oder short zu gehen und Stop-Loss und Trailing-Take-Profit zur Positionsverwaltung einzusetzen.

2. Strategieprinzip

-

Zur Identifizierung von Hoch- und Tiefpunkten der Kurse wird die Bollinger-Band-Hilfsmethode verwendet, um eine ZigZag-Kurve der Kurse zu erhalten.

-

Auf der ZigZag-Kurve wird eine vollständige ABCD-Formation identifiziert. Die vier Punkte A, B, C, D müssen bestimmte proportionale Beziehungen erfüllen. Wird eine qualifizierte ABCD-Formation erkannt, wird long oder short gegangen.

-

Nach dem Eingehen einer Long- oder Short-Position wird ein Trailing-Stop-Loss zur Risikokontrolle gesetzt. Der Stop-Loss beginnt mit einem festen Stop, und sobald der Gewinn einen bestimmten Prozentsatz erreicht hat, wird auf einen gleitenden Stop umgeschaltet, um einen Teil des Gewinns zu sichern.

-

Ebenso wird für die Take-Profit-Linie ein Trailing eingerichtet, um nach Erreichen ausreichender Gewinne rechtzeitig Gewinne mitzunehmen und Gewinnrückgaben zu vermeiden. Auch das Trailing-Take-Profit erfolgt in zwei Phasen: Zuerst wird ein fester Take-Profit verwendet, um einen Teil des Gewinns zu sichern, danach wird auf einen gleitenden Take-Profit umgestellt, um den Kurs weiterzuverfolgen.

-

Wenn der Kurs den gleitenden Stop-Loss oder Take-Profit auslöst, wird die Position geschlossen und ein Handelszyklus abgeschlossen.

3. Analyse der Strategievorteile

-

Die Verwendung der Bollinger-Band-Hilfsmethode zur Identifizierung der ZigZag-Kurve vermeidet das Rückverfolgungsproblem herkömmlicher ZigZag-Kurven und macht die Handelssignale zuverlässiger.

-

Das ABCD-Formationshandelsmodell ist ausgereift und stabil und bietet relativ viele Handelsmöglichkeiten. Zudem ist die Richtung der ABCD-Formation eindeutig, sodass der Einstieg leicht zu bestimmen ist.

-

Die zweistufige Stop-Loss- und Take-Profit-Nachführung ermöglicht eine bessere Risikokontrolle und Gewinnsicherung. Die gleitenden Stop-Loss- und Take-Profit-Einstellungen machen die Strategie flexibler.

-

Die Strategieparameter sind sinnvoll gestaltet. Die Prozentsätze für Stop-Loss, Take-Profit und den Start des Trailing können individuell angepasst werden, was eine flexible Nutzung ermöglicht.

-

Die Strategie kann auf jede Anlageklasse angewendet werden, einschließlich Devisen, Kryptowährungen und Aktienindizes.

4. Analyse der Strategierisiken

-

Obwohl die ABCD-Formation relativ klar ist, sind die Handelsmöglichkeiten begrenzt, sodass keine ausreichende Handelsfrequenz garantiert werden kann.

-

In Seitwärtsmärkten kann es häufig zu Auslösungen von Stop-Loss und Take-Profit kommen. In diesem Fall müssen die Parameter entsprechend angepasst werden, um die Stop-Loss/Take-Profit-Bereiche zu erweitern.

-

Die Liquidität des gehandelten Instruments muss beachtet werden. Bei weniger liquiden Instrumenten können Stop-Loss und Take-Profit nicht präzise ausgeführt werden.

-

Die Strategie reagiert empfindlich auf Transaktionskosten. Daher sollten Broker und Konten mit niedrigen Gebühren gewählt werden.

-

Einige Parameter können weiter optimiert werden, z. B. die Startbedingungen für gleitenden Stop-Loss und Take-Profit, um durch Tests verschiedener Werte den optimalen Punkt zu finden.

5. Optimierungsrichtungen der Strategie

-

Es können andere Indikatoren hinzugefügt werden, um weitere Filterbedingungen zu setzen und bestimmte Fehlformationen zu vermeiden. Dies kann die Anzahl ineffektiver Trades reduzieren.

-

Die Einbeziehung einer Beurteilung der dreiteiligen Marktstruktur kann helfen, nur in der dritten Bewegung nach Handelsmöglichkeiten zu suchen. Dies kann die Trefferquote der Strategie erhöhen.

-

Testen und Optimieren der anfänglichen Kapitalgröße, um das optimale Startkapitalniveau zu finden. Zu groß oder zu klein ist nicht förderlich für die Erzielung der besten Rendite.

-

Es können Daten außerhalb der Stichprobe getestet werden, um die Robustheit der Parameter zu überprüfen. Dies ist für die Beurteilung der mittel- bis langfristigen Stabilität der Strategie notwendig.

-

Fortlaufende Optimierung der Startbedingungen für gleitenden Stop-Loss/Take-Profit und des Slippage-Werts, um die Ausführungseffizienz der Strategie zu verbessern. Die Optimierung der Einstellungen ist nie abgeschlossen.

6. Zusammenfassung der Strategie

Die Strategie basiert hauptsächlich auf der Identifizierung von ABCD-Kursformationen für die Marktbeurteilung und den Einstieg. Sie verwendet eine zweistufige Stop-Loss- und Take-Profit-Nachführung zur Steuerung von Risiko und Gewinn. Die Strategie ist relativ ausgereift und stabil, aber die Handelsfrequenz kann niedrig sein. Durch Hinzufügen von Filterbedingungen können effizientere Handelsmöglichkeiten erzielt werden. Darüber hinaus kann eine weitere Optimierung der Parameter und der Kapitalgröße die stabile Rentabilität der Strategie weiter verbessern. Insgesamt ist die Strategie klar strukturiert, leicht zu verstehen und umzusetzen und stellt eine quantitative Handelsstrategie dar, die es wert ist, eingehend untersucht und angewendet zu werden.

- 1