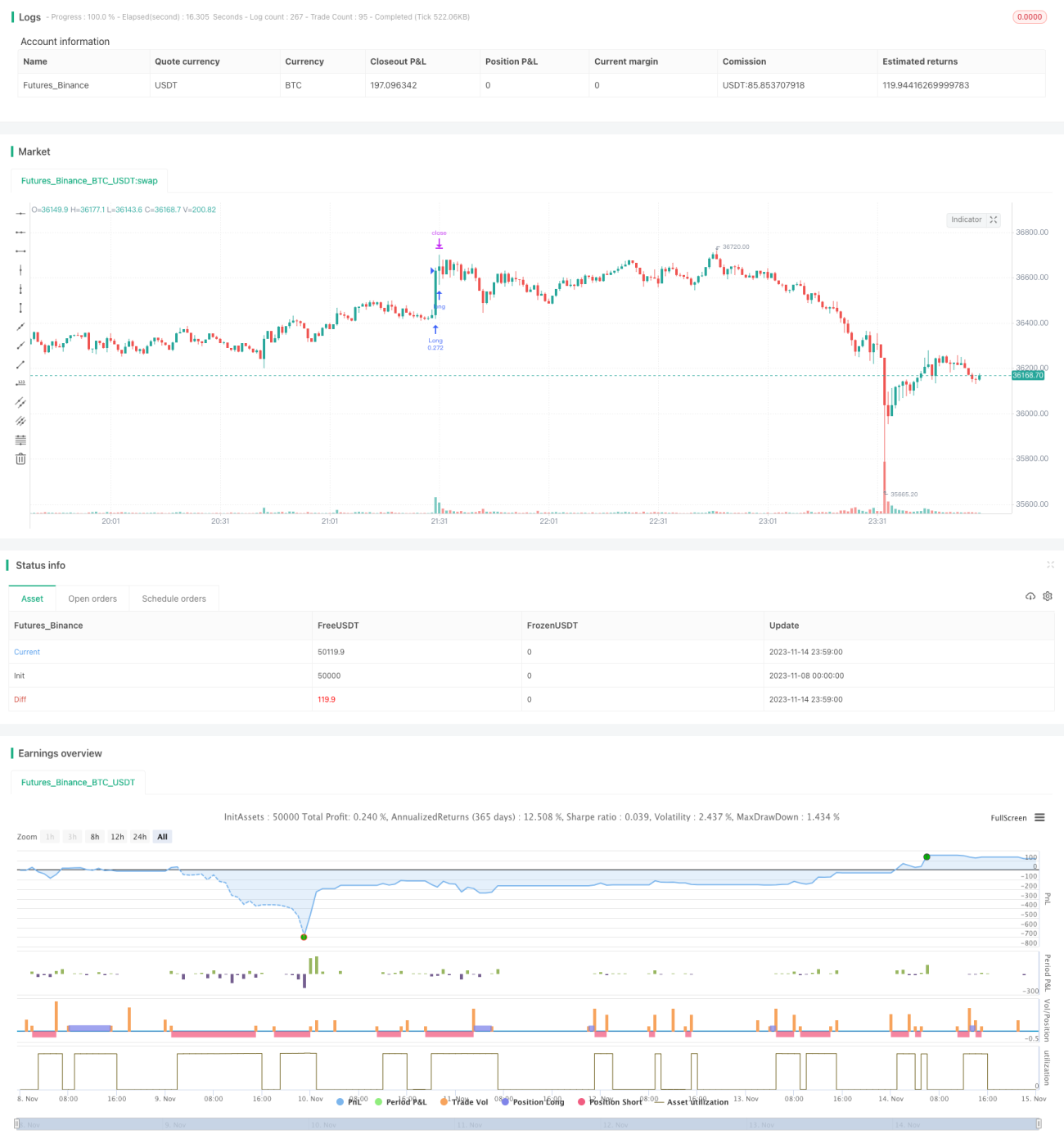

Estrategia de tendencias múltiples

Resumen

Esta estrategia combina múltiples indicadores para identificar la dirección de la tendencia, utilizando un enfoque de seguimiento de tendencia para capturar oportunidades en plazos cortos y medios. Está diseñada específicamente para seguir tendencias, con el objetivo de aumentar la tasa de aciertos y reducir las reducciones.

Principio de la estrategia

- Utiliza el indicador WVAP para evaluar la proporción de precios;

- El indicador RSI mide el impulso alcista y bajista;

- El indicador QQE identifica rupturas de precios;

- El indicador ADX evalúa la fuerza de la tendencia;

- El indicador Coral Trend determina la tendencia fundamental;

- El indicador LSMA ayuda a confirmar la tendencia;

- Combina señales de múltiples indicadores para generar órdenes de trading.

Esta estrategia depende principalmente de indicadores como RSI, QQE y ADX para determinar la dirección y la fuerza de la tendencia, y utiliza la curva del indicador Coral Trend como criterio fundamental. Cuando indicadores como RSI emiten una señal de compra, si el Coral Trend también muestra una curva ascendente, es muy probable que la tendencia sea alcista, por lo que la estrategia opta por comprar. Indicadores como WVAP se utilizan principalmente para evaluar si el nivel de precio es razonable y evitar comprar en máximos.

Ventajas de la estrategia

- Combinación de múltiples indicadores, mejorando la precisión de las señales;

- Énfasis en el seguimiento de tendencia, aumentando la probabilidad de ganancias;

- Enfoque en rupturas, filtrando mercados laterales;

- Incorporación de indicadores fundamentales, evitando operar en contra de la tendencia;

- Horarios de trading y tamaño de las posiciones razonables, reduciendo el riesgo;

- Lógica clara, fácil de entender y optimizar.

La mayor ventaja de esta estrategia es la combinación de múltiples indicadores, lo que reduce en cierta medida la probabilidad de errores de un solo indicador y mejora la precisión. Además, el énfasis en el seguimiento de tendencias y las rupturas ayuda a seleccionar oportunidades confiables a corto y mediano plazo. Asimismo, la inclusión de indicadores fundamentales evita operar en contra de la tendencia. Estos diseños aumentan la estabilidad y la probabilidad de ganancias de la estrategia.

Riesgos de la estrategia

- Existe un desfase en las señales de compra/venta, lo que puede provocar la pérdida de la mejor oportunidad de entrada;

- El control de reducciones no es perfecto, con un riesgo significativo de grandes reducciones;

- Cuando se produce un cambio fundamental, la estrategia puede perder la señal;

- No se consideran los costos de transacción, por lo que en la práctica los rendimientos pueden verse reducidos.

El mayor riesgo de esta estrategia es que la combinación de múltiples indicadores puede introducir un desfase, lo que lleva a perder el mejor momento de entrada y afecta el potencial de ganancias. Además, el control de reducciones no es ideal, con un riesgo considerable de grandes pérdidas. Cuando el mercado cambia fundamentalmente y los indicadores aún no lo reflejan, también se pueden generar pérdidas. En la práctica, los costos de transacción también afectan los rendimientos.

Direcciones de optimización de la estrategia

- Incorporar una estrategia de stop-loss para mejorar el control de reducciones;

- Optimizar los parámetros para reducir el retraso de los indicadores;

- Agregar más indicadores fundamentales para aumentar la precisión;

- Combinar algoritmos de aprendizaje automático para lograr una optimización dinámica de parámetros.

El enfoque de optimización debe considerar el control de reducciones. Se puede agregar un stop-loss móvil para asegurar ganancias y reducir las caídas. También se pueden optimizar los parámetros para acortar el retraso de los indicadores y mejorar la sensibilidad de la estrategia a los cambios del mercado. Además, se pueden incorporar más indicadores fundamentales para aumentar la precisión. Si se aplican métodos de aprendizaje automático para lograr una optimización dinámica de parámetros, la estabilidad de la estrategia mejoraría significativamente.

Conclusión

Esta estrategia combina múltiples indicadores para determinar la dirección de la tendencia, siguiendo un enfoque de seguimiento de tendencia diseñado para mejorar la precisión de las señales y aumentar la probabilidad de ganancias. La estrategia tiene ventajas como la combinación de indicadores, el énfasis en el seguimiento de tendencias y la integración de fundamentos, pero también presenta problemas como desfase en las señales y un control insuficiente de reducciones. En el futuro, se puede mejorar optimizando parámetros, perfeccionando la estrategia de stop-loss e incorporando más indicadores fundamentales, para lograr mejores resultados en la práctica.

- 1