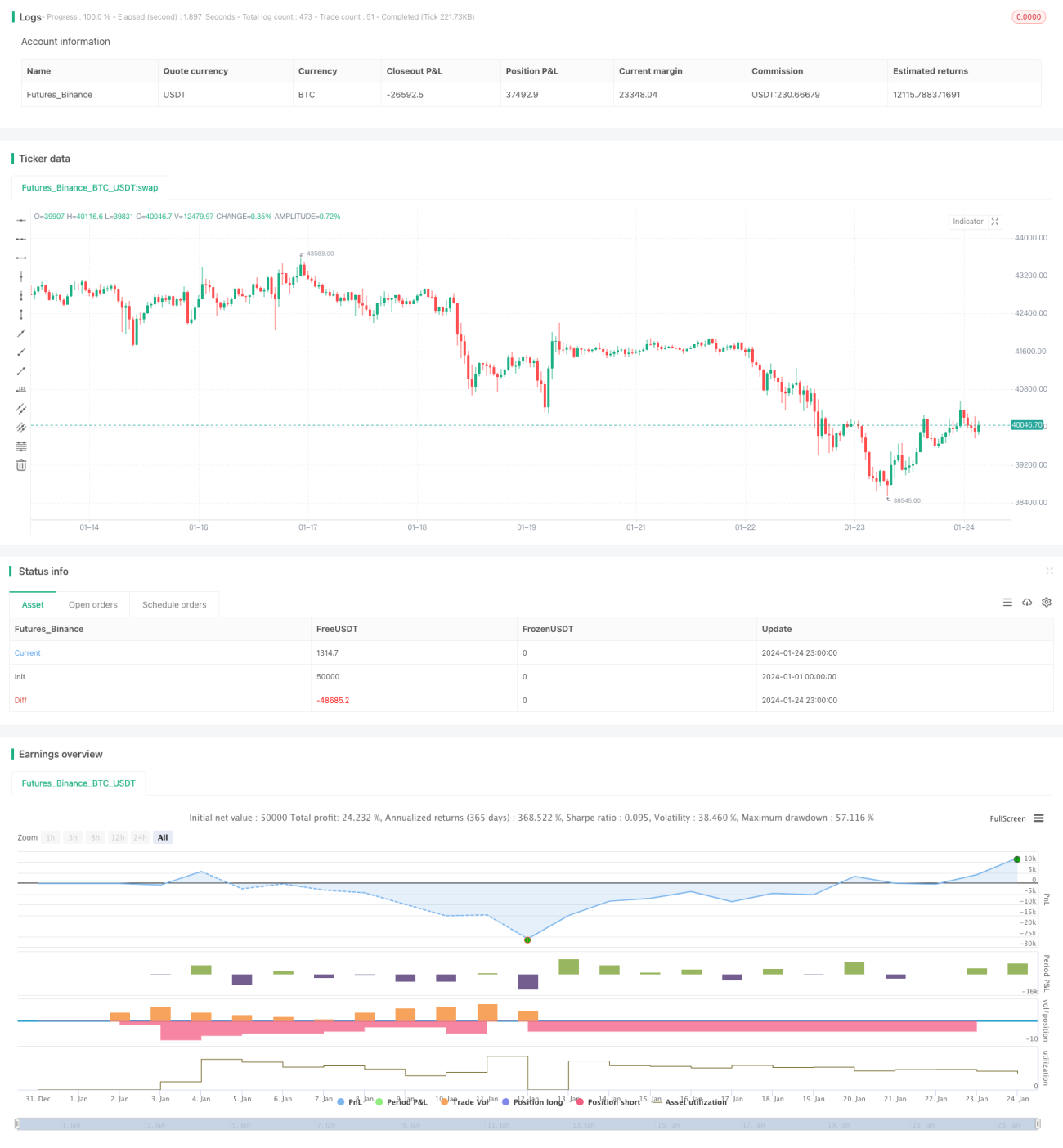

Auf einer quantitativen Handelsplattform basierende adaptive Grid-Trading-Strategie

Übersicht

Diese Strategie ist eine adaptive Grid-Trading-Strategie, die auf einer quantitativen Handelsplattform basiert. Durch die Festlegung eines automatischen oder manuellen Grid-Handelsbereichs werden Kauf- und Verkaufsaufträge in gleichmäßigen Abständen innerhalb des Bereichs platziert, um einen Grid-Handel zu realisieren. Wenn der Preis die obere oder untere Grenze des Grids durchbricht, passt die Strategie den Grid-Bereich automatisch an.

Strategieprinzip

-

Festlegen der oberen und unteren Preisgrenze des Grids. Die historischen Höchst- und Tiefstpreise innerhalb eines bestimmten Intervalls können automatisch als Grenzen berechnet werden, oder es können manuell feste obere und untere Preisgrenzen festgelegt werden.

-

Berechnung des Preisabstands zwischen den einzelnen Grids auf der Grundlage der oberen und unteren Preisgrenze sowie der Anzahl der Grids.

-

Innerhalb der oberen und unteren Preisgrenze werden mehrere Kauf- und Verkaufsstellen in gleichmäßigen Abständen als Grid angeordnet.

-

Wenn der Marktpreis die untere Grenze des Grids durchbricht, wird ein Kaufauftrag auf dem nächsten Grid unterhalb des Grids des aktuell letzten offenen Auftrags platziert. Wenn der Marktpreis die obere Grenze des Grids durchbricht, wird ein Verkaufsauftrag auf dem vorherigen Grid oberhalb des Grids des aktuell letzten offenen Auftrags platziert.

-

Auf diese Weise werden zwischen der oberen und unteren Grenze des Grids kontinuierlich Kauf- und Verkaufsoperationen durchgeführt. Wenn sich der Preistrend umkehrt, werden die vorherigen Aufträge schrittweise mit Gewinn oder Verlust geschlossen.

Strategievorteile

-

Der Grid-Handel kann in seitwärts gerichteten und volatilen Märkten Gewinne erzielen.

-

Die automatische Anpassung des Grid-Bereichs kann je nach Marktvolatilität ohne manuelles Eingreifen erfolgen.

-

Die zu investierende Geldmenge kann voreingestellt und proportional auf die einzelnen Grids verteilt werden, wodurch das Risiko pro Auftrag kontrolliert wird.

-

Einfache Logik, leicht verständlich, flexible Parameteranpassung.

Risiken und Gegenmaßnahmen

-

Verluste durch Durchbrechen der oberen/unteren Grenze

- Lösung: Angemessene Platzierung eines Stop-Loss.

-

Wiederholte Verluste in Trendmärkten

- Lösung: Erkennung des Trends und rechtzeitige Pausierung des Handels.

-

Unangemessene Parametereinstellungen

- Lösung: Anpassung der Grid-Anzahl und des Preisabstands.

Optimierungsmöglichkeiten

-

Nutzung von maschinellem Lernen zur Vorhersage von Preisbewegungen und Trends, dynamische Anpassung der Grid-Parameter.

-

In Trendmärkten Umstellung auf Trendhandel, um Verluste durch Grid-Handel zu vermeiden.

-

Kombination von Kapitalnutzungsrate, Renditekennzahlen usw. zur Risikokontrolle.

-

Erweiterung auf mehrere Instrumente zur breiteren Kapitalanwendung.

Zusammenfassung

Diese Strategie ist eine automatisch anpassbare, parameteradaptive Grid-Strategie, die für seitwärts gerichtete Aktien, Kryptowährungen und Deviseninstrumente geeignet ist. Durch die Anpassung der Parameter kann sie sich an unterschiedliche Marktbedingungen anpassen und besitzt einen gewissen praktischen Wert.

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-24 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//hk4jerry

strategy("Grid Bot Backtesting", overlay=false, pyramiding=3000, close_entries_rule="ANY", default_qty_type=strategy.cash, initial_capital=100.0, currency="USD", commission_type=strategy.commission.percent, commission_value=0.025)- 1